Stop treating consolidated reporting as a compliance checkbox. It's the single process that determines whether your board, investors, and regulators trust your numbers. Spanning 5 entities or 500, the mechanics are the same: combine the financial statements of a parent company and every subsidiary it controls into one unified set of consolidated financial statements. The execution, though, is where things diverge dramatically.

A group with two domestic subsidiaries can often close consolidation in a couple of days using spreadsheets. Scale that to a dozen entities across four currencies with intercompany trading, and the same spreadsheet approach becomes a source of material risk. The 2025 BARC study on financial consolidation and group accounting found that renewal waves in consolidation tooling are accelerating as finance teams confront growing complexity, tighter deadlines, and auditor expectations that keep ratcheting upward.

Three forces make group financial consolidation especially consequential in 2026:

- Regulatory escalation: IFRS updates, mandatory iXBRL tagging in more jurisdictions, and ESG reporting integration mean consolidated statements now carry more disclosure requirements than at any point in the past decade.

- Investor scrutiny: Institutional investors increasingly parse segment-level data within consolidated reports to assess capital allocation quality, not just headline earnings.

- Automation momentum: Cloud adoption for consolidation reached 51% of surveyed companies in 2025, signaling that manual processes are becoming the exception rather than the norm.

- Multi-currency exposure: With continued FX volatility, currency translation errors in consolidation can swing reported group profit by meaningful percentages.

This guide walks through each stage of the consolidation process, from data collection through final reporting. It covers the three main consolidation methods (and when each applies), intercompany eliminations with worked journal entries, multi-currency translation under IAS 21, non-controlling interest measurement, and the automation tools reshaping how finance teams close the books. If you've been consolidating in Excel and feeling the cracks, or if you're scaling a group and need to build the process right from the start, the sections ahead give you a practical framework grounded in current standards and real-world practice.

When Is Group Financial Consolidation Required?

Group financial consolidation becomes necessary when a parent entity controls one or more subsidiaries. This typically means owning more than 50% of voting rights under IFRS 10, though de facto control can trigger the obligation even at lower ownership percentages.

Ownership percentage alone isn't the trigger. Control, as defined under IFRS 10, exists when an investor holds power over the investee, faces exposure to variable returns, and can use that power to influence those returns. That three-part test picks up situations where a parent owns less than 50% of voting rights but still wields de facto control through board appointments, contractual arrangements, or potential voting rights. US GAAP ASC 810 takes things further. Its variable interest entity (VIE) model casts a wider net, requiring consolidation whenever an entity is the primary beneficiary of a VIE, regardless of how much voting ownership it actually holds.

Ownership levels correspond to different accounting treatments:

- Controlling interest (>50% voting rights): Full consolidation is required. Every line item from the subsidiary's financials feeds directly into the group statements.

- Significant influence (20-50%): The equity method applies here. You carry the investment at cost, plus your share of any post-acquisition profits.

- Joint control: Under IFRS 11, joint ventures follow the equity method. For joint operations, you'll need to recognise your share of assets, liabilities, revenues, and expenses directly in the group accounts.

- Below 20%, no significant influence: Generally treated as a financial instrument under IFRS 9. These investments aren't consolidated.

Several exemptions exist. Investment entities that qualify under IFRS 10 don't consolidate their subsidiaries. Instead, they measure them at fair value through profit or loss. Intermediate parent companies can claim an exemption from preparing consolidated statements, provided their own parent produces IFRS-compliant group accounts that are publicly available. Immaterial subsidiaries can also be excluded, though defining "immaterial" calls for careful judgment and thorough documentation to satisfy auditors.

When a group expands from two entities to ten or more, the consolidation burden doesn't scale in a straight line. Intercompany relationships multiply fast. Ownership chains become layered, and figuring out which entities need full consolidation versus equity method treatment turns into a governance challenge all on its own. Groups at this stage typically discover that evaluating financial consolidation software is less of a nice-to-have and more of a practical requirement.

Here's one that catches groups off guard: acquiring a 48% stake paired with a shareholders' agreement granting veto rights over key decisions. That setup may not qualify as control under IFRS 10, but it could very well trigger consolidation under ASC 810's VIE model if the group absorbs the majority of expected losses or residual returns. Get the control assessment wrong at the outset, and you're looking at restatements that are painful, expensive, and fully visible to auditors and investors alike.

