Why Group Consolidations Fail the Audit Test

According to Talentia Software's 2026 consolidation research, finance teams spend roughly 80% of their time on data collection and reconciliation, leaving almost nothing for the documentation auditors actually want to see. The numbers look right. The consolidated trial balance ties out. But when external auditors start pulling threads, they aren't verifying your bottom line. They're tracing how you got there. Every elimination, every currency translation, every ownership percentage change needs a visible path from subsidiary source data to consolidated output.

That's where most group consolidations fall apart. Teams produce accurate figures through heroic spreadsheet efforts, yet can't demonstrate the controls, approvals, and matching logic behind those figures under scrutiny. Audit-ready financial consolidation isn't a year-end sprint. It means your group accounts can withstand examination at any point in the reporting cycle, with every adjustment documented and every intercompany balance reconciled before anyone asks.

With IFRS 18 taking effect on 1 January 2027 and requiring retrospective restatement of 2026 comparative data, the pressure on consolidation processes to maintain continuous, traceable documentation has never been more immediate. Teams that treat audit readiness as an annual cleanup project will find themselves restating figures without the trail to support them.

If you're building or refining your process, understanding group financial consolidation fundamentals is the right starting point before tackling the audit-specific requirements below.

What Do Auditors Actually Check in a Group Consolidation?

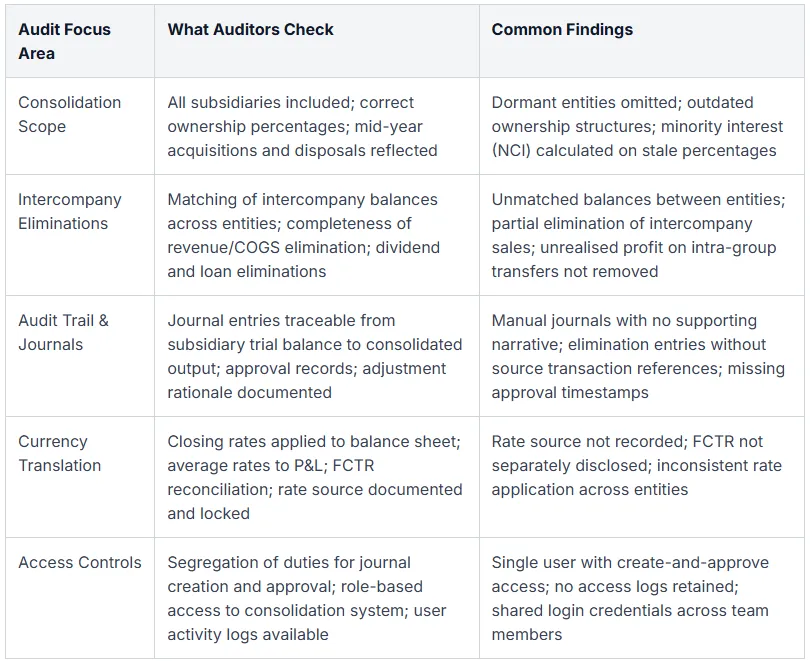

Auditors examine six core areas in group consolidation: scope completeness, intercompany eliminations, journal audit trails, currency translation methods, access controls, and subsidiary-to-consolidated mapping.

The first thing an auditor does isn't open your consolidated financial statements. They pull your group structure chart and cross-reference it against the list of entities feeding into the consolidation. Missing a dormant subsidiary or applying the wrong ownership percentage to a partially held entity triggers an immediate scope finding. This sounds basic, but groups that acquired or disposed of entities mid-year routinely get caught here.

Intercompany reconciliation draws the heaviest scrutiny. Mismatched intercompany balances remain the single most common audit finding in group consolidation processes, and auditors don't just check that eliminations were posted. They verify that every intercompany receivable in Entity A has a corresponding payable in Entity B, that the matching logic is documented, and that residual differences have been investigated and resolved. A $5,000 unmatched balance might seem immaterial, but it signals a process gap that auditors will probe further.

