How to Prepare Consolidated Financial Statements

How do you present ten subsidiaries across four countries as one coherent financial story to auditors, investors, and regulators?

Consolidated financial statements answer that question. They merge the parent company's financials with every subsidiary it controls into a single set of reports: a consolidated balance sheet, income statement, and cash flow statement. The group appears as one economic entity, even when the legal structure spans dozens of companies.

Under IFRS 10, control exists when the parent holds more than 50% of voting rights or has power over the investee's relevant activities, exposure to variable returns, and the ability to use that power to affect those returns. That definition catches arrangements many groups overlook, including structured entities where voting rights alone don't tell the full story.

Not every parent entity is required to consolidate. IFRS 10.4 provides an intermediate parent exemption: if your parent is itself a wholly owned (or partially owned, with no shareholder objection) subsidiary of another entity that publishes IFRS-compliant consolidated statements, you can skip preparing your own group accounts. Other exemptions apply to investment entities that measure subsidiaries at fair value through profit or loss.

The steps below walk through the practical process, with worked examples covering intercompany eliminations, goodwill, NCI calculations, and the consolidation worksheet structure finance teams actually use during the close.

Step 1: How Do You Gather and Align Subsidiary Data?

Consolidated statements require uniform trial balances, aligned reporting dates, standardised accounting policies, and foreign currency translation across every group entity before any consolidation work begins.

The first bottleneck in any consolidation cycle isn't the elimination entries or goodwill calculations. It's getting clean, comparable data from every subsidiary on time.

Start by collecting each entity's trial balance for the same reporting period. If a subsidiary's year-end doesn't match the parent's, IFRS allows a maximum three-month gap, but you'll need to adjust for significant transactions that occurred between the two dates. Most groups push subsidiaries to report on the parent's date to avoid these complications.

Next, standardise the chart of accounts. Subsidiary A might book freight costs under "distribution expenses" while Subsidiary B buries them in "cost of sales." These mapping mismatches cascade through the consolidated income statement if you don't catch them early. Align accounting policies too: depreciation methods, revenue recognition timing, and inventory valuation must be consistent before you combine the numbers. When choosing between ERP and consolidation software, this policy alignment step is where dedicated tools pull ahead.

For groups with foreign subsidiaries, translate balance sheet items at the closing exchange rate and income statement items at the average rate for the period. The resulting foreign currency translation reserve (FCTR) sits in equity and captures the exchange differences.

Before moving to eliminations, confirm you have: trial balances for every entity, intercompany transaction schedules with matching balances, ownership records showing percentage held, and the FX rates used for translation. Missing any one of these stalls the entire consolidation.

Step 2: How Do You Eliminate Intercompany Transactions and Calculate Goodwill?

Intercompany eliminations remove intra-group sales, receivables, payables, dividends, and unrealised inventory profits so the consolidated statements reflect only external transactions.

Once subsidiary data is aligned, the real consolidation work begins: stripping out every transaction that occurred between group entities. If the parent sold $100,000 of goods to a subsidiary during the year, that revenue and corresponding cost of sales must be cancelled. The group didn't generate income by moving goods between its own pockets.

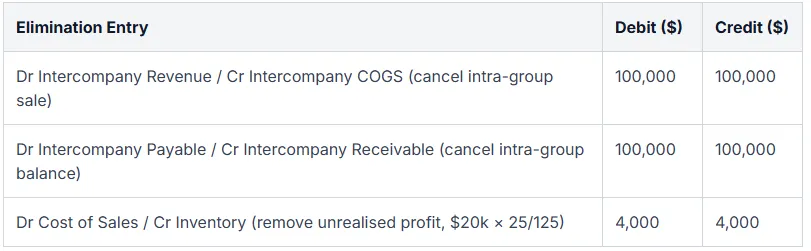

The trickier adjustment involves unrealised profit sitting in inventory at year-end. Suppose $20,000 of that intercompany inventory remains unsold by the subsidiary, and the parent applied a 25% markup on cost. The unrealised profit is $20,000 × 25/125 = $4,000. You debit cost of sales and credit inventory to remove that $4,000 from the consolidated balance sheet. Some practitioners mistakenly apply the margin to the selling price rather than grossing up from cost, which inflates the elimination. For a deeper walkthrough with multi-step scenarios, see this guide on intercompany eliminations.

A consolidation worksheet for these entries looks like this:

After eliminations, calculate goodwill on each acquisition. The formula: consideration paid by the parent, minus the parent's share of the subsidiary's net assets at fair value on the acquisition date. If the parent paid $800,000 for 80% of a subsidiary whose net assets had a fair value of $900,000, goodwill equals $800,000 minus (80% × $900,000) = $80,000. Fair valuing the subsidiary's assets at acquisition is critical here. Land, customer lists, and brand names often carry values well above book, and missing these adjustments understates goodwill while overstating post-acquisition profits through lower depreciation and amortisation charges.

As ACCA Global's consolidation guidance notes, intra-group current account balances must also be cancelled. Even a $500 mismatch between the parent's receivable and the subsidiary's payable will prevent the consolidated balance sheet from balancing, and tracking down that difference at midnight before a filing deadline is exactly as painful as it sounds.

