How to Eliminate Intercompany Transactions in Consolidation

A group accountant at a 15-entity conglomerate stared at consolidated revenue that looked 22% higher than external sales actually warranted. Three subsidiaries had been trading with each other all quarter, and nobody had stripped those internal transactions out before rolling up the numbers.

That scenario captures the exact problem intercompany eliminations solve. When entities within the same group buy from, lend to, or pay dividends to each other, both sides record the transaction. Left unchecked, those entries double-count revenue, expenses, assets, and liabilities on the consolidated financial statements. The group ends up reporting activity that never involved an outside customer, lender, or supplier. Regulators, auditors, and investors all see a distorted picture.

Intercompany eliminations strip away every internal transaction so the consolidated statements reflect only what the group did with the rest of the world. Under both IFRS 10 and US GAAP ASC 810, full elimination of intragroup balances and transactions is mandatory for controlled subsidiaries. Wolters Kluwer classifies these eliminations into three broad categories: intercompany debt, intercompany revenue and expenses, and intercompany stock ownership.

The types of transactions you'll need to eliminate include:

- Sales and purchases between group entities (and any unrealised profit sitting in inventory)

- Intercompany loans and interest charges

- Dividends declared by a subsidiary and received by the parent

- Payables and receivables arising from intragroup trading

- Transfers of fixed assets where the selling entity recorded a gain or loss

This walkthrough covers the full elimination process from start to finish: reconciling intercompany balances, posting elimination journal entries for each transaction type, handling NCI allocations, managing multi-level group structures, and addressing the IFRS vs. US GAAP differences that catch teams off guard during audit season. Each step includes worked numerical examples with debit-and-credit entries you can adapt to your own consolidation workbook.

What Are the Prerequisites Before You Begin Intercompany Eliminations?

Before posting any elimination entries, finance teams need finalised subsidiary trial balances, a uniform chart of accounts, aligned reporting periods, and consistently tagged intercompany codes across all entities.

Skipping straight to elimination journal entries before the underlying data is clean is the fastest way to create a consolidation that doesn't balance. Every prerequisite below exists to prevent a specific failure mode during the close.

Start with subsidiary trial balances. Each entity's numbers must be finalised, reviewed, and imported into your consolidation workbook or consolidation software before any elimination work begins. Partial or draft trial balances introduce moving targets; you'll eliminate a balance that changes two days later, forcing rework.

Next, confirm your chart of accounts mapping. Subsidiaries acquired at different times, or operating in different jurisdictions, almost always use different account structures. A parent might book intercompany sales under account 4100 while the subsidiary records the corresponding purchase under 5200. Without a group-wide mapping table that links these accounts, your elimination entries won't offset correctly. Intuit's enterprise finance guidance recommends a one-page group policy mandating uniform account codes and formats across all subsidiaries to prevent exactly this kind of mismatch.

Reporting period alignment is non-negotiable. If one subsidiary reports through 31 March and another through 28 February, the intercompany balances won't agree. IFRS 10 permits a maximum three-month difference between subsidiary and parent reporting dates, but even a one-month gap introduces timing variances that complicate reconciliation.

Consistent intercompany tagging deserves its own emphasis. Every intercompany transaction should carry a standard identifier (something like "IC-SALE" or "IC-LOAN") so you can extract all intragroup activity in seconds rather than hunting through general ledger detail. SAP's Group Reporting module, for instance, relies on two-sided intercompany data matched in group currency after foreign currency translation; without clean tagging, that matching step fails.

A written group intercompany policy should mandate that both sides of every intercompany transaction use the same reference, amount, and posting period. When the paying entity records an invoice, the receiving entity should record it simultaneously. Policies that allow "we'll true it up at month-end" are the root cause of most reconciliation headaches.

Get these foundations right and the elimination entries themselves become mechanical. Get them wrong and you'll spend more time investigating differences than actually consolidating.

Step 1: How Do You Reconcile Intercompany Balances Before Elimination?