How to Consolidate Financial Statements: The Step-by-Step Process

Consolidating financial statements involves six distinct phases: data collection, alignment, currency translation, intercompany elimination, consolidation adjustments, and final review with reporting. What most teams don't realize is that close cycle length depends almost entirely on how well you've structured those first two phases.

Top-performing finance teams aim to close consolidation in five days. But many organizations, especially those still dependent on spreadsheets across multiple entities, need 15 to 20 days or more. The gap between these two realities? It nearly always hinges on how well the first two phases are organized.

Phase 1: Data Collection

Every consolidation kicks off by collecting trial balances and sub-ledger data from each entity in the group. The real bottleneck isn't the data itself. It's chasing down subsidiaries that submit late, use inconsistent formats, or send over unreconciled balances. Setting a firm submission deadline (usually day two or three after period-end) and enforcing a standardized reporting template will cut out most of the back-and-forth that drags close timelines out. The 2025 BARC study highlighted that standardizing templates is a key trend among groups working to reduce manual handling during the close.

Phase 2: Alignment

Subsidiaries spread across different jurisdictions frequently work with distinct charts of accounts, follow local accounting policies, or report on fiscal periods that don't line up. Before any figures can be merged, the group accountant has to map each entity's chart of accounts to the group's unified structure, adjust for policy variations (depreciation methods, revenue recognition timing), and pro-rate or restate numbers where reporting periods are mismatched. This is the stage where audit readiness gets built or falls apart. Teams that automate financial statements at the entity level tend to find this mapping step far less painful.

Phase 3: Currency Translation

For groups with overseas subsidiaries, IAS 21 lays out the translation method: assets and liabilities at the closing rate on the balance sheet date, income and expenses at the average rate for the period (or transaction-date rates where that's practicable). The resulting exchange difference gets recorded in other comprehensive income, not the P&L. Get this wrong and you'll inflate or deflate reported equity. Auditors know it too, and they'll test translation calculations line by line.

Phase 4: Intercompany Matching and Elimination

Before the group numbers mean anything, you've got to find, match, and strip out every transaction between entities within the group. This covers intercompany sales, loans, interest charges, management fees, and dividends. Unmatched balances (where one entity records £100,000 receivable but the counterpart shows £98,500 payable) need investigation and resolution before elimination entries can be posted. The next section walks through this process in detail with journal entries.

Phase 5: Consolidation Adjustments

After eliminations wrap up, the group accountant records adjustments that exist only at the consolidated level: goodwill from acquisitions, fair value uplifts on acquired assets, deferred tax on consolidation adjustments, and the split of profit or loss to non-controlling interests. None of these entries show up in any individual entity's books. That's exactly why they're so easy to overlook or miscalculate when you're working across disconnected spreadsheets.

Phase 6: Review and Reporting

The last phase produces the consolidated income statement, balance sheet, cash flow statement, and supporting notes. Analytical review at this point compares consolidated results to prior periods and budgets, flagging anomalies that could point to missed eliminations or translation mistakes. Your output needs to satisfy internal stakeholders (board packs, management reporting) while also meeting external requirements (statutory filings, auditor requests).

The difference between a five-day close and a twenty-day close seldom comes down to one phase. It's the cumulative weight of manual data collection, inconsistent entity-level reporting, and elimination errors, all compounding at every step along the way.

What Are the Different Consolidation Methods and When Should You Use Each?

