Why Multi-Currency Spreadsheet Consolidation Is Breaking Your Month-End

Month-end arrives. Your team opens the consolidation workbook. Three hours later, someone notices the EUR closing rate in tab 4 doesn't match the rate hardcoded in tab 11.

This is where multi-currency consolidation quietly breaks. Finance teams burn days re-keying FX rates across linked spreadsheets, chasing broken references between subsidiary files, and reverse-engineering why the FCTR plug doesn't tie to last period. Every manual rate entry is an audit finding waiting to happen. Every broken link is a restatement risk.

The core problem is structural, not effort-based. Spreadsheets weren't built to handle a 12-entity group operating in four currencies, where closing rates apply to balance sheets, average rates apply to income statements, and historical rates apply to equity movements. Add intercompany loans, minority interests, and a subsidiary in a hyperinflationary economy, and the model becomes a black box that only one person on the team fully understands.

Automated financial consolidation is the process of using cloud-based software to merge multi-entity, multi-currency financials without manual spreadsheet work. The software pulls trial balances from each entity, applies the correct FX rate by line type, eliminates intercompany transactions, calculates FCTR, and produces audit-ready group financial statements. No re-keying. No broken links. No mystery balances.

Below are eight specific ways automation replaces the spreadsheet workflows that are costing your finance team time, accuracy, and credibility with auditors. Each one targets a failure mode that finance controllers already know intimately.

1. Automate FX Rate Sourcing and Application Across Entities

FX rate sourcing is where most consolidation errors begin. Someone pulls a rate from a central bank website. Someone else uses last month's average. A third analyst types the rate into a cell, transposing two digits. By the time the auditor asks which rate was applied to which line, nobody can reconstruct the answer.

Automated consolidation flips this entirely. The software pulls daily and period-end rates from a central FX feed, stores them against the consolidation period, and applies them automatically based on the line type in each trial balance. Balance sheet items pick up the closing rate. Income statement items pick up the period average. Equity movements pick up the historical rate at the date of transaction. All of it happens per IAS 21, without anyone touching a cell.

Consider a mid-market group running 12 entities across USD, EUR, GBP, and ZAR. In a spreadsheet model, that's 48 manual rate entries per close. Multiply by closing, average, and historical, and you're past 140 individual data points every month. Each one is a re-keying risk. One automated FX sync replaces all of them and timestamps the source.

The audit benefit is immediate. The classic question, which rate did we use on this line, has a one-click answer. Every translated balance carries its rate, its source, and the date the rate was captured. Reviewers stop reconciling and start reviewing.

For finance teams operating across jurisdictions, the right approach to automated financial consolidation removes the rate-sourcing argument from the close entirely. The conversation shifts from which rate is correct to whether the underlying trial balance is complete. That's the conversation worth having.

2. Eliminate Intercompany Transactions in Foreign Currencies Without Manual Reconciliation

Intercompany eliminations look simple on paper. Entity A sells to Entity B, you eliminate both sides, the group P&L stays clean. Then the entities transact in different functional currencies, and the spreadsheet model starts producing imbalances that don't tie out.

The failure is mechanical. Entity A books a EUR receivable. Entity B books a GBP payable. The original transaction used a spot rate from three weeks ago. At period-end, each side translates at a different rate to the group currency. The elimination no longer balances, and someone posts a plug to FCTR or, worse, to retained earnings.

Automated consolidation handles this in a defined sequence. The software matches intercompany balances across entity pairs, translates each side using the correct rate, eliminates the matched portion, and posts the FX difference to the appropriate reserve. Rounding differences below a defined threshold are auto-cleared. Timing differences, where one side booked the transaction in a different period, are flagged for review rather than silently absorbed.

For finance teams that have spent years untangling intercompany loans denominated in three currencies, this is the workflow that stops eating weekends. The software keeps a running ledger of every elimination entry, every FX adjustment, and every unmatched balance. When the auditor asks why the intercompany interest charge moved 200K period-over-period, the answer takes a minute, not a morning.

The compliance benefit goes beyond speed. Every elimination carries a full audit trail: the source documents, the FX rates applied, the user who reviewed it, the timestamp of the post. Practitioners who have moved from spreadsheets to dedicated platforms know how to eliminate intercompany transactions cleanly when the system enforces the matching logic rather than leaving it to a careful analyst with a coffee.

