Translating a Consolidation into Reporting Currency

Have you ever asked yourself what exchange rates should I use when preparing my consolidation? Or should I use average exchange rates or closing spot rates when preparing my consolidation? Or, what exchange rates should I use to translate my share capital when preparing my consolidation? Well, hopefully this guide will give you the answers to all those questions.

Introduction

In a group structure, it is common for subsidiaries to operate in different countries and therefore keep their accounting records indifferent currencies. When preparing consolidated financial statements, these results must be translated into a single presentation currency for the group.

This article will offer guidance on how to translate these numbers as well as answer the basic question we all have:

Why do we use the spot rate here, the average rate there, and historical rates somewhere else entirely?

The aim here is to provide some practical guidance on how to translate a consolidation into another currency and understand why IFRS works the way it does.

The technical guidance comes from IAS 21 – The Effects of Changes in Foreign Exchange Rates, but the explanations are simplified.

Functional vs Presentation Currency

Before any translation happens, the two currencies must be clear:

· Functional currency: The local currency in the environment in which the entity operates.

· Presentation currency: The currency in which the group presents its consolidated financial statements.

As per IAS 21:

“An entity’s functional currency is the currency of the primary economic environment in which the entity operates.”

(IAS 21.8)

How IFRS Wants You to Translate

When a subsidiary’s functional currency differs from the group’s presentation currency, IFRS applies what is commonly called the closing rate method.

In practice, this means:

- Assets and liabilities are translated at the closing (spot) rate

- Income and expenses are translated at rates at the dates of the transactions (usually an average rate for the month when there is a large volume of transactions)

- Equity items are translated at historical rates

- Any difference goes to Other Comprehensive Income (OCI)

“The assets and liabilities of a foreign operation shall be translated at the closing rate.”

(IAS 21.39(a))

“Income and expenses… shall be translated at exchange rates at the dates of the transactions.”

(IAS 21.39(b))

Why Assets and Liabilities Use the Closing Rate

Assets and liabilities represent what the group owns and owes at reporting date.

If the group had to realise an asset or settle a liability on reporting date, it would do so at the current exchange rate, not last year’s rate. Using historical rates would understate or overstate the group’s actual exposure to currency risk at reporting date.

This is what IAS 21 requires:

“The assets and liabilities of a foreign operation shall be translated at the closing rate.”

(IAS 21.39(a))

Example 1:

A subsidiary has cash of $100,000 at year-end. The closing rate is 1 USD = 20 ZAR.

$100,000 × 20 = ZAR 2,000,000

This reflects the real value of that cash to the group at year-end, which is what the balance sheet is trying to show.

Why Income and Expenses Use an Average Rate

Income and expenses are not created all at once, they occur over time and build up over the period.

Using a single closing rate for all revenue and costs would apply year-end currency conditions to transactions that may have occurred months earlier. That can distort performance results.

IFRS makes provision for this here:

“For practical reasons, a rate that approximates the exchange rates at the dates of the transactions, for example an average rate for the period, is often used.”

(IAS 21.40)

As long as exchange rates haven’t been wildly volatile, an average rate usually gives a fair picture.

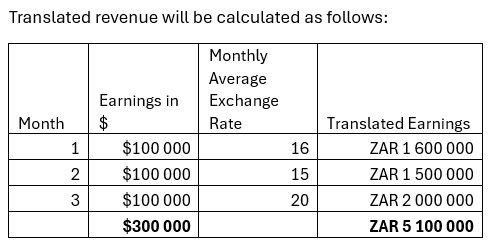

Example 2:

A subsidiary earns $100 000 revenue a month, with average monthly rates fluctuating between ZAR 16 – ZAR 20.

This better reflects how the business actually performed over time.

Why Equity Is Kept at Historical Rates

The key thing to remember is that equity represents owner investment, not operational activity.

That investment happened at a specific point in time, at a specific exchange rate. IFRS specifically caters for this and ensures the original value is preserved.

“Equity items are translated at historical rates.”

(IAS 21.47)

Example 3:

Share capital of $500,000 was created when the exchange rate was 1 USD = 15 ZAR.

$500,000 × 15 = ZAR 7,500,000

That translated amount stays fixed, year after year, provided there has been no change to the initial $500,000 such as sale of shares or issue of new shares (these subsequent transactions will be accounted for individually based on the rates on the new transaction dates).

Bringing in Foreign Currency Translation Reserve

Because different parts of the financial statements use different rates, the translated balance sheet will never balance naturally.

IFRS accounts for this difference by absorbing it into Other Comprehensive Income, where it accumulates in equity as the Foreign Currency Translation Reserve (FCTR).

“Exchange differences arising on translating the financial statements of a foreign operation shall be recognised in other comprehensive income.”

(IAS 21.41)

This keeps profit or loss focused on operational performance, not currency fluctuations.

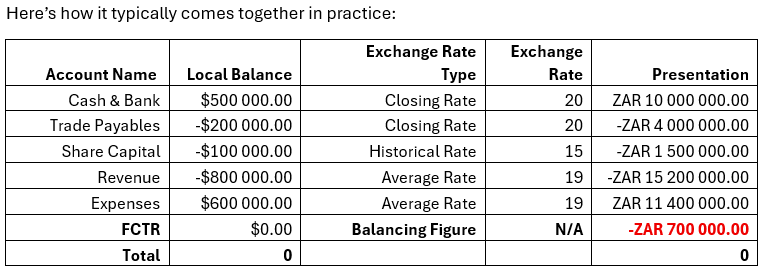

Basic Trial Balance Translation Example

The difference ends up in FCTR as the balancing figure.

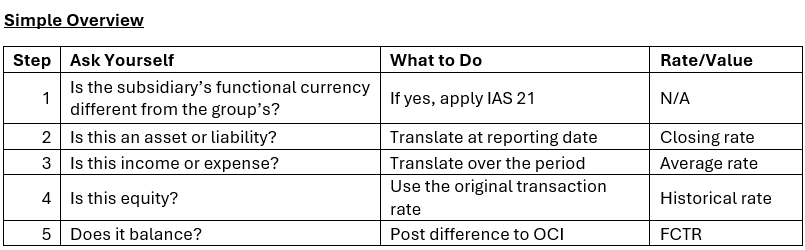

Simple Overview

Common Mistakes

- Using closing rates for revenue and expenses

- Re-translating share capital every year

- Posting translation differences to profit or loss

- Forgetting to assess whether an average rate is still appropriate

Each of these breaks the underlying IAS 21 logic.

Side note: Effect on NCI (When applicable)

Because FCTR sits in equity, it’s treated like any other equity movement. That means it’s shared between the parent and NCI based on their ownership percentages

- The total translation difference for the period is calculated at group level

- That amount is then split between:

- equity attributable to the owners of the parent, and

- non-controlling interests, according to their shareholding

Doing this ensures that NCI reflects its share of both:

- the subsidiary’s net assets translated at closing rates, and

- the currency movements affecting those net assets over time

Final Thoughts

Currency translation is about understanding what the numbers are trying to represent and using the correct conversion rates to most accurately represent these results.

- Closing rates show today’s financial position

- Average rates show performance over time

- Historical rates protect the integrity of owner investment

Once the basics are understood, the translation process becomes easier.

In closing, the good news is that our software at Quick Consols can automate these complex calculations and conversions. If you're interested in learning more book a demo with us or visit our Linkedin page for more information.

Get the latest updates, exclusive content, and exciting news delivered right to your inbox.

Share this Article

Get in touch!

If you have any questions about our Consolidation Software, send us a message below and we'll get back to you ASAP.