Financial Consolidation Software: 8 Ways to Fix Multi-Entity Close

A group financial controller with 14 subsidiaries across three countries spent her entire weekend reconciling intercompany loan balances in a spreadsheet that someone accidentally overwrote on Friday afternoon. She isn't alone, and the fix isn't working harder.

Mid-market groups are acquiring faster than their finance processes can absorb. A company that operated as three entities five years ago now manages twelve, spanning multiple currencies, jurisdictions, and accounting standards. But the consolidation method? Still the same patchwork of Excel workbooks, emailed trial balances, and manual journal entries that barely worked at three entities. The global financial consolidation software market was valued at USD 1.5 billion in 2023 and is projected to reach USD 3.2 billion by 2032, according to Dataintelo's market report. That growth reflects a simple reality: organizations are hitting the ceiling of what spreadsheets can handle.

The symptoms are predictable across nearly every mid-market group:

- Version control failures where two people edit the same consolidation workbook simultaneously

- Copy-paste errors in trial balance data that cascade silently through elimination entries

- Email chains replacing proper workflow, with no audit trail showing who approved what

- Foreign currency translation done through manual rate lookups and formula overrides

- Month-end closes stretching to 15 or 20 working days because nobody trusts the numbers until they've been checked three times

This article breaks down eight concrete ways that financial consolidation software replaces the broken status quo. Each section tackles a specific pain point, from intercompany eliminations and multi-currency translation to ERP integrations and audit readiness, with a focus on what mid-market finance teams actually need rather than enterprise-scale features they'll never use.

1. How Does Financial Consolidation Software Replace Spreadsheet-Based Closes?

Financial consolidation software replaces spreadsheets by automating trial balance collection, chart of account mapping, adjustments, intercompany eliminations, and consolidated reporting in one controlled workflow.

The consolidation process follows a consistent sequence regardless of group size. First, trial balances are collected from every entity. Then each entity's chart of accounts is mapped to the group's reporting structure. Consolidation adjustments (goodwill amortization, fair value uplifts, NCI calculations) are posted. Intercompany eliminations remove intra-group transactions. Finally, consolidated financial statements and segmental reporting are produced.

In Excel, every one of those steps is a manual handoff. Someone exports a CSV from QuickBooks. Someone else pastes it into the master workbook. A formula references cell G47 on a tab called "Entity 5 TB," and if that tab gets renamed or a row gets inserted, the formula breaks silently. Multiply that across ten entities and you're troubleshooting phantom variances at 11pm on day eight of the close.

Financial consolidation software compresses this into a controlled sequence. Trial balances pull directly from source systems. Mapping rules persist between periods, so you configure once and adjust only when the chart of accounts changes. Elimination entries generate automatically based on pre-defined intercompany relationships. The output is a consolidated trial balance, group P&L, balance sheet, and cash flow, all traceable back to the source data.

One trigger that pushes teams toward automation is the end-of-life problem. Legacy desktop consolidation tools or heavily customized Excel models eventually reach a point where the person who built them leaves, the software loses vendor support, or the group simply outgrows the model's capacity. That migration moment, replacing a system that no longer scales, is when most mid-market groups first evaluate purpose-built consolidation platforms.

The practical difference comes down to control. In a spreadsheet, you're managing data and logic in the same place, which means any user can accidentally alter the consolidation engine itself. In dedicated software, the logic is locked, the data flows through it, and every change is logged. That distinction alone eliminates the most common category of consolidation errors: unintentional structural changes to the workbook.