Intercompany reconciliation aligns receivables with payables, revenue with cost of sales, and loan balances across entities. It resolves variances driven by timing differences, FX rates, or unrecorded items before elimination entries are posted.

You can't eliminate what doesn't match. Say Entity A reports a $500,000 intercompany receivable, but Entity B only shows a $485,000 payable. A standard elimination entry won't fix that. It just leaves a $15,000 orphan sitting on your consolidated balance sheet. Reconciliation catches these gaps before they turn into audit findings.

Most teams only reconcile intercompany balances at period end. That's a mistake. Reconciling continuously throughout the month works far better because it catches mismatches while transactions are still recent and the people who posted them actually remember what happened. Wait until close week, and you're stuck investigating stale entries under intense time pressure. Tracking down explanations at that point becomes significantly harder.

The reconciliation process follows a consistent order. Pull all intercompany-tagged balances from each entity's trial balance. Place them next to each other, categorized by counterparty and transaction type. Examine every discrepancy, regardless of size (a $200 rounding error in January turns into a $2,400 annualized problem by December). Record how each difference was resolved, whether it's a timing entry, an FX retranslation, or a genuinely missing transaction that one party neglected to book.

Four causes explain most intercompany mismatches:

- Timing differences: Entity A posts a sale on 29 March. Entity B doesn't record the purchase until 2 April

- FX rate discrepancies: Entities working in different functional currencies end up translating the same transaction at different spot rates, or on entirely different dates

- Unrecorded transactions: One entity books the invoice. The counterparty never receives it or simply doesn't record it

- Cut-off inconsistencies: Subsidiaries running on slightly different close calendars will capture different transaction populations

A reconciliation schedule puts these variances right in front of you:

That $12,000 revenue/COGS variance in the table above is a classic FX problem. Entity A reported revenue in USD. Entity B recorded cost of sales in EUR, converting at a marginally different rate. The fix? Agree on a uniform translation rate for intercompany transactions, or book a consolidation adjustment for the difference. Neglecting to resolve these common consolidation mistakes before posting eliminations creates imbalances that ripple through your entire consolidation package.

When every line balances to zero (or ties to a documented difference with a matching adjustment), you're in a position to post elimination entries with confidence.

Step 2: How Do You Eliminate Intercompany Payables, Receivables, and Loans?

Intercompany payables and receivables eliminate by debiting the payable and crediting the receivable for the matched amount, netting both balances to zero on the consolidated balance sheet.

Balance sheet eliminations are the most mechanical step in the consolidation process. Once reconciliation confirms that Entity A's intercompany receivable equals Entity B's intercompany payable, the journal entry is straightforward: debit the payable, credit the receivable, and both disappear from the group's consolidated position. The same logic applies to intercompany loans.

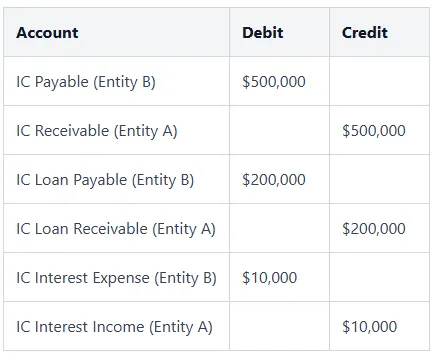

Consider a practical scenario. Subsidiary A lends $200,000 to Subsidiary B at 5% annual interest. At the reporting date, A holds a $200,000 loan receivable plus $10,000 in accrued interest income. B carries a $200,000 loan payable and $10,000 in accrued interest expense. From the group's perspective, no money left the organisation. Every dollar of that loan and every dollar of that interest charge must be removed.

The full set of elimination entries looks like this:

The payable/receivable elimination ($500,000) addresses the trading balance from the reconciliation example in the previous section. The loan and interest entries handle the financing arrangement separately. Keeping these entries distinct rather than lumping everything into one journal makes audit trails cleaner and rollforward schedules easier to maintain.