The result is a consolidation that ties, every time, with no plugs and no manual force-balancing.

3. Automate the Foreign Currency Translation Reserve (FCTR) Calculation

The Foreign Currency Translation Reserve is the single biggest source of consolidation errors in multi-currency groups. FCTR captures the FX differences that arise when a subsidiary's net assets are translated at the closing rate while its results are translated at the average rate. The math is precise. The execution, in spreadsheets, is brutal.

In manual models, FCTR is usually a plug. The analyst translates the trial balance, the consolidation doesn't tie, and the difference goes to FCTR. The reserve becomes the dumping ground for every rounding error, every rate mismatch, and every late adjustment nobody wanted to trace. Auditors notice. They always notice.

Automated consolidation calculates FCTR from first principles. The software tracks the opening FCTR balance per entity, applies the closing rate to net assets, applies the average rate to current-year movements, and isolates the historical rate on opening equity. The closing FCTR balance is the mathematical result of those translations, not a residual. Every component is traceable to a source line in the underlying trial balance.

The difference at audit is significant. A spreadsheet FCTR plug invites questions the team cannot fully answer. A calculated FCTR, with every translation broken out by entity and by line, shuts the question down before it's asked. Teams that ship this workflow consistently cut FX reconciliation time meaningfully during close, often the difference between a stretched week and a controlled cycle.

For groups carrying multiple foreign subsidiaries, this is where automated financial consolidation earns its keep. The reserve stops being a mystery account and starts being a derived output. Every period-on-period movement is explainable. Every translation difference has a home.

This is also the area where finance leaders feel the operational shift most. The work moves from reconciling FCTR to reviewing it, which is the work the team should have been doing all along.

4. How to Handle Hyperinflationary Subsidiaries Without Rebuilding Your Model

How do you consolidate a hyperinflationary subsidiary without rebuilding your group model?

You apply IAS 29 restatement to the subsidiary's financials before translating them into the group currency. Automated consolidation does this in sequence: index the subsidiary's non-monetary items using the local CPI, restate the income statement to current purchasing power, recognize the gain or loss on the net monetary position, and only then translate the restated figures at the closing rate.

IAS 29 defines a hyperinflationary economy as one where cumulative inflation over three years approaches or exceeds 100%, a threshold documented by Fuel Finance in its overview of consolidation software. Argentina, Turkey, and Zimbabwe have all crossed that line in recent reporting cycles. For groups with subsidiaries in those jurisdictions, the accounting treatment is not optional.

In spreadsheet models, hyperinflation is a structural failure. The model was built to translate, not to restate. When a subsidiary's economy crosses the threshold mid-year, the team faces a choice: rebuild the model from scratch, or apply restatement as a manual overlay that nobody fully trusts. Both options are expensive, and both produce results that auditors challenge.

Automated consolidation handles the transition without a rebuild. The software flags the subsidiary, applies the CPI index series to the appropriate balances, calculates the monetary gain or loss, and feeds the restated trial balance into the standard translation workflow. The group consolidation continues normally. The audit trail captures every restatement entry and every index applied.

The practical benefit is continuity. A subsidiary moving into hyperinflation no longer triggers a panic project. The treatment is mechanical, repeatable, and reviewable. That matters when the controller is already managing a close and cannot afford a parallel workstream rebuilding a multi-entity spreadsheet.