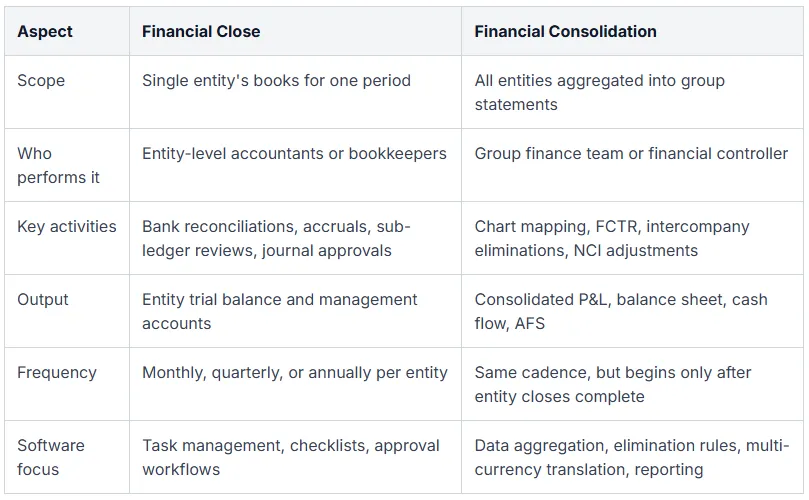

2. What's the Difference Between Financial Consolidation and Financial Close?

Financial close finalizes an individual entity's books for a reporting period; financial consolidation aggregates those closed books into group-level statements with eliminations and adjustments applied.

These two processes get conflated constantly, partly because they happen back-to-back and partly because some platforms handle both. They solve different problems. The financial close is entity-level work: reconciling bank accounts, posting accruals, reviewing sub-ledgers, and confirming that a single entity's trial balance is accurate and complete. Financial consolidation starts after that, taking the closed trial balances from every entity in the group and combining them into one set of IFRS or US GAAP compliant group financial statements.

The sequencing matters because consolidation can't produce reliable output from unreliable inputs. If Entity 7 hasn't finished its close and the trial balance still has unreconciled suspense account balances, the consolidated numbers will be wrong. Modern cloud platforms address this by building close management (task checklists, approval workflows, status dashboards) directly into the same environment where consolidation runs. CCH Tagetik, for example, was named a Leader in the 2026 Gartner Magic Quadrant for Financial Close and Consolidation, partly because of this unified approach. For a broader comparison, this list of consolidation tools covers options across different group sizes.

For mid-market groups, the practical question is whether you need two separate systems or one that handles both. Groups with fewer than 20 entities typically benefit from a single platform that manages the close checklist and runs the consolidation, because it reduces handoffs and keeps everything in one audit trail.

3. Why Should Mid-Market Finance Teams Prioritize Automated Intercompany Eliminations?

Intercompany eliminations remove intra-group transactions from consolidated statements, and manual processing of these entries accounts for over 40% of close delays in multi-entity groups.

Conventional wisdom says tackle intercompany eliminations last, after everything else in the consolidation is clean. That's backwards. Eliminations should be the first process you automate, because errors here contaminate every downstream output: consolidated revenue, group profit margins, balance sheet integrity, and segmental reporting. A mismatched intercompany receivable/payable doesn't just create a variance; it raises questions during audit that consume days of investigation.

Four categories of intercompany transactions require elimination in group financial statements:

- Intercompany revenue and expenses: Entity A sells services to Entity B. Both record the transaction, but at group level it's internal activity that must be removed to avoid inflating consolidated revenue.

- Intercompany loans and balances: Receivables and payables between entities must net to zero in the consolidated balance sheet. Foreign currency translation differences on these balances create reconciliation headaches.

- Unrealised profit on inventory transfers: If Entity A sells inventory to Entity B at a markup and Entity B hasn't sold it externally by period-end, that unrealised profit must be eliminated from consolidated inventory and cost of sales.

- Intercompany dividends: Dividends paid by a subsidiary to its parent are eliminated to prevent double-counting of group retained earnings.

In a spreadsheet, each of these requires manual identification, matching, and journal entry. When Entity A records an intercompany sale of £250,000 and Entity B records a purchase of £249,800 (because of rounding, timing, or FX differences), someone has to investigate the £200 variance manually. Across 15 entities with dozens of intercompany relationships, these small mismatches multiply into a reconciliation nightmare.

"The biggest risk in manual eliminations isn't the large errors. Those get caught. It's the small, systematic mismatches that accumulate over quarters and only surface during year-end audit." This pattern shows up repeatedly in groups that have grown through acquisition without standardizing their intercompany accounting policies.

Rule-based elimination engines solve this by pre-defining intercompany relationships and matching criteria. When trial balances are loaded, the software automatically identifies intercompany pairs, flags mismatches above a defined threshold, and generates elimination journals with a full audit trail. You review exceptions rather than building every entry from scratch. For groups managing intercompany eliminations with associates and partial consolidations, this rule-based approach handles the equity method adjustments and NCI calculations that make manual processing particularly error-prone.

