Unrealised Profit in Consolidation: The Practitioner's Guide

Intra-group trading creates a quiet accounting problem. Two entities in the same group transact, profit gets booked, and the goods sit in inventory at the reporting date. From the group's perspective, that profit isn't real. The group hasn't sold anything to the outside world yet.

This is unrealised profit. It's profit recorded on intra-group sales that has not yet been realised through external sale. According to ACCA Global, until inventory is sold to entities outside the group, any profit is unrealised and should be eliminated from the consolidated financial statements.

For any group with intercompany trading, this is a core consolidation issue. Get it wrong and the consolidated numbers overstate revenue, gross profit, and inventory carrying values. Auditors flag it. Stakeholders make decisions on inflated figures.

This guide covers the full practitioner mechanics. Definition, calculation, journal entries, the difference between downstream and upstream sales, treatment in PPE versus inventory, deferred tax implications, and how automation eliminates the manual workload. It goes beyond exam syllabus material into the territory finance teams actually deal with at month-end.

What Is Unrealised Profit in Consolidation Accounting?

Unrealised profit is profit recognised on intra-group transactions where the goods or assets remain within the group at the reporting date. The transaction happened. The invoice was raised. Cash may even have moved between subsidiaries. But the goods haven't left the group, so from a consolidated perspective, nothing was actually earned.

The source is intra-group trading. Parent sells inventory to subsidiary at a margin. One subsidiary transfers PPE to another. A service entity charges its sister company. As ACCA Global explains, unrealised profit arises when one group company sells goods to another at a profit and the goods remain in closing inventory, because the profit is 'unrealised' from the group's perspective until the goods are sold to an external customer.

The distinction is simple. Realised profit means the goods or assets have been sold to an external party. Unrealised profit means they're still sitting somewhere inside the group structure.

This ties back to the single economic entity concept. A group cannot make profit by trading with itself. IFRS 10 and IAS 27 set out the consolidation principles that require elimination of these internal transactions. The same logic extends to associates under IAS 28, where the investor's share of profit on intercompany transactions with associates transactions with the associate must also be eliminated.

Unrealised profit can arise in three main places: inventory still held at year-end, non-current assets like PPE transferred between entities, and through transactions with associates. Each requires a different elimination mechanic, but the underlying principle is the same.

Why Must Unrealised Profit Be Eliminated on Consolidation?

Unrealised profit must be eliminated because consolidated financial statements present the group as a single economic entity, and an entity cannot profit from transactions with itself. That is the short, snippet-ready answer. The longer version is where most finance teams get tripped up.

The contrarian view here: eliminating PURP is not primarily about compliance. It's about not lying to your own decision-makers. Boards setting capital allocation, lenders sizing facilities, and CFOs forecasting cash all rely on consolidated numbers being a true reflection of external trading. Internal markups dressed up as group profit corrupt every downstream decision.

The mechanical impact is precise. ACCA Global notes that if intra-group profit in unsold inventory is not eliminated, group revenue, cost of sales and gross profit will be overstated. The income statement looks healthier than reality.

The balance sheet takes a parallel hit. As ACCA Global also points out, without elimination of intra-group profit, inventory will be carried above cost, mis-stating both the consolidated profit or loss and statement of financial position. PPE carries the same risk when assets are transferred internally at a markup.

The audit consequences are immediate. PURP is one of the first areas external auditors test on group accounts. A missed elimination shows up in working papers, triggers adjustments, and erodes auditor confidence in the rest of the close. For listed groups, it can mean a restatement.

External stakeholders, lenders, investors, regulators, all price decisions off these numbers. Accurate consolidation isn't a finance team luxury. It's the foundation of every external preparing consolidated financial statements judgement made about the group.

How to Calculate PURP: Step-by-Step Worked Example

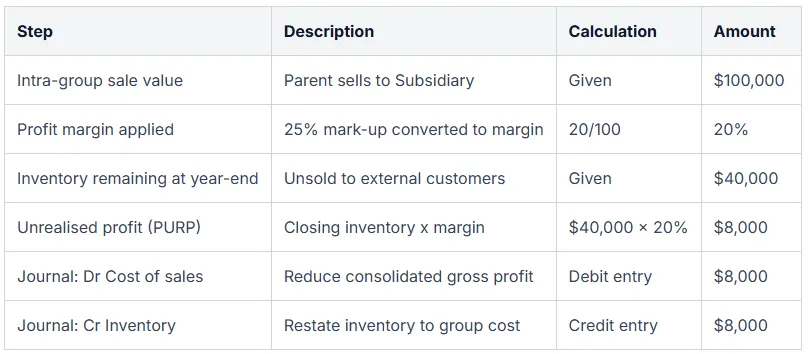

PURP stands for Provision for Unrealised Profit. The standard formula is straightforward: PURP equals closing inventory from intra-group sales multiplied by the seller's profit margin. The complexity sits in getting the margin definition right.

Margin and mark-up are not the same thing. ACCA Global defines margin as profit divided by selling price, and mark-up as profit divided by cost, noting that a 25% margin corresponds to a 33⅓% mark-up. Confuse the two and the elimination amount is wrong by a material number every single time.