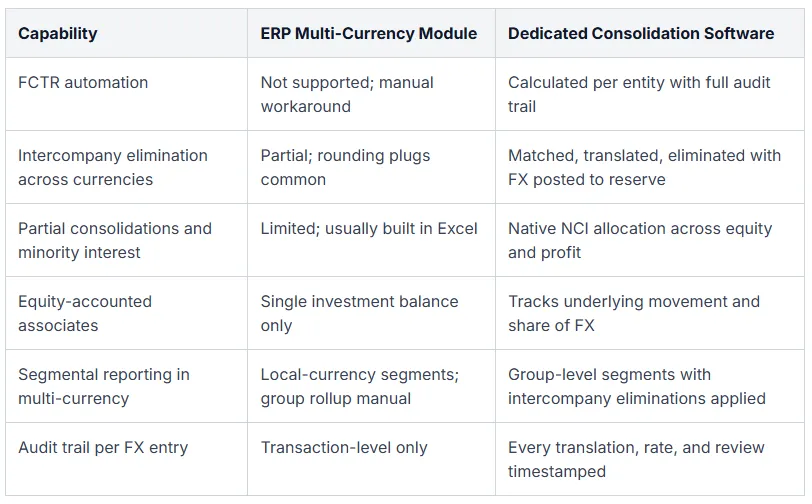

5. Why ERP Multi-Currency Modules Are Not Enough for True Consolidation

The finance industry has a comfortable assumption: a strong ERP handles consolidation. It does not. ERP multi-currency modules translate transactions at the entity level. They were not built to produce consolidated group reports with FCTR tracking, partial consolidations, and minority interest logic.

The evidence is empirical. Most groups, even those running well-implemented ERPs, still rely on Excel after the ERP go-live. The reason is structural. ERPs excel at recording transactions in local currency and translating them for local reporting. Consolidation is a different problem. It requires logic the ERP wasn't designed to hold.

Minority interests are the clearest example. When a group owns 70% of a subsidiary, the consolidation needs to allocate the NCI share of profit, equity, and FCTR across multiple reporting layers. ERP modules typically don't carry that logic. The team builds it in Excel, and the spreadsheet becomes the system of record for the most complex part of the consolidation.

Equity-accounted associates pose the same problem. The associate isn't consolidated line-by-line, but its share of profit and FX movement still flows into the group accounts. ERPs treat the investment as a single balance. Dedicated consolidation software tracks the underlying movement.

Segmental reporting in multi-currency compounds the issue. Reporting profitability by business unit, geography, and currency, with intercompany eliminations applied at the segment level, requires a consolidation layer that an ERP module cannot provide.

The practical recommendation is to add dedicated consolidation software on top of the ERP rather than replace it. The ERP keeps doing what it does well. The consolidation platform handles the group-level logic. For controllers weighing the tradeoff, the comparison of ERP vs automated financial consolidation tooling clarifies where each system earns its place.

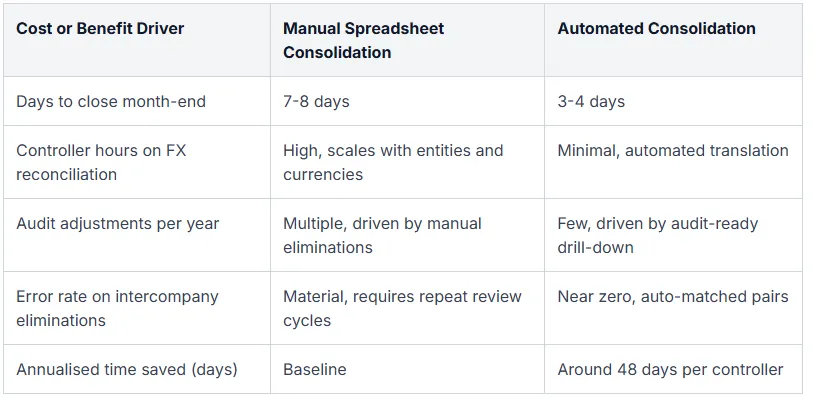

6. Calculate the ROI of Automated Multi-Currency Consolidation

ROI conversations about consolidation software usually stall because finance teams measure the wrong things. They count license fees against headcount savings. That math misses the point.

The real ROI sits in three buckets: time saved, error reduction, and audit fee compression. Each one compounds. Each one shows up on a different line of the P&L.

Start with the time calculation. Multiply entities by currencies by manual hours per month, then by twelve. A group with eight entities across four currencies, where each FX reconciliation eats two controller hours, burns 768 hours a year on translation alone. That's before intercompany matching. Before FCTR validation. Before the trial balance even gets touched.

A mid-market group that cuts four days off month-end recovers 48 days of controller time per year. Blend a controller's loaded hourly rate against that recovered capacity and the software pays for itself before the second close. Leading organizations using specialist consolidation tools reduced their close cycle from 7-8 days to 3-4 days on average, which lines up with what finance teams report after their first automated consolidation cycle.