On the IT controls side, role-based access and segregation of duties are no longer optional in the consolidation tool. Auditors increasingly request user access logs showing who posted elimination journals, who approved them, and whether any single user had the ability to both create and approve entries. According to CRMT's consolidation research, legacy systems that lack governed environments frequently fail these IT general control reviews, even when the underlying accounting is sound.

Currency translation is another area where documentation matters as much as accuracy. Applying closing rates to balance sheet items and average rates to income statement lines correctly is only half the job. Without a record of which rate source you used, when the rates were locked, and how the foreign currency translation reserve (FCTR) was calculated, auditors will qualify their findings regardless.

EisnerAmper's audit advisory practice highlights reconciliation as a "core component" of audit readiness for group accounts. That perspective aligns with what most experienced financial controllers already know: the reconciliation schedule, not the consolidated P&L, is what auditors spend 70% of their time reviewing.

How Should You Document Intercompany Eliminations for Auditors?

Each intercompany elimination requires documented source transactions from both entities, the matching logic applied, and the resulting consolidation adjustment entry.

Poorly documented eliminations cause more audit delays than any other single consolidation issue. The reason is straightforward: eliminations touch every entity in your group, and a documentation failure in one entity cascades into qualified findings across the consolidated output.

Conventional advice focuses documentation effort on the elimination journal entries themselves. That's the wrong priority. The journal is actually the least important piece. Auditors spend most of their time on the pre-elimination reconciliation: the schedule showing each entity's intercompany balances, the differences identified during matching, and the resolution for each difference. A clean, complete reconciliation schedule means the elimination journals almost review themselves. Without it, even perfectly posted eliminations generate audit queries because the auditor can't verify the basis for the adjustment.

Three categories of intercompany eliminations consistently generate findings:

- Intercompany revenue and cost of goods sold: Both selling and purchasing entities must record identical transaction values. When one entity recognises revenue in a different period than the other recognises cost, the elimination won't net to zero, and auditors flag the timing mismatch.

- Intercompany dividends: Upstream dividends from subsidiaries to the parent must be eliminated against the parent's investment income. Groups with multiple tiers of ownership (sub-subsidiaries paying dividends to intermediate holding companies) frequently miss one layer.

- Unrealised profit on intra-group asset transfers: If Entity A sells inventory to Entity B at a markup and Entity B hasn't sold it to a third party by period end, the unrealised profit sitting in Entity B's inventory must be eliminated. This catches even experienced teams because it requires tracking downstream inventory movements, not just the original intercompany sale.

Your PBC (Prepared By Client) list for the consolidation audit should include elimination schedules with transaction-level detail, a current group ownership structure chart, and the intercompany reconciliation showing balances per entity with variance explanations. Teams still managing this in spreadsheets often find that consolidation software versus Excel becomes a critical decision point once the group exceeds five or six entities, because maintaining bidirectional transaction references manually across that many legal entities is where errors creep in.

Auditors expect the intercompany reconciliation to be completed and reviewed before the consolidation is finalised, not assembled retrospectively during fieldwork. If your team is building elimination documentation after the auditors arrive, you're already behind.

What Does Continuous Audit Readiness Look Like for Consolidation Teams?

Continuous audit readiness means every monthly consolidation carries full documentation and controls, so annual audits become verification exercises rather than forensic reconstructions.

Most finance teams treat audit preparation as a discrete project. That framing creates the problem. If your December consolidation is the only one with clean elimination journals and complete FCTR reconciliations, you're rebuilding eleven months of documentation under deadline pressure. The groups that breeze through audits don't prepare differently. They consolidate differently every single month.

Monthly close discipline is the mechanism that makes this work. Each period-end consolidation should produce the same deliverables your auditor expects at year-end: matched intercompany balances, timestamped adjustment entries, subsidiary data completeness confirmations, and scope verification against your current group structure. When the annual audit arrives, you hand over twelve already-reviewed packages instead of constructing one massive retrospective file.