Here's the worked example. Parent sells inventory to Subsidiary for $100,000 at a 25% mark-up on cost. At year-end, $40,000 of that inventory remains unsold to external customers.

Step one: convert the mark-up to a margin so the formula works cleanly. A 25% mark-up means cost is $80, profit is $20, selling price is $100. The margin is $20 divided by $100, or 20%.

Step two: apply the margin to the closing intra-group inventory. $40,000 multiplied by 20% equals $8,000. That $8,000 is the unrealised profit sitting inside the consolidated inventory balance.

Step three: post the elimination. The journal entry is Dr Cost of sales $8,000 / Cr Inventory $8,000. Cost of sales goes up, gross profit comes down, and inventory is written back to the group's actual cost. KPMG's illustrative IFRS disclosures guide confirms this is the standard mechanic: inventory from intra-group sales multiplied by profit margin, adjusted through cost of sales and inventory in the consolidation worksheet.

The impact flows through. Consolidated retained earnings drop by $8,000, and inventory on the consolidated statement of financial position is presented at the group's true cost rather than an internally inflated value.

In the following period, when those goods are finally sold externally, the adjustment reverses. The profit becomes realised through the external sale, so the prior-year elimination unwinds and the group recognises the profit in the correct period.

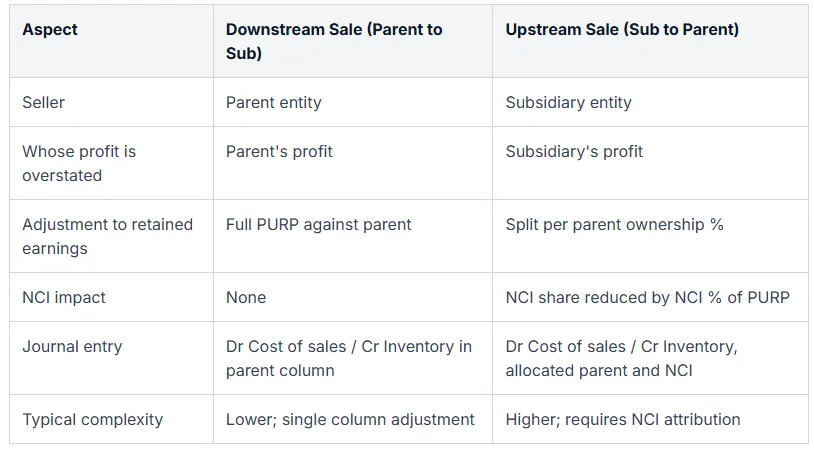

Downstream vs Upstream Sales: How Each Affects NCI

The direction of the sale changes who absorbs the elimination. This is the area where practitioners most often get the mechanics wrong, particularly when a non-controlling interest sits in the structure.

A downstream sale is parent to subsidiary. The parent recognises the profit, so the parent's books carry the overstatement. The full PURP adjustment hits the parent's retained earnings. There is no NCI impact, because NCI has no stake in the parent's profit.

An upstream sale is subsidiary to parent. The subsidiary recognises the profit, which means the subsidiary's reported profit is overstated. When that profit gets allocated up to the group, it splits between the parent's share and the NCI's share. The PURP adjustment must split the same way.

Here's the worked case. An 80% owned subsidiary sells $50,000 of inventory to its parent at a 30% margin. At year-end, $20,000 of that inventory remains unsold externally. PURP equals $20,000 multiplied by 30%, or $6,000.

Because this is upstream, the $6,000 reduces the subsidiary's profit. The parent's share of the elimination is 80%, or $4,800. The NCI absorbs 20%, or $1,200. As ACCA Global illustrates, when a subsidiary is 80% owned and makes an upstream sale, the unrealised profit adjustment is split 80:20 between parent and NCI. The principle is identical to how ACCA Global worked examples allocate an upstream unrealised profit adjustment of CU 10,000 between parent and NCI columns in consolidated retained earnings.

The common error: practitioners post the full elimination against parent retained earnings and forget the NCI line entirely. The consolidated profit is correct in total, but the attribution between owners of the parent and NCI is wrong. Audit catches it. Then comes the rework.

Unrealised Profit in Non-Current Assets (PPE) vs Inventory

Inventory isn't the only place unrealised profit hides. When one group entity sells property, plant or equipment to another at a margin above carrying value, that margin sits inside the asset on the buyer's balance sheet. From the group's perspective, no external transaction has occurred. The profit is unrealised and the asset is overstated.

The principle is anchored in IFRS. IFRS 10.B86(c) requires elimination of unrealised profit on intra-group transfers of assets recognised on the balance sheet, covering both PPE and inventory. IAS 16 reinforces this by requiring PPE to be carried at cost less accumulated depreciation and impairment, which means intra-group margin must be stripped out to reflect the group's historical cost.

Here's where PPE diverges from inventory. Inventory PURP reverses in one hit when the goods leave the group. PPE PURP reverses gradually, over the asset's remaining useful life, through a depreciation true-up.