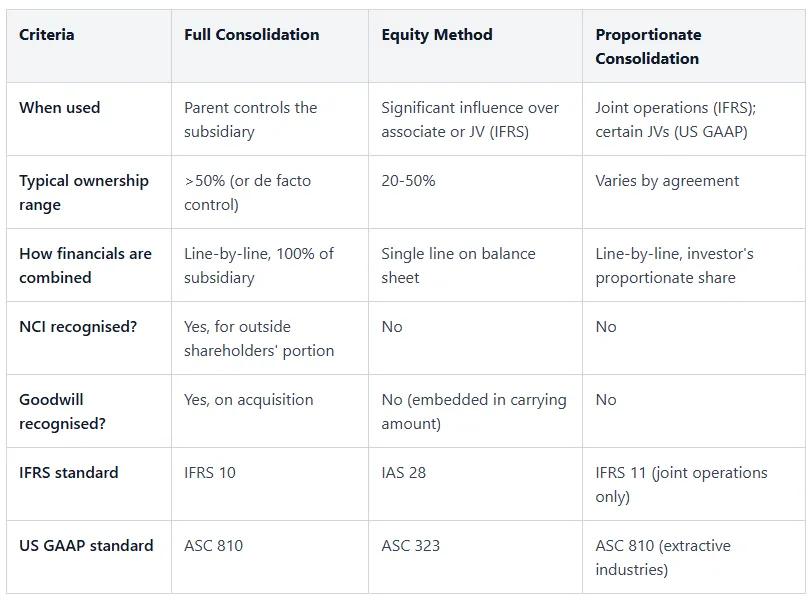

Under international and US standards, three consolidation methods apply: full consolidation, equity method, and proportionate consolidation. Each one is triggered by how much control or influence the investor holds over the investee.

Ownership percentage is a natural starting point when picking a consolidation method, but it's not what actually decides things. The real determinant is the nature of control, not the number sitting on the share register. Consider this: a parent holding just 45% of voting rights can still be required to fully consolidate if board composition, contractual terms, or de facto power satisfy IFRS 10's control criteria. Percentage gets you started. It doesn't give you the answer.

Full consolidation applies when the parent controls a subsidiary. You combine 100% of the subsidiary's assets, liabilities, revenues, and expenses on a line-by-line basis with the parent's own financials. The share of equity and profit that belongs to outside shareholders gets carved out as non-controlling interest. It's the method most finance teams spend the bulk of their time on, since it demands intercompany eliminations, goodwill calculations, and fair value adjustments.

The equity method applies to associates where the investor holds significant influence (typically 20-50% ownership) but doesn't have control. Rather than combining every line item, you record the investment as a single entry on the balance sheet at cost, plus your cumulative share of the associate's post-acquisition profits or losses. Dividends received reduce the carrying amount. Mechanically, it's much simpler. That said, the judgment call on whether "significant influence" actually exists can be surprisingly tricky when board representation is ambiguous or hard to pin down.

Proportionate consolidation was once the go-to treatment for joint ventures under IAS 31. IFRS 11 did away with that option: joint ventures must now apply the equity method under IFRS. Joint operations, where parties hold rights to specific assets and bear obligations for specific liabilities, still require you to recognise your proportionate share directly. US GAAP, on the other hand, keeps proportionate consolidation alive in certain extractive industries. Groups operating across both frameworks need to track which standard applies to each entity, and that's no small task.

Here's how the three methods stack up against the criteria that matter most when you're automating consolidation or putting a new group structure in place:

Incorrectly categorizing the relationship between a parent and an investee is one of the quickest routes to a material misstatement. If you treat an entity as an associate when it should be fully consolidated, you're understating group assets, liabilities, and revenues while concealing intercompany exposures that auditors will eventually uncover. Getting the control assessment right before selecting the method isn't merely good practice. It's the foundation that everything else in the consolidation process relies on.

How Do Intercompany Eliminations Work? A Worked Example

Intercompany eliminations strip out transactions between group entities so your consolidated financial statements don't inflate revenues, expenses, assets, or liabilities through double-counting. Of all the categories involved, unrealised profit in inventory is the one that catches most consolidation teams off guard.

Think about a 12-entity precision engineering group where the parent makes components and five subsidiaries handle final assembly. Intercompany trading accounts for roughly 30% of the group's combined revenue. If you skip eliminations, the consolidated income statement would inflate revenue by nearly a third. The balance sheet? It'd be loaded with receivables and payables that don't actually represent obligations to anyone outside the group.

Four types of intercompany transactions need to be eliminated:

- Intercompany sales and purchases: Revenue the selling entity records and cost of goods sold the buying entity books both need to be stripped out.

- Intercompany loans and interest: The loan receivable sitting on one entity's balance sheet and the matching payable on the other's cancel each other out, and so do the related interest income and expense.