Currency translation creates the one real complication in this otherwise simple step. When Entity A reports in USD and Entity B reports in GBP, both sides translate the intercompany balance into the group's presentation currency. But they rarely use identical rates. Entity A might translate its receivable at the closing rate on 31 December, while Entity B translates its payable using a rate sourced from a different provider or timestamped slightly differently.

The resulting FX difference doesn't just vanish. You need to park it somewhere. Standard practice under IFRS is to recognise the translation variance in the foreign currency translation reserve (FCTR) within other comprehensive income. The entry typically debits or credits the FCTR for the residual amount after the intercompany balances are eliminated. Groups that skip this step end up with a consolidation that doesn't balance, and the out-of-balance amount grows every period as exchange rates move.

One pattern that trips up even experienced teams: intercompany loans denominated in a currency that's neither entity's functional currency. A USD-functional parent lends EUR to a GBP-functional subsidiary. Both entities revalue the loan through their own P&L for FX movements, but the group elimination needs to reverse both revaluation entries and recognise only the net FX impact at the consolidated level. If you encounter this, map out all three currencies on paper before touching the consolidation entries. It saves time.

Once payables, receivables, loans, and interest are eliminated, the consolidated balance sheet and income statement carry only third-party positions. The next step tackles the trickier profit and loss eliminations where unrealised margin enters the picture.

Step 3: How Do You Eliminate Intercompany Revenue, Cost of Sales, and Unrealised Profit?

Intercompany revenue eliminates against intercompany cost of sales, and any profit on goods still held in group inventory at period end requires a separate unrealised profit elimination entry.

Removing intercompany revenue and expenses is more nuanced than eliminating balance sheet items because you're dealing with two distinct problems: the gross transaction and the embedded margin. Miss the second one and your consolidated inventory is overstated.

The gross elimination is simple. If a parent sold $600,000 of goods to its subsidiary during the quarter, the parent recorded $600,000 in revenue and the subsidiary recorded $600,000 in cost of sales (assuming the subsidiary has since sold the goods externally). The elimination entry reverses both:

The second pair of entries in that table is where the real complexity lives. Here's the worked example.

The parent manufactures goods at a cost of $420,000 and sells them to the subsidiary for $600,000, earning a 30% gross margin. The remaining 40% ($240,000 at transfer price) sits in the subsidiary's warehouse. The subsidiary resells 60% of those goods to external customers by period end.

From the group's perspective, that inventory cost $420,000 × 40% = $168,000 to produce. But the subsidiary's books show it at $240,000 (the intercompany purchase price). The difference of $72,000 is unrealised profit that exists only because of the internal transaction. It hasn't been earned through a sale to an outside party, so it must be stripped out of consolidated inventory.

The calculation: $240,000 transfer price × 30% margin = $72,000 unrealised profit. Debit cost of sales (or retained earnings, if the sale occurred in a prior period) and credit inventory for $72,000.

TRG International's consolidation guidance draws an important distinction between downstream and upstream transactions that directly affects NCI. In a downstream sale (parent sells to subsidiary), the parent initiated the transaction and earned the margin, so the full unrealised profit adjustment hits the parent's share of consolidated equity. NCI isn't touched.

Upstream transactions flip the analysis. When the subsidiary sells to the parent, the subsidiary earned the margin. If the parent owns only 80% of that subsidiary, the unrealised profit adjustment must be split: 80% allocated to the parent and 20% to NCI. Forgetting this allocation is one of the most common errors in group consolidations with partially owned subsidiaries. Auditors check for it specifically.

The upstream/downstream distinction matters even more than most guides suggest. In a group with multiple tiers of partial ownership, a single upstream sale can require NCI adjustments at every level of the ownership chain. Groups with three or more consolidation layers should map the ownership waterfall before calculating the split.

For groups running dozens or hundreds of intercompany product lines, tracking which goods remain in inventory at period end becomes a data problem as much as an accounting one. Inventory subledgers need to flag intercompany-sourced stock separately, with the original transfer price and the seller's cost attached. Without that granularity, calculating unrealised profit at scale requires manual inventory analysis that can consume days of close time.