Worked example. A subsidiary sells equipment to the parent for $80,000. Carrying value at the date of transfer is $60,000. Remaining useful life is 5 years.

- Initial elimination: Dr Gain on sale $20,000 / Cr PPE $20,000

- Annual depreciation adjustment: Dr Accumulated depreciation $4,000 / Cr Depreciation expense $4,000

The depreciation reversal runs every year until the asset is fully depreciated or disposed of externally. This is the trap. Practitioners eliminate the initial profit, move on, and forget the depreciation true-up in subsequent periods. The result is consolidated profit understated each year by the depreciation the group never should have recognised on the inflated carrying value.

Deferred Tax Implications and Automation of PURP Adjustments

Eliminating PURP isn't the end of the adjustment. It triggers a deferred tax consequence that catches many practitioners off guard.

The logic is straightforward. When you strip unrealised profit out of consolidated inventory or PPE, the carrying value in the group accounts drops. The tax base, recorded at the individual entity level, does not. That gap is a temporary difference, and IAS 12 requires deferred tax recognition.

The calculation is mechanical: unrealised profit multiplied by the applicable tax rate. KPMG's 'Insights into IFRS' walks through this directly. A CU 10,000 unrealised profit in inventory generates a deferred tax asset of CU 3,000 at a 30% tax rate. The standard journal entry per KPMG is Dr Deferred tax asset CU 3,000 / Cr Income tax expense CU 3,000, posted in the consolidation worksheet.

Most competitor articles stop at the PURP elimination and skip the deferred tax leg entirely. It's a practitioner-level adjustment that sits outside basic exam material, which is exactly why audit reviewers flag it.

Now consider doing this manually. Each entity. Each intra-group sale. Each closing inventory balance. Each PPE transfer with its multi-year depreciation true-up. Each NCI split. Each deferred tax entry. Across a multi-entity group with recurring intercompany trading, spreadsheets break down fast.

This is where automated consolidation software earns its place. PURP adjustments, upstream and downstream allocations, NCI splits, and the deferred tax journals all flow from a single workflow. The audit trail is preserved. The eliminations repeat cleanly each period. Manual errors drop. For teams looking to fix multi-entity close bottlenecks, removing manual PURP tracking is one of the highest-leverage changes you can make.

Frequently Asked Questions

What is unrealised profit in consolidation accounting?

Unrealised profit is profit recognised on intra-group sales where the goods or assets are still held within the group at the reporting date. Because no external transaction has occurred, the profit has not been realised from the group's perspective. It must be eliminated to avoid overstating consolidated revenue, profit, and asset values.

Why must unrealised profit be eliminated on consolidation?

Consolidated statements present the group as a single economic entity. A group cannot profit by trading with itself. Leaving unrealised profit in overstates both consolidated profit and the carrying value of inventory or PPE. Eliminating it ensures the group accounts reflect only transactions with parties outside the group.

What is PURP and how is it calculated?

PURP stands for Provision for Unrealised Profit. It is calculated by taking the value of closing inventory still held within the group from intra-group sales and multiplying it by the seller's profit margin or markup. The result is the profit element that must be stripped out of consolidated inventory and cost of sales.

How does upstream vs downstream sale affect NCI?

Downstream sales, where the parent sells to a subsidiary, affect only parent retained earnings. Upstream sales, where the subsidiary sells to the parent, reduce subsidiary profit. The PURP adjustment is shared between parent and NCI in line with ownership percentages, so the NCI absorbs its proportional share of the elimination.

Does unrealised profit elimination create deferred tax?

Yes. PURP elimination reduces the consolidated carrying value of the asset, but the tax base at the individual entity level is unchanged. That temporary difference creates a deferred tax asset, calculated at the applicable tax rate. The journal entry is Dr Deferred tax asset / Cr Income tax expense in the consolidation worksheet.

What happens to unrealised profit in the next period?

When the inventory or asset is sold to a party outside the group, the previously unrealised profit becomes realised. The prior period elimination is reversed in the consolidation, restoring the profit to consolidated retained earnings. This is why PURP tracking must be maintained period after period, not treated as a one-off adjustment.

Automate PURP and Group Consolidation with Quick Consols

Tracking PURP manually compounds quickly. Every intra-group sale, every closing inventory balance, every PPE transfer with its multi-year depreciation true-up, every upstream split between parent and NCI, every deferred tax journal. Across a multi-entity group running recurring intercompany trading, the spreadsheet workload becomes a monthly drain on finance teams who already have a close deadline pressing.

Quick Consols automates this. Intercompany eliminations, PURP adjustments, NCI splits, and the corresponding deferred tax journals all run inside one cloud-based workflow with a complete audit trail. The platform integrates directly with Xero, QuickBooks, and Sage, pulling entity-level data into a single source of truth for group reporting. Foreign currency translation, FCTR movements, and audit-ready financial statements come out the other side without the manual rework.

If your team is spending close week reconciling PURP schedules instead of analysing results, see how Group Financial Consolidation handles the mechanics end-to-end. Book a demo and walk through your own consolidation pain points with the team.