- Intercompany dividends: Dividends a subsidiary pays to the parent show up as income for the parent and a distribution for the subsidiary. Both sides get eliminated.

- Unrealised profit in inventory: If goods sold between group entities haven't been sold on to external customers by year-end, the profit margin baked into that inventory isn't truly earned from the group's perspective.

That last category catches more consolidation teams off guard than any other. Here's how it plays out with specific numbers.

Worked example: Parent Co and Subsidiary Co

Parent Co sells inventory to Subsidiary Co for £500,000. The cost to Parent Co was £350,000, which means there's a £150,000 margin baked in. By year-end, Subsidiary Co has moved 60% of this inventory to external customers but still holds 40% (£200,000 at transfer price) in stock.

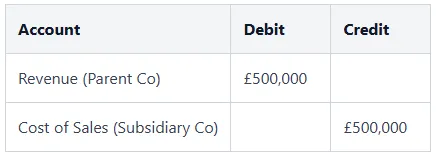

Journal entry 1: Eliminate intercompany revenue and cost of sales

This completely eliminates the intra-group sale from the consolidated income statement. External sales that Subsidiary Co made to third-party customers aren't affected.

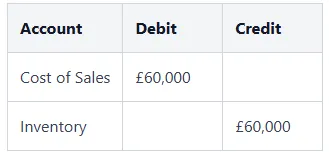

Journal entry 2: Eliminate unrealised profit in closing inventory

The remaining 40% still sits in Subsidiary Co's inventory at £200,000, but from the group's perspective, producing it only cost £140,000 (40% × £350,000). That leaves an unrealised profit of £60,000 (40% × £150,000 margin).

This adjustment brings inventory on the consolidated balance sheet down to its cost to the group. It also pushes up consolidated cost of sales, which cuts group profit by the £60,000 that hasn't yet been realised through a sale to an external party.

Mistakes in intercompany eliminations remain the most common source of consolidation misstatements. When intercompany trading is heavy, even minor matching discrepancies can spiral quickly. A subsidiary recording a purchase at one exchange rate while the seller books the sale at another, for example, creates elimination differences that require manual investigation to sort out.

For the engineering group described above, where intercompany revenue accounts for 30% of combined turnover, monthly elimination entries easily run into hundreds of line items. That's a lot of manual work. Teams relying on purpose-built tools to simplify group consolidations can automate the matching process and flag discrepancies before they turn into audit findings. But even with automation in place, your finance team still needs to understand the mechanics behind each elimination entry. The software depends on correct rules, and those rules come from human judgment about how transactions actually flow between entities.

How Should You Handle Non-Controlling Interests in Group Consolidation?

Non-controlling interest (NCI) is the portion of equity in a subsidiary that the parent doesn't own. It's shown separately within equity on the consolidated balance sheet. IFRS 3 provides two measurement methods here, and they can produce significantly different goodwill amounts.

If a parent holds 80% of a subsidiary, the other 20% sits with outside shareholders. Full consolidation still pulls in 100% of the subsidiary's assets, liabilities, and results. So how do you account for that outside slice? NCI is the mechanism that assigns the external shareholders' portion back to them, both on the balance sheet and in the income statement.

IFRS 3 lets you choose how to measure NCI at the acquisition date, and that choice carries real consequences for your goodwill calculation. The fair value method (sometimes called full goodwill) values NCI at its acquisition-date fair value, so goodwill ends up capturing both the parent's and the non-controlling shareholders' portions. The proportionate share method (partial goodwill) measures NCI at its share of the subsidiary's identifiable net assets, which produces a smaller goodwill figure. You don't have to pick one approach for the whole group, either. It's an election you make transaction by transaction, meaning different subsidiaries can follow different methods.

In the consolidated balance sheet, NCI appears within equity but gets its own separate line from the parent's shareholders' equity. The income statement divides total profit or loss for the period between what's attributable to the parent's shareholders and what's attributable to NCI. That same split carries through to the statement of changes in equity too.

A common error that keeps showing up in audits: not allocating losses to NCI when those losses drive the NCI balance into deficit. IFRS 10 is clear on this point. Losses must continue to be attributed to NCI, even when the result is a negative balance. Under the old IAS 27, loss allocation stopped once NCI hit zero, and some teams still haven't caught up with the change. Auditors in 2026 are paying closer attention to this specific area, driven by tighter regulatory scrutiny around transparency in group reporting.