Teams using cloud-based consolidation software can automate the unrealised profit calculation by maintaining transfer pricing rules and inventory aging data within the consolidation layer, reducing the manual extraction work significantly. The journal entries still follow the same logic; the difference is speed and accuracy at volume.

Step 4: How Do You Eliminate Intercompany Dividends and Equity Investments?

Intercompany dividends are removed by debiting the parent's dividend income and crediting the subsidiary's dividends declared. The equity investment elimination then offsets the parent's investment against the subsidiary's net assets, effectively zeroing out both sides of the transaction.

Dividend elimination is straightforward in concept, but it sits right where two broader consolidation entries overlap, and that's where teams get tripped up: the dividend entry itself and the acquisition (equity) elimination. Both need to be posted. They interact with each other through retained earnings, which is exactly why getting one wrong can quietly break the other.

Start with dividends. Say a subsidiary declares a $60,000 dividend and the parent holds 100% of its shares. The parent booked $60,000 as dividend income; the subsidiary reduced retained earnings by $60,000. From the group's perspective, cash simply shifted from one pocket to another. The elimination entry clears both sides:

- Debit Dividend Income (Parent): $60,000

- Credit Dividends Declared (Subsidiary): $60,000

When the parent holds less than 100%, only its share of the dividend gets eliminated. At 75% ownership, the parent recorded $45,000 in dividend income ($60,000 × 75%). The remaining $15,000 paid to outside shareholders isn't intercompany. It's a real cash outflow from the group and stays in the consolidated statements.

Equity investment elimination is more complex. On the parent's standalone balance sheet, the subsidiary investment shows up as a single-line asset. Over on the subsidiary's side, that same value is reflected through share capital, retained earnings, and other reserves. Consolidation swaps out the parent's investment line for the subsidiary's actual assets and liabilities, then removes the equity duplication entirely.

Assume the parent company paid $500,000 for 80% of a subsidiary with net assets of $400,000 at acquisition. The parent's 80% share of those net assets comes to $320,000. That leaves a surplus of $180,000, which represents goodwill. NCI at acquisition is 20% × $400,000 = $80,000 (applying the proportionate share method).

The equity accounting entry on consolidation:

The dividend elimination and equity elimination appear together here because they both hit the subsidiary's retained earnings. Plenty of teams post them as separate journals for clarity, and that's fine. What matters is that the net effect on retained earnings reconciles.

Goodwill from acquisitions sits on the consolidated balance sheet and gets tested for impairment each year under IFRS (IAS 36), or at the reporting unit level under US GAAP (ASC 350). It's not eliminated. It's monitored.

NCI doesn't stop mattering after the acquisition date. Every subsequent reporting period, you split the subsidiary's post-acquisition profits and losses between the parent's share and NCI according to ownership percentages. Say the subsidiary earned $50,000 after acquisition and NCI holds 20%. That means $10,000 of the profit belongs to NCI. This allocation shows up on the consolidated income statement as "profit attributable to non-controlling interests" and bumps up the NCI balance on the consolidated balance sheet.

Groups with multiple subsidiaries at different ownership levels repeat this process for every entity. The mechanics stay the same. But the volume of entries ramps up fast, so a structured elimination schedule becomes critical if you want to keep your consolidation package audit-ready.

Step 5: How Do Multi-Level Group Structures Affect Intercompany Eliminations?

Multi-level group structures demand sequential, bottom-up elimination across three tiers: sub-group, intermediate parent, and ultimate parent. NCI compounds at each level.

Most consolidation guides assume a flat parent-subsidiary structure. Real groups don't look like that. Picture a holding company that owns 80% of an intermediate parent, which owns 75% of an operating subsidiary, which itself holds 60% of a joint venture entity. Every tier brings its own intercompany transactions, and each one requires elimination before the numbers can roll up properly.