The workload concern is real but backwards. Catching a $40,000 intercompany mismatch in February takes thirty minutes to resolve. Discovering it in December, compounded across ten subsequent periods, can consume days. Automated consolidation platforms generate audit trails in real time, logging every adjustment with user attribution and timestamps. The documentation isn't an extra step. It's a byproduct of the consolidation itself.

One thing that catches groups off guard: only 53% of businesses have sufficient historical data quality to support the kind of continuous monitoring that regulators and auditors increasingly expect. If your subsidiary data feeds are inconsistent month to month (different chart of accounts mappings, inconsistent currency rate sources, varying cutoff dates), continuous readiness is impossible regardless of your tooling.

A practical monthly audit-readiness routine covers six checkpoints. Run through these before signing off each period:

- Subsidiary data completeness: confirm all entities submitted trial balances using the current group chart of accounts, with no unmapped lines

- Intercompany balance matching: verify that every intercompany pair nets to zero before eliminations post, with variance explanations for any residual differences

- Elimination journal review: check that each elimination ties to source documentation from both counterparties, not just the reporting entity

- FCTR reconciliation: reconcile the foreign currency translation reserve movement to the underlying rate changes and subsidiary equity movements for the period

- Access control verification: confirm that only authorised users posted consolidation adjustments, and that no manual overrides bypassed approval workflows

- Consolidation scope confirmation: validate that the entity list reflects any acquisitions, disposals, or ownership changes effective during the period

Skipping any one of these in a given month doesn't cause an immediate problem. But it creates a gap that auditors will find, and explaining a gap retroactively is always harder than preventing it.

Frequently Asked Questions About Audit-Ready Consolidation

What is the difference between audit-ready and audit-proof consolidation?

Audit-ready means your consolidation can withstand external scrutiny at any point, with complete documentation, clear control evidence, and traceable adjustments. "Audit-proof" is a term that floats around but doesn't reflect reality. Every consolidation carries some risk of findings. The goal is minimising qualifications and avoiding delays, not achieving invulnerability.

What documents should be on a consolidation audit PBC list?

Subsidiary trial balances for every entity in scope, intercompany reconciliation schedules showing matched pairs, elimination journals with line-level supporting detail, the group ownership structure (including mid-year changes), currency translation workings with rate sources identified, and consolidation adjustment narratives explaining the business rationale for each manual entry.

How does IFRS 18 affect consolidation audit requirements in 2026?

IFRS 18 replaces IAS 1 and mandates new income statement categories: operating, investing, and financing. Groups preparing 2026 comparatives under IFRS need to restructure their consolidation templates now and document the reclassification methodology clearly. Auditors will test whether the new categorisation has been applied consistently across all subsidiaries.

How often should intercompany balances be reconciled for audit readiness?

Monthly. Full stop. Leaving intercompany matching to year-end creates large, compounding discrepancies that auditors flag as control weaknesses and that take disproportionate effort to unwind.

Can Excel-based consolidation be audit-ready?

Technically yes, but the discipline required is extreme. You'd need enforced version control, manual audit trails logging every cell change, restricted file access, and documented review sign-offs for each period. Most auditors assign higher inherent risk to spreadsheet-based consolidations because Excel lacks built-in controls for user attribution, change tracking at the formula level, and concurrent access management. For groups with more than five or six entities, the overhead of maintaining audit-quality spreadsheets typically exceeds the cost of purpose-built consolidation software.

Build Audit-Ready Consolidations Without the Year-End Scramble

Reconstructing twelve months of audit documentation in a few weeks is a problem that shouldn't exist. If your consolidation process generates audit trails, intercompany matching, and IFRS-compliant output automatically each period, the annual audit becomes a formality. Explore Quick Consols' consolidation software to see how that works in practice.