This article was written by Steven Auf, CEO and founder of Quick Consols

How to calculate foreign currency translation reserve(FCTR)

In this guide we’ll give you a complete run down of why we calculate FCTR and exactly how to go about doing it right.

What is FCTR?

FCTR is purely a book entry (journal) processed on the balance sheet when converting any company’s results into another currency. Accountants have decided that different line items on your balance sheet need to be converted/translated using different exchange rates and FCTR is needed to make sure your balance sheet still balances after all the line items on your balance sheet are converted at all those different rates.

When do I need FCTR?

When consolidating a foreign company in your group or converting a single company into another currency you’ll trigger the need to process an FCTR entry on your balance sheet.

To be clear, FCTR has got nothing to do with translating individual balances in a company’s trial balance. For example, a company with afunctional currency in Euros that has a USD bank account. That bank account gets converted to spot in that company’s functional currency at month end in that company’s trial balance. This is normally done by the accounting system.

FCTR only arises when you’re reporting an entire business/trial balance into another currency, whether on its own or as part of a consolidation process.

Why convert my balance sheet at different exchange rates?

Let’s just agree that the people making the rules very seldom sit down and rest. They’re obsessed with how best to present a company’s results.

For example, think of how weird it would be if share capital kept moving just based on the spot rate changing when you haven’t in fact issued new shares. And we want to make sure that the movement in retained earnings year on year ties in 100% with what you see on the P&L.

So how do I calculate FCTR?

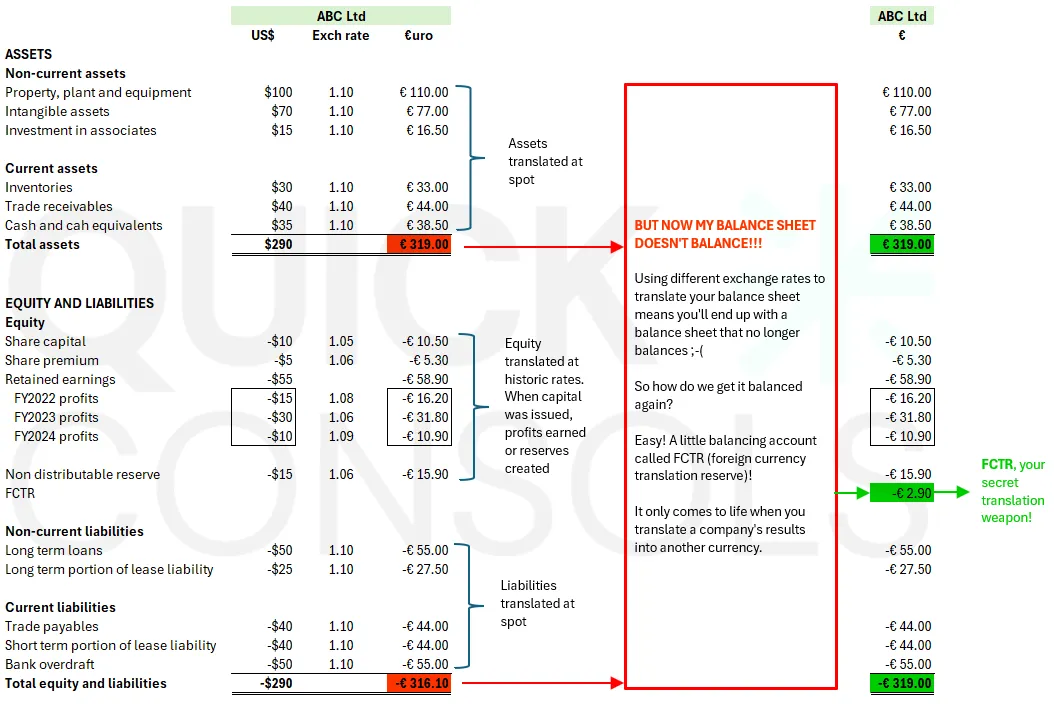

The easiest way to get your head around these rules is that all assets and liabilities get converted at closing spot rates. Equity is converted at the rates at which it was earned or created.

In a nutshell your FCTR is the difference between converting your equity line items at spot and converting them using these special "historical rates”.

Expressed as a formula

FCTR = (equity x spot) – (equity x special historical rates)

Let’s see what that looks like with a practical example:

What happens to my FCTR if I have non-controlling interests

Ah, a true twist on an old classic!

FCTR sits in the equity portion of your balance sheet. And if it sits under equity, it means it’s classified as a reserve account and your non-controlling interests need to share in that reserve.

All you need to do is calculate the FCTR value exactly as you normally would and allocate the relevant percentage to the non-controlling interests at the balance sheet date.

Expressed as a formula:

FCTR attributable to parent = FCTR x shareholding %

FCTR attributable to NCI = FCTR x NCI %

Get in touch with us

There’s only one thing we like more than consolidations, and that’s hearing from our followers and customers. If you’ve enjoyed this article or want to find other great resources, follow us on Linkedin.

If you’re interested in automating your FCTR or the consolidation in your business, feel free to contact us here or book a demo here.