The method Oracle outlines in its Financials Cloud platform splits this into three separate tiers. Level 1 clears out transactions within the lowest sub-group: if two sister subsidiaries traded with each other, those entries get resolved right here. Level 2 rolls that sub-group into its intermediate parent, wiping out any transactions between the sub-group and the intermediate entity. The Corporate level then folds the intermediate parent into the ultimate parent, capturing whatever intercompany activity remains.

Always work bottom-up. Completing eliminations at the lowest tier first prevents double-counting when those numbers feed into the next level. If you start at the top and work down, you'll miss embedded intercompany balances that only become visible once sub-group consolidation is complete.

Two approaches exist for managing multi-level structures:

- Direct method: Every subsidiary consolidates straight into the ultimate parent in one step. It's simpler to execute, but it ignores sub-group reporting requirements and can make it hard to trace where intercompany activity originates.

- Indirect (sequential) method: Each sub-group consolidates first, then feeds into the next tier up. This preserves sub-group financial statements for local regulatory filings and gives controllers clear visibility into elimination entries at each level.

- NCI compounding: Under the indirect method, NCI at each tier multiplies. Say the ultimate parent owns 80% of the intermediate parent, and that intermediate parent owns 75% of the operating subsidiary. The group's effective interest in the subsidiary comes out to 60% (0.80 × 0.75). The remaining 40% splits between NCI attributable to the intermediate parent's outside shareholders and NCI attributable to the subsidiary's outside shareholders.

- Upstream profit allocation: Unrealised profit on transactions from a lower-tier subsidiary to a higher-tier parent must be split according to the effective ownership percentage at that level, not the direct holding.

The direct method gets recommended a lot because it's faster. But the indirect method catches elimination errors sooner, since every sub-group has to balance on its own before rolling up. Groups with three or more tiers that skip sequential consolidation often don't spot mismatches until they reach the ultimate parent level, where tracing the source becomes a real headache.

For groups with multi-tier ownership structures, Quick Consols handles this sequential consolidation automatically, applying elimination rules at each level and calculating effective NCI percentages across the entire group.

How Does IFRS 10 Compare to US GAAP ASC 810 for Intercompany Eliminations?

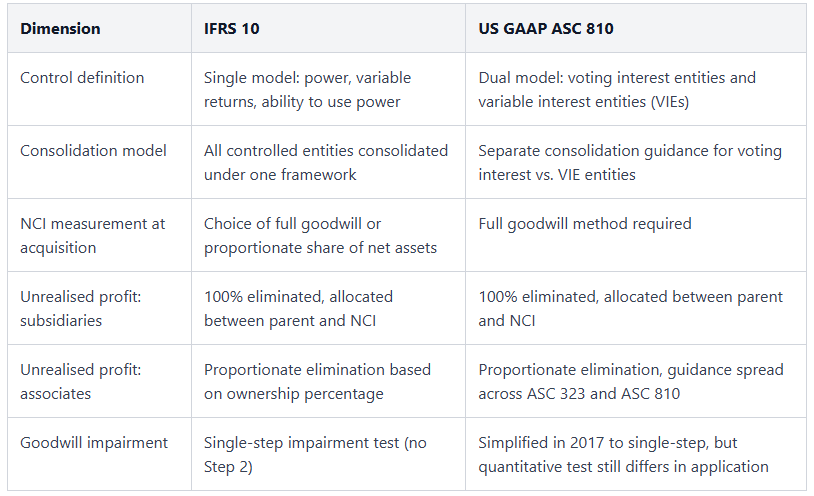

IFRS 10 and US GAAP ASC 810 both mandate full elimination of intercompany transactions for subsidiaries. Where they diverge is in how they define control, measure NCI, and handle associate treatment.

The elimination entries look the same under both frameworks: debit intercompany revenue, credit intercompany cost of sales, remove intercompany receivables against payables. Where the two standards actually diverge is in deciding which entities need full consolidation and how you measure the portion that belongs to outside shareholders.