Mid-market groups with 5 to 20 entities sit in an awkward gap. They have enough intercompany complexity to make manual elimination unsustainable, but enterprise platforms built for Fortune 500 groups are often oversized and overpriced for their needs. Purpose-built mid-market consolidation software fills that gap by delivering automated eliminations without requiring a six-month implementation.

4. How Do ERP and Accounting System Integrations Speed Up the Close?

Direct integrations between consolidation software and ERP or accounting systems eliminate manual trial balance exports, cutting close cycle times by 50 to 70 percent.

The trial balance bottleneck is the single biggest time drain in most mid-market closes. Before any consolidation logic can run, someone at each entity has to export their trial balance, format it to match the group template, and send it to the group finance team. If the group has ten entities running three different accounting systems (Xero in the UK, QuickBooks in the US, and Sage in South Africa), that's ten manual exports in three different formats, each requiring reformatting before they can be loaded.

Direct API integrations bypass all of that. The consolidation platform connects to each entity's accounting system and pulls trial balance data automatically. No CSV exports. No email attachments with filenames like "TB_Entity4_Final_v3_REVISED.xlsx." The data arrives in a standardized structure, already mapped to the group chart of accounts based on rules configured during setup. No reformatting.

The mixed-ERP reality deserves specific attention because it's the norm, not the exception, for mid-market groups. An acquisition typically brings a new subsidiary running whatever system it already had. Mandating a single ERP across all entities is expensive and disruptive, so most groups live with a patchwork for years. Consolidation software that integrates with QuickBooks, Xero, Sage, SAP Business One, and NetSuite simultaneously treats this heterogeneity as a design constraint rather than a problem to be solved later.

Real-time or scheduled data syncing also changes the cadence of consolidation. Instead of waiting until day five of the close for all trial balances to arrive, the group controller can see which entities have posted their final journals and which are still open. Some platforms offer dashboard views showing entity-level close status alongside the latest synced trial balance, so you know exactly where the bottleneck is at any point in the cycle.

One practical detail that often gets overlooked: integrations don't just pull numbers. The better platforms also pull account descriptions, cost centre structures, and profit centre hierarchies, which means your segmental reporting stays aligned with the source system without manual re-keying. That alignment matters because auditors increasingly ask for drill-through capability from the consolidated statements back to the entity-level source. An unbroken data chain from Xero or SAP through to the group balance sheet answers those questions in minutes rather than hours.

5. What Role Do AI and Automation Play in Financial Consolidation in 2026?

AI in financial consolidation has moved beyond marketing language into production use cases: anomaly detection, journal auto-classification, predictive close timelines, and natural language data querying.

There's an important distinction between rule-based automation and AI-driven intelligence, and conflating the two leads to confusion about what you're actually buying. Rule-based automation handles the predictable, repeatable parts of consolidation: applying elimination rules to intercompany pairs, translating foreign currency balances at closing rates, running minority interest calculations using fixed ownership percentages. These capabilities have existed in consolidation software for over a decade. They're essential, but they aren't AI.

AI adds a layer of pattern recognition and adaptive decision-making on top of that foundation. Four specific capabilities are reaching production maturity in 2026:

- Anomaly detection in intercompany balances: Instead of flagging every mismatch above a fixed threshold, machine learning models learn what "normal" variance patterns look like for each entity pair and flag only the statistically unusual ones. This reduces false positives dramatically.

- Auto-classification of journal entries: When manual adjustment journals are posted during consolidation, AI categorizes them by type (goodwill adjustment, fair value uplift, prior period correction) based on patterns in the account codes, descriptions, and amounts. This speeds up review and improves audit trail consistency.

- Predictive close timelines: By analyzing historical close data (which entities are typically late, which adjustments take longest, where review bottlenecks occur), AI models forecast the expected close completion date and highlight the tasks most likely to cause delays.

- Natural language querying: Finance teams can ask questions like "show me the top five intercompany balance mismatches this quarter" in plain English and receive structured output from the consolidated dataset, rather than building custom reports.

HighRadius, recognized as a Challenger in the 2026 Gartner Magic Quadrant for Record to Report, claims AI-powered value creation across 1,300+ enterprises. That signals institutional validation of AI in this space. The enterprise adoption numbers don't tell the mid-market story, though. Most groups with 5 to 30 entities aren't deploying AI agents for consolidation yet. They're still getting baseline automation right: reliable data pulls, consistent elimination rules, and standardized reporting.