Changes in the parent's ownership stake that don't result in losing control (buying an additional 5% from minority shareholders, for example) get treated as equity transactions. No gain or loss hits the P&L. The difference between what's paid and the corresponding adjustment to NCI is recognised directly in the parent's equity. It's only when control is actually lost that the full derecognition and remeasurement cycle kicks in. At that point, any retained interest gets remeasured at fair value, and a gain or loss is recognised in profit or loss.

The NCI measurement choice at acquisition carries more weight than most groups appreciate at the time. When you opt for full goodwill on a sizable acquisition, you're putting a larger asset on the balance sheet, one that's subject to yearly impairment testing. That can introduce real earnings volatility years later if the subsidiary doesn't perform as expected.

Why Is Multi-Currency Consolidation So Challenging?

Multi-currency consolidation requires applying three different exchange rates across the balance sheet, income statement, and equity, creating translation differences that compound through multi-tier group structures and can dwarf a subsidiary's reported profit in volatile currency environments.

A 20-entity group operating across eight currencies doesn't just translate once. Each subsidiary's trial balance passes through IAS 21's rate hierarchy: assets and liabilities convert at the closing rate on the reporting date, income and expenses at the average rate for the period (or transaction-date rate for material items), and equity components at the historical rates prevailing when capital was contributed or reserves were earned. The resulting mismatch between the balance sheet (closing rate) and the income statement (average rate) lands in other comprehensive income as the foreign currency translation reserve (FCTR). For groups with significant operations in volatile currencies, the FCTR swing can dwarf the subsidiary's reported profit.

A shortcut some less experienced teams apply is using the closing rate across everything to simplify translation. That approach creates material misstatement in equity and distorts period-over-period trend analysis, because equity translated at closing rates will fluctuate with every reporting date even when the underlying business hasn't changed. Auditors flag this routinely, and restating after the fact burns days you don't have during the close.

The real headache arrives with multi-tier translation. Picture a Japanese subsidiary (functional currency JPY) owned by a European intermediate holding company (EUR), which itself reports into a UK ultimate parent (GBP). The JPY financials translate into EUR first, generating one FCTR. Then the EUR intermediate's consolidated results, including that FCTR, translate into GBP, generating a second FCTR. Each step introduces its own translation differences, and the two reserves don't net cleanly. If the intermediate holding also has its own trading activity in EUR, you're reconciling three layers of currency impact in a single consolidation pack.

Things get worse when a subsidiary's functional currency differs from its local currency. A Nigerian subsidiary billing in USD but incurring costs in naira must first remeasure its local-currency transactions into USD (its functional currency) under IAS 21's individual-entity rules, generating exchange gains and losses in profit or loss. Only then does the group translate the USD functional-currency financials into the parent's presentation currency, generating FCTR in OCI. Two separate currency processes, two separate accounting treatments, feeding into one set of consolidated numbers.

2026 has amplified these pressures. Emerging-market currencies across West Africa, South America, and Southeast Asia have seen monthly swings exceeding 5% against major currencies, making quarterly translation reconciliation inadequate. Monthly reconciliation of FCTR movements against actual rate movements is now the baseline expectation from audit committees. Teams that reconcile only at year-end find unexplained variances accumulating to the point where the close itself becomes an investigation rather than a process.

Finance teams running multi-currency consolidations should maintain a rate source log documenting which exchange rate provider, rate type (spot, average, or historical), and extraction date was used for every translation. Auditors increasingly request this as standard working paper support, and retroactively reconstructing it's painful.

What Are the Key Differences Between IFRS 10 and US GAAP ASC 810?

