Multi-Currency Consolidation: FX Translation Without the Headaches

Finance teams that manually consolidate across five or more currencies routinely spend 15+ days closing their books. Those with proper automation cut that to under five. The gap isn't knowledge. It's the sheer number of moving parts that compound with every subsidiary you add.

Multi-currency consolidation translates each subsidiary's financial statements from its functional currency into the group's presentation currency, then combines everything into one consolidated set of accounts. If your group operates entities in the US, Germany, and Singapore, you're juggling USD, EUR, and SGD before a single elimination journal is posted.

Any group with subsidiaries, franchises, or holding entities across borders needs this process; mid-market holding structures with three entities and large multinationals with fifty alike. The mechanics are the same; the pain scales.

Three things trip up even experienced controllers: applying different exchange rates to different line items (closing, average, historical), tracking cumulative translation adjustment movements period over period, and reconciling intercompany balances that never quite match after translation. Each of these deserves its own walkthrough, and that's exactly what the sections below cover.

What Exchange Rates Apply to Which Line Items?

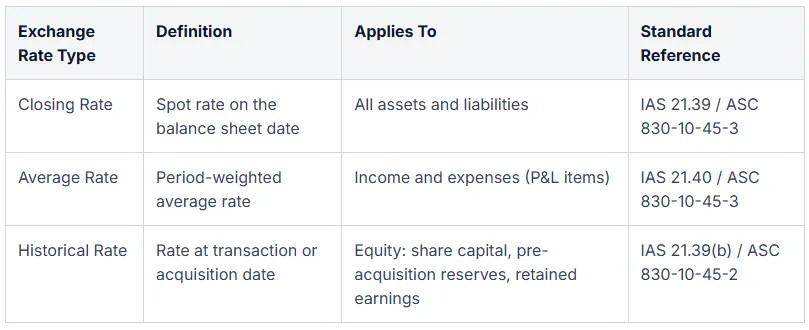

Under IAS 21 and ASC 830, three exchange rate types govern currency translation: closing rates for the balance sheet, average rates for the income statement, and historical rates for equity.

Getting the rate mapping wrong is where most translation errors originate. The logic feels straightforward on paper, but in practice it breaks down fast when you're consolidating a dozen entities across multiple reporting periods.

The closing rate (the spot rate on the balance sheet date) applies to all assets and liabilities. The historical rate is the exchange rate on the date of a specific transaction or acquisition, and it applies to equity components: share capital, pre-acquisition reserves, and certain retained earnings balances. The average rate is a period-weighted average, typically sourced from a central bank or rate provider, applied to revenue, expenses, and other income statement items.

A common misconception is that you can simplify this by using the closing rate for everything. Doing so violates both IFRS and US GAAP and creates artificial gains or losses in equity that auditors will flag immediately. The distinction between functional currency (the currency of the subsidiary's primary economic environment) and presentation currency (the group's reporting currency) drives the entire rate-mapping framework. A German subsidiary whose customers, suppliers, and financing are all EUR-denominated has EUR as its functional currency, regardless of whether the parent reports in GBP. Only once you've confirmed the functional currency can you determine which rates to apply during group consolidation.

Both IAS 21 and ASC 830 follow the same general methodology for rate application, but they diverge on specific disclosure requirements. IAS 21 requires disclosure of exchange differences recognised in profit or loss, while ASC 830 prescribes more granular analysis of cumulative translation adjustment changes. For dual-listed groups reporting under both frameworks, the translation mechanics are nearly identical. The footnotes are where the extra work lives.

How Does the Foreign Currency Translation Adjustment (CTA) Work?

The CTA is a balancing equity entry that arises because balance sheet items translate at closing rates while equity components translate at historical rates, creating an unavoidable periodic mismatch.

Every time the exchange rate moves between reporting periods, the translated value of a subsidiary's net assets changes, but the historical rate locked into share capital and pre-acquisition reserves doesn't. The residual difference flows into Other Comprehensive Income (OCI) and accumulates in a separate equity reserve, typically called the Foreign Currency Translation Reserve (FCTR). It bypasses the income statement entirely because it represents an unrealised translation effect, not a cash gain or loss.

Consider a UK-based group consolidating a US subsidiary. At Q1 close, the subsidiary holds net assets of $1,000,000 and the GBP/USD closing rate is 1.27, giving translated net assets of £787,402. By Q2 close, the rate shifts to 1.31. Net assets haven't changed in USD terms, but translated net assets are now £763,359. That £24,043 difference is the CTA movement for the quarter, sitting in the FCTR within consolidated equity. You can walk through the full FCTR calculation steps for a more detailed breakdown.

One question that rarely gets addressed is the difference between monthly and year-to-date (YTD) CTA calculation methodologies. Under the monthly approach, you recalculate the CTA each month using that specific month's closing and average rates. Under the YTD approach, you use cumulative averages from the start of the financial year, which smooths out intra-year volatility but produces different CTA and retained earnings figures.

Most groups default to the YTD method because it aligns with annual reporting and produces a cleaner reconciliation to the prior year-end FCTR balance. Groups producing monthly management accounts for board reporting often prefer the monthly method, since it gives a truer picture of how FX movements affected each individual period. Pick one approach and apply it consistently across all entities.

The CTA reserve is recycled to the income statement only when a foreign subsidiary is disposed of or substantially liquidated. Until that point, it accumulates in equity period after period.

How Do Intercompany Eliminations Work Across Currencies?

Intercompany eliminations across currencies produce residual FX differences because each entity records the same transaction at a different exchange rate on a different date.