Then layer in error reduction. Manual eliminations carry a known failure rate. Each missed intercompany pair becomes either an audit adjustment or a restated prior period. Both cost money. Both damage trust with the board.

Finally, audit fees. Auditors price risk. A consolidation pack with a clean drill-down audit trail, automated FCTR, and consistent FX rate sourcing changes the conversation with the audit partner. Lower risk premium. Fewer adjustment hours. Smaller management letter.

The table below frames the comparison the way a CFO needs to see it.

7. How AI Agents Handle Currency Consolidation Tasks in 2026

AI agents in consolidation software get marketed harder than they get explained. Strip the language back and the picture is simpler. An AI agent in consolidation is software that autonomously executes defined accounting tasks and flags exceptions for human review. Nothing more. Nothing less.

The useful question is what they actually do during a close.

Anomaly detection on FX movements. Agents compare current-period exchange rate movements against historical ranges and flag translations that fall outside expected bounds. A subsidiary booking a 12% currency swing in a quarter where the underlying pair moved 3% gets surfaced before the controller opens the file.

Auto-matching intercompany pairs across currencies. This is where agents earn their keep. Manual intercompany matching breaks when the parent books USD and the subsidiary books in local currency at a different rate or on a different day. An agent reconciles the pair at the booking-date rate, identifies the residual, and proposes the elimination journal. The controller approves or rejects.

Drafting variance commentary. Agents pull the largest movements between current and prior period, attribute them to volume, price, or FX, and draft the first paragraph of management commentary. The controller edits. The first draft is gone.

Exception routing on FCTR. When the foreign currency translation reserve moves outside expected bands, the agent flags the segments driving it before sign-off.

What AI agents cannot do is replace controller judgment on materiality, disclosure, and going concern. They do not decide whether a contingent liability gets disclosed. They do not assess whether a related-party transaction needs board attention. They do not sign the representation letter.

The boundary is clean. Agents handle reconciliation, matching, and first-pass analysis. Controllers handle judgment and accountability. Treating that boundary as a feature, not a limitation, is how finance teams get value from the technology. When evaluating tools, what to look for during a demo matters more than the feature list on the website.

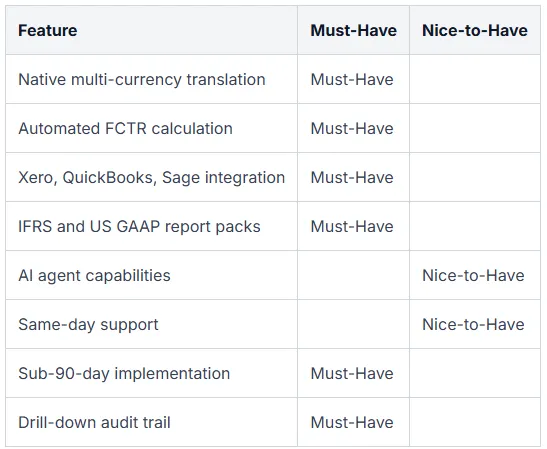

8. What to Look for in Multi-Currency Consolidation Software (Selection Checklist)

What should finance teams actually look for in multi-currency consolidation software?

The vendor shortlist is where most selection processes go sideways. Demos look polished. Feature lists overlap. Pricing pages dodge the questions that matter. A clear checklist forces vendors to demonstrate capability instead of describe it.

Non-negotiables for any mid-market group:

- Native multi-currency translation. The software handles closing rate, average rate, and historical rate translation without bolt-on modules or manual journals.

- Automated FCTR calculation. The foreign currency translation reserve posts automatically with full audit trail back to source rates.

- Direct integrations with Xero, QuickBooks, and Sage. Trial balances pull on demand. No CSV exports. No reformatting.

- IFRS and US GAAP report packs. Both standards run in parallel from the same data source, with management and statutory views available.

- Drill-down audit trail. Every consolidated number traces back to the source journal in the subsidiary ledger.

Mid-market specific criteria:

Implementation should run under 90 days. Anything longer signals enterprise-tier complexity that mid-market teams cannot absorb. The product should not require a dedicated IT resource to operate. Finance owns the system; IT does not need to be in the room.

