Stepped Acquisitions (IFRS)

Overview

Not all business acquisitions happen in a single transaction. Businesses often build their ownership over time, starting with a smaller holding percentage and increasing it over time. From an accounting perspective, this is known as a stepped acquisition.

While the concept is straightforward, the accounting treatment under IFRS can be complex, particularly at the point where control is obtained.

What is a stepped acquisition?

A stepped acquisition is when a company gradually increases its ownership in another company over time, eventually gaining control.

Control usually means owning more than 50% of the business or having the power to make key economic decisions.

For example:

Before control is achieved, the investment is typically treated as:

• An associate, or

• A financial asset

Once control is achieved, the entity becomes a subsidiary.

How the Accounting Changes

Under IFRS 3 (Business Combinations), gaining control is treated as a significant economic event.

“An acquirer shall recognize goodwill as of the acquisition date” (IFRS 3.32)

“The acquisition date is the date on which the acquirer obtains control of the acquiree” (IFRS 3.8)

At the point of control, the transaction is accounted for as if the entire business is acquired on that date. This is why previously held interests must be reassessed.

Accounting at the Point of Control

There are three key steps to apply:

1. Remeasure previously held Interest

The existing investment must be remeasured to fair value.

“Ina business combination achieved in stages, the acquirer shall remeasure its previously held equity interest at its acquisition-date fair value” (IFRS 3.42)

- Increase in value → recognize a gain

- Decrease in value → recognize a loss

Impact: Recorded in profit or loss.

2. Recognize the entire business

Once control is achieved:

- Recognize 100% of assets and liabilities

- Prepare consolidated financial statements

“The acquirer shall recognize, separately from goodwill, the identifiable assets acquired and the liabilities assumed” (IFRS 3.10)

Anon-controlling interest (NCI) is recognized for any portion not owned.

3. Calculate Goodwill

Goodwill is calculated as:

Goodwill= Total Consideration – Net Identifiable Assets

“Goodwill is measured as the excess of (a) over (b)” (IFRS 3.32)

Where total consideration includes:

- New investment

- Fair value of previously held interest

In simple terms: Goodwill represents what you paid above the value of the underlying assets, often for things like a brand, customers, or future growth.

Example

Scenario:

· Initial 30% acquired for R300,000

· Additional 40% acquired for R500,000

· Fair value of initial stake at control date: R450,000

· Net assets: R800,000

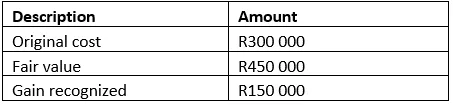

Step 1: Remeasure Existing Interest

The initial investment increased from R300,000 to R450,000.

You will recognise a R150,000 gain in profit or loss.

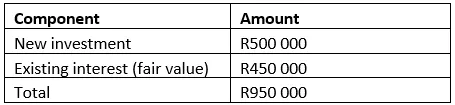

Step 2:Total Consideration

Even though you only paid an additional R500 000 now, IFRS treats your total investment as R500 000 +R450 000 = R950 000

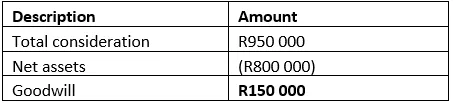

Step 3: Goodwill Calculation

You paid R950,000 for a business with identifiable net assets of R800,000. The difference

R150 000is recognized as goodwill.

Additional Note – If consideration is less than NAV

Sometimes, instead of paying more than the value of the business, you end up paying less.

This results in what IFRS calls a bargain purchase gain.

In simple terms:

- If Total Consideration < Net Identifiable Assets

- The difference is recognised as a gain in profit or loss

"If the acquirer’s interest in the net fair value of the identifiable assets and liabilities exceeds the consideration transferred, the acquirer shall recognise the resulting gain in profit or loss" (IFRS 3.34)

Why this happens: This is less common, but it can occur where:

- The seller is under pressure to exit

- The business is distressed

- There is a particularly favourable deal negotiated

Important to note: Before recognising the gain, IFRS requires you to reassess all measurements to make sure nothing has been misstated. In other words, if it looks like a “too good to be true” deal, you need to double-check your numbers first.

Key Takeaways

· Remeasure previously held interests (IFRS 3.42)

· Using fair value and not historical cost

· Goodwill calculations must include prior holding value

· Omitting gains or losses from profit or loss

· The critical point is when control is achieved

· At that point:

o Remeasure existing investment (IFRS3.42)

o Consolidate the full business (IFRS3.10)

o Calculate goodwill (IFRS 3.32)

Final Thought

Stepped acquisitions reflect a core IFRS principle: substance over form.

Although ownership increases over time, the financial reporting resets at the point control is obtained. You may have invested over time, but once control is achieved, IFRS treats it as a new starting point.