IFRS 10 defines control through a single framework resting on three pillars: power over the investee, exposure to variable returns, and the ability to use that power to influence those returns. ASC 810 takes a different approach, splitting this into two separate tests. Voting interest entities consolidate when the parent holds a majority of voting rights. Variable interest entities (VIEs) consolidate when the parent is the primary beneficiary, absorbing most of the expected losses or receiving the majority of expected residual returns. Because of this dual-model structure, an entity that wouldn't require consolidation under IFRS could very well trigger VIE consolidation under US GAAP, or the reverse.

The practical gap gets bigger with associates. IFRS requires proportionate elimination of transactions between a group and its associate (accounted for under the equity method), based on the group's ownership percentage. Sell $100,000 of goods to a 30%-owned associate, and you're eliminating $30,000 of the unrealised profit. US GAAP takes a comparable approach for equity method investees, but the specific guidance is scattered across multiple codification topics rather than sitting in a single standard. Teams managing NCI calculations under both frameworks need to track these distinctions with care.

For dual-reporting groups that prepare consolidated financial statements under both frameworks, the control assessment is where you start. One entity consolidated under a single framework but not the other produces two distinct consolidation scopes, and that means two different sets of elimination entries. Get the scope wrong, and the error cascades through every step that follows.

Step 6: How Can You Automate Intercompany Eliminations to Reduce Errors and Save Time?

Consolidation software with rule-based elimination engines can reduce intercompany reconciliation time by 80-90%, replacing manual spreadsheet processes with automated matching and journal generation.

Spreadsheet-based eliminations break in predictable ways. A formula references the wrong cell after someone inserts a row. Two controllers work on different versions of the same workbook. An elimination entry from last quarter gets pasted into this quarter's file without updating the amounts. None of these errors announce themselves; they sit quietly in the consolidated numbers until an auditor finds them.

The workflow in financial consolidation software follows a different pattern entirely. You connect each entity's accounting platform, whether that's Xero, QuickBooks, or Sage, and the system imports trial balances automatically. Intercompany accounts are tagged during initial setup, usually by mapping them to a dedicated account range or applying intercompany partner codes. From that point, the software handles the heavy lifting.

Once trial balances land, the system matches intercompany receivables against payables across all entities simultaneously. Matched pairs generate elimination journal entries without manual intervention. Unmatched items surface as exceptions for the consolidation team to investigate. The entire process, from data import to draft elimination entries, can run in minutes rather than the days it takes in a spreadsheet environment.

The complexity argument actually strengthens the case for automation. A group with 15 subsidiaries across 4 currencies generates hundreds of intercompany line items each month. Manual matching at that scale isn't just slow; it's where the highest-risk errors hide. Rule-based engines apply the same logic every period without fatigue, and they flag anomalies that a tired accountant scrolling through row 847 of a spreadsheet would miss.

According to Wolters Kluwer's consolidation guidance, enforcing double-entry logic within the consolidation system prevents one-sided entries, one of the most common causes of out-of-balance consolidations. Every elimination debit has a corresponding credit, validated before posting.

The audit trail matters just as much as the speed gain. Each auto-generated elimination entry links back to the source transactions in both entities, the matching rule that triggered it, and the user who approved it. Auditors can trace any consolidated line item from the group financial statements down to the original intercompany invoice without requesting a separate reconciliation workpaper.

What Are the Most Common Mistakes in Intercompany Eliminations, and How Do You Avoid Them?

Most intercompany elimination failures come down to six repeat offenders: skipped reconciliation, unrecognized unrealised profit, FX mismatches, incorrect NCI allocation, misclassified associates, and weak documentation.

Bypassing reconciliation before you post elimination entries is the quickest way to throw your consolidated trial balance out of whack. Say Entity A records a $150,000 receivable, but Entity B only shows $140,000 payable because B hasn't posted the latest invoice. Eliminating the full $150,000 leaves a $10,000 hole. The fix is straightforward: require that intercompany reconciliation is finalized, with all differences investigated, before anyone drafts an elimination journal. Add a formal sign-off step to your close checklist.