Step 3: How Do You Record Non-Controlling Interests and Complete the Worksheet?

Non-controlling interest (NCI) represents the subsidiary equity percentage not held by the parent, reported separately within consolidated equity on the balance sheet.

Take a parent that owns 80% of a subsidiary with net assets of $500,000 at the reporting date. NCI equals 20% × $500,000 = $100,000. That $100,000 appears as a separate line within equity on the consolidated balance sheet, and the NCI's share of the subsidiary's profit or loss shows up on the face of the consolidated income statement. You include 100% of the subsidiary's assets, liabilities, revenue, and expenses in the group figures, then carve out the minority's slice through these NCI entries.

The consolidation worksheet that brings all of this together typically has four columns: parent figures, subsidiary figures, adjustments and eliminations, and the consolidated total. You populate it line by line. Cash from the parent column plus cash from the subsidiary column, minus any eliminated intercompany cash movements, gives you consolidated cash. Repeat for every balance sheet and income statement line. The adjustments column captures everything covered in the previous steps: intercompany eliminations, unrealised profit removals, goodwill recognition, fair value uplifts, and NCI allocation.

Building this worksheet in spreadsheets breaks down past five or six entities. Formula chains become brittle, version control disappears, and a single mislinked cell can misstate consolidated equity without triggering any obvious error. Groups managing ten or more subsidiaries across multiple currencies find that a practical consolidation guide built around dedicated software cuts days from the close while reducing the risk of undetected mistakes.

Once the worksheet is complete, verify the fundamental equation: consolidated assets must equal consolidated liabilities plus parent equity plus NCI. If the balance sheet doesn't balance, the most frequent culprits are a missed intercompany elimination, an NCI percentage applied to the wrong net asset figure, or a foreign currency translation entry that landed in the wrong period. Work backwards from the out-of-balance amount; it almost always ties to a specific adjustment.

Step 4: Why Should You Automate the Consolidation Process?

Automating consolidation eliminates spreadsheet formula errors, version control failures, and missing audit trails that cost finance teams days of rework each reporting cycle.

Building a master Excel workbook with linked tabs and manual elimination columns works until it doesn't. Past five entities across multiple currencies, a single broken cell reference can cascade through your entire consolidated balance sheet without anyone noticing until the auditors flag it.

The shift toward financial consolidation software isn't about replacing accounting judgment. It's about removing mechanical grunt work that shouldn't require judgment in the first place. Automated platforms handle:

- Intercompany matching and elimination journals, flagging mismatches before they become reconciliation headaches

- Foreign currency translation at closing and average rates, with the FCTR posting automatically to other comprehensive income

- NCI calculations that update in real time as subsidiary net assets change

- Trial balance imports pulled directly from accounting platforms like Xero and QuickBooks, so nobody is copying and pasting CSVs at midnight on day five of the close

Automation doesn't change your accounting policies or consolidation methodology. It stops you from losing hours to data wrangling that a machine handles in minutes, freeing the team for variance analysis, segmental reporting, and actually understanding what the numbers mean.

Frequently Asked Questions

Who is responsible for preparing consolidated financial statements?

The parent company's management bears ultimate responsibility. In practice, the group financial controller owns the consolidation process end to end, coordinating subsidiary data submissions, reviewing elimination entries, and preparing the final pack. External auditors then review the consolidated statements for compliance with applicable standards.

What is the difference between consolidation under IFRS and GAAP?

IFRS uses a single control-based model: power over the investee plus exposure to variable returns. US GAAP splits the analysis into a voting interest model for most entities and a separate variable interest entity (VIE) model for structured entities. Presentation differences exist in areas like NCI placement and goodwill impairment testing, but both frameworks require combining 100% of subsidiary assets, liabilities, and results.

When is a parent company exempt from preparing consolidated financial statements?

A parent can skip consolidation if it's a wholly-owned subsidiary (or partially-owned with unanimous shareholder consent), its securities aren't publicly traded, and its ultimate parent already publishes compliant consolidated statements.

How do you handle foreign subsidiaries in consolidation?

Translate income statement line items at the average exchange rate for the period and balance sheet items at the closing rate on the reporting date. The difference flows into the foreign currency translation reserve within other comprehensive income, not through profit or loss. This reserve can become material quickly for groups with subsidiaries in volatile currency markets.

What is a consolidation worksheet and why is it important?

It's a structured working paper with columns for the parent, each subsidiary, adjustment entries, and final consolidated figures. The worksheet creates a clear audit trail showing exactly how intercompany balances, unrealised profits, and NCI were treated, which is precisely what auditors request first during the annual review.

Simplify Your Next Group Consolidation

Aligning trial balances, posting elimination journals, and calculating NCI across multiple entities doesn't have to consume your month-end. Explore how Quick Consols simplifies group consolidations by connecting directly to Xero and QuickBooks and producing audit-ready consolidated statements without the spreadsheet chaos. Book a demo to see it in action.