This is one of the most persistent sources of out-of-balance consolidation journals. A parent invoices a subsidiary for management fees in GBP. The subsidiary records the expense in its local currency at the spot rate on the date it processes the invoice. The parent records revenue at face value. By the time both trial balances are translated into the group's presentation currency, the two sides of the intercompany balance no longer match. That residual isn't a booking error. It's a structural consequence of FX timing differences.

The problem shows up across every type of intercompany flow. Intercompany loans are the worst offenders because they sit on the balance sheet for extended periods, accumulating rate drift. Management fees and transfer pricing transactions create smaller but more frequent mismatches. Royalty payments between entities in volatile currency pairs can produce elimination variances that exceed the royalty amount itself in extreme quarters.

Conventional advice says to "just eliminate intercompany at the closing rate." That oversimplification causes audit differences because it ignores the distinction between monetary and non-monetary items. Monetary intercompany balances (receivables, payables, loans) should be eliminated in group currency after translation, with the FX residual posted to the translation reserve for long-term items or to the P&L for short-term operational items. Non-monetary intercompany balances (such as inventory purchased from a group entity) require elimination at the historical rate used by the receiving entity.

Take a concrete scenario: a USD parent lends $100,000 to a GBP subsidiary on January 1 at 1 USD = 0.79 GBP. The subsidiary records a payable of £79,000; the parent records a receivable of $100,000. At year-end, the rate moves to 1 USD = 0.76 GBP. After translation, the parent's receivable converts to £76,000 in group currency, while the subsidiary's payable also translates to £76,000 at the closing rate. The residual FX difference on elimination, driven by when each entity last revalued, flows to the FCTR for long-term intercompany loans.

The most common errors here: failing to reconcile intercompany balances before translation (so you're eliminating amounts that don't agree in local currency), using mismatched rate sources between entities, and attempting to eliminate in local currency rather than group currency. Each of these turns a mechanical process into an audit finding.

When Should You Move From Spreadsheets to Consolidation Software?

Finance teams managing three or more functional currencies on monthly reporting cycles will typically save 70-95% of translation time by switching from spreadsheets to consolidation software.

The common advice is to stick with Excel until you "outgrow it." Spreadsheets don't fail gradually, though. They fail silently. A mislinked VLOOKUP pulls last month's closing rate instead of this month's. A manual CTA journal uses the wrong historical rate for share capital. You won't catch these until an auditor flags them, and by then you've reported inaccurate group numbers.

The clearest signals that your spreadsheet process is breaking down: audit queries keep landing on your FX calculations, your close cycle stretches past ten days, and you're maintaining separate rate tables that nobody fully trusts. Once you're consolidating more than two currencies across monthly periods, rate management alone (closing rates, average rates, historical rates per equity tranche) becomes a full-time coordination exercise.

Dedicated consolidation software eliminates the manual steps that consume the most time and produce the most errors. Automated rate lookups pull closing and average rates from external providers like Open Exchange Rates without anyone copying figures into a spreadsheet. CTA calculations post automatically to OCI based on rate differentials the system detects each period. Intercompany matching identifies counterparty balances, eliminates them, and routes residual FX differences to the correct reserve, with a full audit trail behind every translated figure.

The question isn't whether your current process works today. It's whether it scales when the group adds two more subsidiaries next year, or when your auditors start asking for drill-down evidence on every FCTR movement. For a detailed breakdown of where spreadsheets typically fail in consolidation workflows, the comparison between consolidation software and Excel is worth reading.

The shift from spreadsheets to software isn't about convenience. It's about producing consolidated financial statements you can defend under audit pressure, every single period.

Frequently Asked Questions About Multi-Currency Consolidation

What is multi-currency consolidation?

It's the process of translating each subsidiary's trial balance from its functional currency into the group's presentation currency, then combining those translated figures into one set of consolidated accounts. The applicable standards are IAS 21 (IFRS) and ASC 830 (US GAAP), which prescribe how rates are selected and where translation differences are reported.

Which exchange rate should I use for balance sheet items vs. income statement items?

Assets and liabilities take the closing rate at period end. Revenue and expenses take the weighted average rate for the period. Equity accounts (share capital, pre-acquisition reserves) stay locked at historical rates from the date of the original transaction or acquisition.

What is a foreign currency translation adjustment (CTA)?

The CTA captures the mismatch that arises when balance sheet items translate at one rate and equity components translate at another. It sits in Other Comprehensive Income as a cumulative reserve. For a subsidiary with a strengthening functional currency, the CTA grows positive over time; for a weakening currency, it accumulates as a debit. It never hits the income statement unless the subsidiary is disposed of.

Why don't intercompany balances eliminate cleanly in a multi-currency group?

Because each entity books the transaction at the spot rate on the date it processes the invoice, and those dates rarely align. By the time both sides are translated into the presentation currency, rate movements create a residual that won't net to zero. This residual is a structural FX difference, not a booking error, and it needs to be routed to an appropriate reserve on elimination.

How does multi-currency consolidation differ on a monthly vs. year-to-date basis?

Monthly consolidation translates each month's P&L at that specific month's average rate and recalculates CTA at each month-end closing rate. YTD consolidation uses a cumulative average rate from the start of the financial year, which smooths out monthly volatility but produces different CTA and retained earnings figures. The two methods can yield materially different FCTR balances, so groups need to pick one approach and apply it consistently across all entities.

Take the FX Complexity Out of Your Next Consolidation

Manually managing rate lookups, CTA journals, and intercompany FX differences drains time that finance teams should spend on analysis. See exactly where the process breaks down in the consolidation software vs. Excel comparison, then book a demo of Group Financial Consolidation to see automated multi-currency handling in action.