The practical path for mid-market teams is to adopt a platform with strong rule-based automation today and evaluate AI features as they mature. Paying a premium for AI capabilities you won't use for 18 months doesn't make financial sense.

The data on mid-market AI adoption is mixed, but the trend points toward selective adoption rather than wholesale transformation. Anomaly detection and predictive close timelines are the two features most likely to deliver immediate value for groups running 10 to 20 entities, because they address real pain points (chasing variances and managing close timelines) without requiring significant change management.

6. How Does Multi-Currency Consolidation Handle Foreign Exchange Translation?

Multi-currency consolidation translates each subsidiary's financials into the group's presentation currency using IAS 21 or ASC 830 rules, applying average rates to income and closing rates to balance sheets.

The distinction between rate types is where most translation errors originate. Under both IAS 21 and ASC 830, income statement items (revenue, expenses, gains, losses) are translated at the average exchange rate for the reporting period. Balance sheet items (assets, liabilities) use the closing spot rate on the reporting date. Equity accounts follow historical rates from the date of acquisition or the date capital was contributed. Getting even one of these wrong cascades through your consolidated financial statements.

Foreign currency translation reserves (FCTR) capture the difference between translating net assets at closing rates versus the rates used for equity and retained earnings. This reserve sits in other comprehensive income within equity, not in profit or loss. For groups with subsidiaries in volatile currency markets (the Turkish lira or Argentine peso, for example), FCTR swings can materially distort the equity section of consolidated statements. IAS 29 requires entities operating in hyperinflationary economies to restate their financial statements to current purchasing power before translation, a step that many mid-market teams overlook entirely.

Consolidation software automates rate sourcing by pulling daily exchange rates from central bank feeds or commercial data providers, then applying the correct rate type per line item based on its classification. A financial controller at a South African retail group with 12 subsidiaries across six African currencies cut their FCTR reconciliation from a full day to under 30 minutes after moving off spreadsheets. The software tagged each trial balance line with its rate type (average, closing, or historical) and ran translation automatically, with no manual rate lookups required.

Two pitfalls catch teams repeatedly. First, applying closing rates to income statement items because someone copied the wrong rate column in a spreadsheet, which overstates or understates consolidated revenue depending on currency direction. Second, failing to identify hyperinflationary subsidiaries that require IAS 29 restatement before translation. If you're managing exchange rates on consolidation across more than three currencies, the manual approach isn't just slow; it's a compliance risk that auditors will flag.