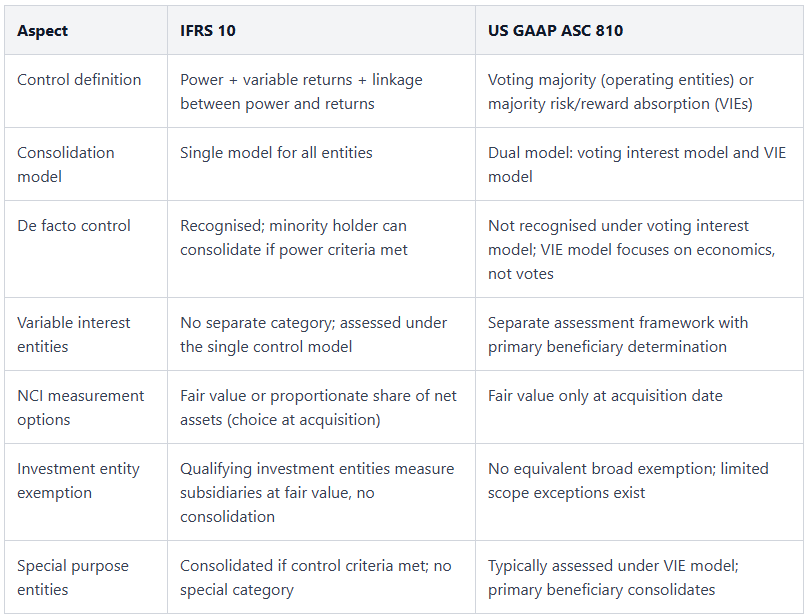

IFRS 10 uses a single control model based on power over an investee, while US GAAP ASC 810 operates a dual model splitting voting interest entities from variable interest entities, and the same investment can fall inside the consolidation boundary under one standard and outside it under the other.

For groups reporting under only one framework, the distinction is academic. For dual-listed companies or multinational groups with US and European operations, this divergence has real consequences. It happens regularly with structured entities, joint arrangements, and investment vehicles.

The core divergence sits in how each standard defines control. IFRS 10 asks three questions about every investee: does the investor have power over it, is the investor exposed to variable returns, and can the investor use that power to affect those returns? All three must be satisfied simultaneously. IFRS 10 also recognises de facto control, meaning a 35% shareholder can be the consolidating parent if the remaining shares are widely dispersed and no other party can coordinate a majority. US GAAP ASC 810 takes a different path. For traditional operating entities, it applies the voting interest model: whoever holds more than 50% of voting shares consolidates. For structured entities, it switches to the variable interest entity (VIE) model, asking which party absorbs the majority of expected losses or receives the majority of expected residual returns.

The practical consequence for a dual-reporting group is that consolidation scope can differ between the two sets of financial statements. A structured securitisation vehicle might sit off-balance-sheet under IFRS 10 (because the group lacks power over its relevant activities) but require consolidation under ASC 810's VIE model (because the group absorbs the majority of expected losses). Finance teams maintaining parallel reporting packs need to map every investee against both frameworks and document the conclusion separately.

As of early 2026, the IASB and FASB continue their periodic convergence discussions, but no joint exposure draft has been issued that would unify these two approaches. The gap persists, and teams should plan their consolidation policies accordingly rather than anticipating imminent alignment.

How Can Automation and Software Reduce Consolidation Risk and Time?

Specialized financial consolidation software can cut close cycles from 15+ working days to under five. It also removes the formula mistakes and version-control failures that turn spreadsheet-based consolidation into a growing risk as group structures scale.

Spreadsheets are still the go-to tool for a surprising number of mid-market groups, and every new entity in the structure just piles on more risk. One broken VLOOKUP in a master consolidation workbook can quietly ripple through intercompany matching, currency translation, and NCI allocation before anyone catches it. Version control is its own headache. When three people edit copies of the same consolidation file during a compressed close window, reconciling those versions often eats up more time than the original consolidation work itself.

The financial consolidation software market tells you a lot about how seriously organisations are treating this challenge. Industry research puts the market at $2.7 billion in 2024, with projections reaching $6.4 billion by 2032 at a compound annual growth rate of 11.4%. Compliance alone isn't driving that growth. Roughly 42% of organisations now connect their consolidation platform with planning and reporting tools, effectively turning consolidated actuals into the foundation for budgeting, forecasting, and strategic analysis.