Overlooking unrealised profit on assets still held within the group is more nuanced, and it's frequently caught only during audit. Earlier sections covered inventory, but the same principle holds for fixed assets. Say a subsidiary sold equipment to its parent at a $50,000 markup. That profit stays embedded in the parent's depreciation base until the asset is fully depreciated or sold externally. The right preventive control here is a fixed asset intercompany register that tracks every intra-group transfer and its remaining unrealised margin. For guidance on how this differs for intercompany transactions with associates, the proportionate elimination rule applies rather than full elimination.

FX mismatches catch out groups where two entities transact in different functional currencies. Entity A records the intercompany balance at the EUR closing rate, while Entity B records it at the GBP closing rate. The underlying transaction amount may have matched perfectly at inception, but exchange rate movements will create a gap by reporting date. Don't try to force-match the balances. That's not the fix. Instead, translate both sides at the same rate (typically the closing rate per group policy), post any resulting FCTR difference to equity, and then eliminate the translated amounts.

Assigning all upstream unrealised profit to the parent while ignoring NCI's portion underrepresents the minority interest on the balance sheet. If a 70%-owned subsidiary sells goods to the parent at a margin, 30% of that unrealised gain belongs to NCI. The elimination entry needs to be split accordingly.

Documentation failures won't blow up your numbers right away, but they'll trigger audit delays that cost just as much. Every elimination entry needs to cite the matching report, the intercompany account codes, and the approval. If auditors can't trace an entry from the consolidated financial statements back to source transactions, they'll issue a finding. It doesn't matter whether the numbers are actually correct.

Frequently Asked Questions About Intercompany Eliminations in Consolidation

What are intercompany eliminations in consolidation?

Intercompany eliminations are consolidation adjustments that strip out the financial effects of transactions between entities within the same corporate group. Their purpose is straightforward: consolidated financial statements should reflect only transactions with external third parties. Without these adjustments, revenue, expenses, assets, and liabilities get double-counted across the group, distorting the true financial picture.

Why are intercompany eliminations required for accurate financial reporting?

Without them, a parent selling $1 million of goods to its subsidiary would book $1 million in group revenue that never actually left the organisation. Revenue, receivables, and payables on the consolidated statements would all be inflated, giving investors and regulators a distorted picture of the group's real economic activity.

What types of intercompany transactions need to be eliminated?

All intra-group transactions: sales and purchases, loans and accrued interest, dividends, management fees, payables and receivables, and unrealized profit on inventory or fixed assets that remain within the group at the reporting date.

How do you handle intercompany eliminations for partially-owned subsidiaries?

100% of the intercompany transaction still eliminates. The subtlety sits in how you allocate unrealised profit. For upstream transactions (subsidiary sells to parent), the unrealised margin gets split between the parent's share and NCI according to ownership percentages. So a 70%-owned subsidiary's unrealised profit? That's 70% to the parent, 30% to NCI.

What happens when intercompany balances don't match during reconciliation?

Timing differences are behind most mismatches: one entity posted the invoice, the other hasn't yet. FX rate discrepancies and unrecorded transactions explain the rest. You need to investigate and resolve every difference before posting elimination entries. Leave a $5,000 mismatch unresolved, and the consolidated balance sheet will be out of balance by exactly that amount.

Can consolidation software automate intercompany elimination entries?

Yes. Rule-based consolidation platforms auto-generate elimination journals by matching tagged intercompany accounts across entities. They handle multi-currency translation, compute NCI splits, and keep a full audit trail that links every elimination back to its source transactions.

Simplify Your Intercompany Eliminations with Quick Consols

Manual intercompany eliminations drain hours from every close cycle while leaving your group financials exposed to errors auditors will find. Quick Consols automates the entire elimination workflow, from intercompany matching through multi-currency translation to audit-ready consolidated reporting. Book a demo to see how Quick Consols automates consolidation.