Red flags during vendor demos:

Watch for vendors who cannot show a live FX translation walkthrough. If the demo skips the actual translation mechanics and jumps straight to dashboards, the underlying engine is probably weaker than the marketing suggests. Ask to see a hyperinflationary subsidiary handled end-to-end. Ask to see an intercompany pair eliminated across two currencies in real time. Vendors with mature multi-currency engines welcome these questions. Vendors without them deflect.

The checklist below separates the must-haves from the nice-to-haves. Use it to score vendors during demos. The scoring usually makes the decision obvious by the second or third call.

Frequently Asked Questions About Automated Multi-Currency Consolidation

What is automated financial consolidation?

Automated financial consolidation is the use of dedicated cloud-based software to merge multi-entity financial data, perform foreign currency translation, eliminate intercompany transactions, and produce group financial statements without manual spreadsheets. The benefits are concrete: shorter close cycles, fewer audit adjustments, and a drill-down audit trail that traces every consolidated number back to its source journal.

How does automated consolidation handle multi-currency translation?

Automated consolidation applies the closing rate to balance sheet items, the average rate to P&L items, and the historical rate to equity, in line with IAS 21. The resulting translation difference posts automatically to the foreign currency translation reserve through OCI. Rates pull from a single source, and the FCTR carries a full audit trail back to the originating transactions.

What is the difference between financial consolidation and financial close?

The financial close is an entity-level process. It finalises the trial balance for a single legal entity by booking accruals, reconciling sub-ledgers, and locking the period. Consolidation is the group-level process that follows. It combines multiple closed trial balances, translates foreign currencies, eliminates intercompany transactions, and produces one set of group financial statements.

Can mid-market companies afford automated consolidation software?

Yes. Modern cloud-based consolidation tools are priced per entity rather than per seat, and they integrate directly with Xero, QuickBooks, and Sage. Groups with five or more entities and multi-currency exposure typically reach payback inside the first few close cycles, driven by recovered controller time, fewer audit adjustments, and a tighter audit fee.

How long does it take to implement automated consolidation software?

Mid-market implementations typically run between 30 and 90 days when the platform is cloud-native and ships with pre-built integrations for Xero, QuickBooks, and Sage. Enterprise implementations stretch to six to twelve months because of custom ERP work and bespoke chart-of-accounts mapping. Speed of deployment is one of the strongest signals of product fit for mid-market groups.

Does automated consolidation software support IFRS and US GAAP?

Yes. Quality consolidation software supports IFRS and US GAAP in parallel from the same underlying data source. Finance teams can produce statutory reports under one framework and management reports under the other without rekeying data. The same engine handles segmental reporting, partial consolidations, and the disclosure notes required by each standard.

Stop Converting Currencies in Spreadsheets, Start Consolidating with Quick Consols

Spreadsheets are not free. They cost controller weekends, audit adjustments, and the trust of every board member who has watched a restated number land in a quarterly pack.

The cost of staying manual compounds quietly. Each new entity adds another trial balance to map. Each new currency adds another FCTR calculation to verify. Each audit cycle adds another round of adjustments that should have been caught at consolidation, not at sign-off. By the time the team admits the model is brittle, the close is already three days longer than it should be.

Quick Consols is built for finance teams that have run out of patience with that math. The platform handles multi-entity, multi-currency consolidation natively. FCTR posts automatically. Intercompany pairs match across currencies. IFRS and US GAAP packs run in parallel from the same trial balances. Direct integrations with Xero, QuickBooks, and Sage mean trial balances pull on demand, with no CSV gymnastics in between.

The product was built by a Chartered Accountant for finance teams, not by a software vendor selling to IT. That shows up in the way the platform handles partial consolidations, segmental reporting, NCI calculations, and the trial balance level audit trail that auditors actually trust.

If the next month-end already looks like the last one, the system is the bottleneck. Book a demo for Group Financial Consolidation and walk through your actual entity structure with someone who has consolidated groups for a living. Bring the spreadsheet that keeps breaking. We will show you what the same close looks like when the conversions, eliminations, and FCTR handle themselves.

Stop converting currencies in spreadsheets. Start running closes that finish on time, every month.