Trust in the numbers matters just as much as speed. Studies show that 40% of CFOs question the accuracy of manually consolidated data. That kind of skepticism chips away at confidence in board packs, investor reporting, and the internal decisions that shape strategy. Automated intercompany matching, pre-built elimination rules, and system-enforced currency translation rates tackle the root causes of that doubt. They do it by pulling manual intervention out of the steps where errors are most likely to creep in.

When you're assessing financial consolidation software, there are six capabilities that separate tools that merely get the job done from those that actually deliver results:

- Complex group structures: Sub-groups nested within sub-groups, partial ownership chains, and different consolidation methods applied at the same time across various investees.

- Configurable multi-currency translation: Rate setup by entity and rate type, not just a single closing-rate conversion.

- Automated elimination engines: Going well beyond simple intercompany sales to cover unrealised profit in inventory, intercompany loans with accrued interest, and intercompany dividends.

- Complete audit trail: Every journal, adjustment, and elimination tagged with timestamps and user attribution.

- ERP integration: Direct trial balance extraction instead of relying on CSV exports and manual uploads.

- Dual-framework compliance: Full support for both IFRS and US GAAP reporting requirements.

The selection criterion most teams undervalue is how the software deals with mid-period acquisitions and disposals. Think about adding a subsidiary partway through a reporting period. You're looking at pro-rata consolidation of results, goodwill recognition, and NCI allocation from the acquisition date. That's exactly where generic tools fall apart, and it's where specialist platforms genuinely earn their keep.

Moving away from spreadsheets toward specialized platforms isn't really a technology preference thing. It comes down to something more fundamental: can the group's consolidated numbers hold up under scrutiny from auditors, regulators, and the board without anyone needing to reverse-engineer how they were put together?

Frequently Asked Questions About Group Financial Consolidation

What are consolidated financial statements?

Consolidated financial statements merge the financial results of a parent company with all the subsidiaries it controls into a single set of reports. They depict the group as one economic entity, covering a consolidated balance sheet, income statement, cash flow statement, and statement of changes in equity. Before the statements are finalized, all intercompany balances and transactions get eliminated.

How do you consolidate financial statements for multiple entities?

Start by gathering trial balances from every entity, then align accounting policies (depreciation methods, revenue recognition criteria) and reporting periods so you're comparing like with like. Convert any foreign-currency subsidiaries using the correct exchange rates, remove intercompany transactions, recognise goodwill and non-controlling interests, and generate the consolidated output. For a 15-entity group, this typically means hundreds of separate adjustments before the final statements are ready. It's a heavy lift, even for experienced teams.

What is the difference between the equity method and full consolidation?

Full consolidation pulls in 100% of a subsidiary's assets, liabilities, revenues, and expenses, adding them to the parent's figures line by line, with NCI shown separately. The equity method works differently. It records only the investor's share of an associate's net assets and profit as a single line on the balance sheet and income statement. When a parent controls the entity, full consolidation applies. Where the investor holds significant influence, typically between 20% and 50% ownership, the equity method is the right approach.

What is the role of intercompany eliminations in group consolidation?

They stop double-counting. When one subsidiary sells goods to another for £2 million, both entities record that transaction on their books. Skip the elimination step, and group revenue plus cost of goods sold end up overstated by £2 million each.

How are foreign subsidiaries translated for consolidation purposes?

Under IAS 21, balance sheet items get translated at the closing exchange rate, while income statement items use the period's average rate. Equity stays at historical rates from the date of contribution or earning. The gap between these different rates produces what's known as the foreign currency translation reserve, which is recognised in other comprehensive income rather than profit or loss.

What is a non-controlling interest in group financial consolidation?

NCI refers to the slice of a subsidiary's equity held by shareholders outside the parent company. So if a parent owns 75% of a subsidiary, the other 25% is NCI. On the consolidated balance sheet, it's reported as a distinct component within total equity. The subsidiary's profit gets divided between the parent's share and the NCI share in the income statement. Under IFRS 3, you can measure NCI at either fair value or the proportionate share of the subsidiary's net identifiable assets on the acquisition date.

Take Control of Your Group Financial Consolidation

Multi-currency translation, intercompany eliminations, and complex ownership structures don't need to consume your close cycle. Explore Quick Consols' consolidation platform to see how finance teams automate multi-entity group consolidation and produce audit-ready statements without spreadsheet risk.