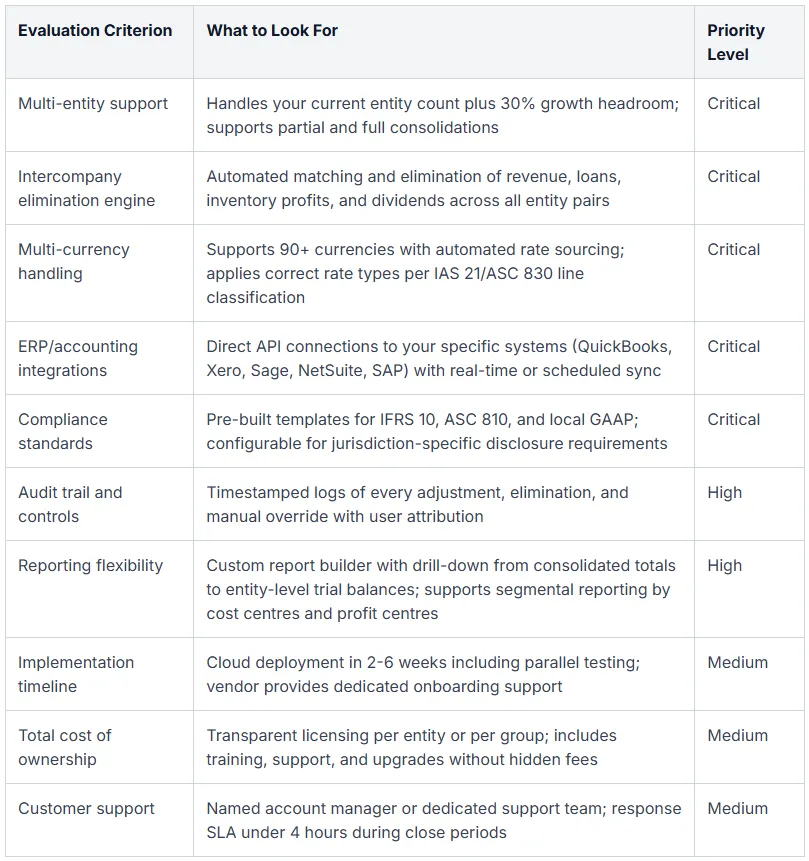

7. What Should a Buyer's Guide for Financial Consolidation Software Include?

A thorough buyer's evaluation should cover ten criteria, from multi-entity support and intercompany eliminations to total cost of ownership, deployment model, and vendor-specific RFP questions.

Most finance teams start their software search by comparing feature lists. That's the wrong starting point. Features only matter in the context of your group structure, your reporting obligations, and the accounting systems your subsidiaries already run. A ten-entity group with straightforward ownership and a single reporting standard has fundamentally different requirements than a 50-entity group with partial ownership stakes, three GAAP frameworks, and subsidiaries on four different ERPs.

The table below maps each evaluation criterion to what you should specifically look for and how to prioritize it for a mid-market finance team.

Beyond the checklist, your RFP should include questions that separate capable platforms from marketing claims. Ask vendors: "Can you demonstrate automated intercompany eliminations for loan balances across five entities in a live environment?" Ask: "How does your platform handle a subsidiary that changes its functional currency mid-year?" Ask: "What happens when an entity's trial balance is submitted late, after the consolidation has already run?"

Total cost of ownership deserves its own scrutiny. Licensing fees are only part of the equation. Implementation consulting, chart of accounts mapping, training for subsidiary controllers, and ongoing support fees can double the first-year cost. Some vendors charge per entity, others per user, and a few charge per consolidation run. Month-to-month pricing with no long-term contracts reduces the financial risk of switching if the tool doesn't fit your group's needs.

Deployment model matters less than it did five years ago. Cloud-native platforms dominate the mid-market because they eliminate infrastructure overhead and push updates automatically. On-premise deployments still exist in regulated industries where data residency requirements mandate local hosting, but for most groups with 3 to 50 entities, cloud is the default choice.

8. What Does Implementation and Onboarding Actually Look Like?

Cloud-based mid-market consolidation software typically goes live in two to six weeks, while enterprise on-premise deployments stretch to three to twelve months depending on group complexity.

The implementation timeline gap between cloud and on-premise isn't just about technology. It reflects a fundamental difference in how much configuration sits with the vendor versus your team. Cloud platforms ship with pre-built consolidation logic, standard elimination templates, and currency translation engines that work out of the box. On-premise solutions often require custom database schemas, server provisioning, and IT involvement that adds months before the finance team even touches the software.

A typical mid-market cloud implementation moves through five phases. Data migration comes first: exporting historical trial balances, opening balances, and prior-period consolidated statements into the new platform. Chart of accounts mapping follows, where each subsidiary's local account codes are linked to the group's unified structure. This phase surfaces inconsistencies you didn't know existed (one subsidiary coding intercompany loans as "other receivables" while another uses "related party balances"). Elimination rule configuration is next: defining which intercompany account pairs should net to zero and setting thresholds for acceptable matching variances. Parallel runs, where you process a consolidation simultaneously in the old spreadsheet and the new software, validate that outputs match. Go-live happens once a parallel run produces results within an acceptable tolerance, typically less than 0.5% variance on consolidated net assets.

Change management is where implementations actually stall, not the technical setup. Subsidiary controllers who've submitted trial balances via email for years resist logging into a new platform. Excel power users who built elaborate consolidation workbooks feel their expertise is being devalued. The most successful rollouts address this head-on by involving subsidiary finance staff in the parallel run phase, letting them see their own data flow through the system and verify the output matches what they'd expect.

Plan for the first close cycle after go-live to take longer than your steady-state target. Teams typically spend 20 to 30% more time on the first live consolidation because they're double-checking every output against their old process. By the second or third cycle, the time savings compound as trust in the automated outputs builds and teams stop manually verifying every elimination entry.

Training shouldn't be a one-time event. Schedule a refresher session after the second close cycle, once users have real questions based on actual experience rather than hypothetical scenarios from a demo environment.

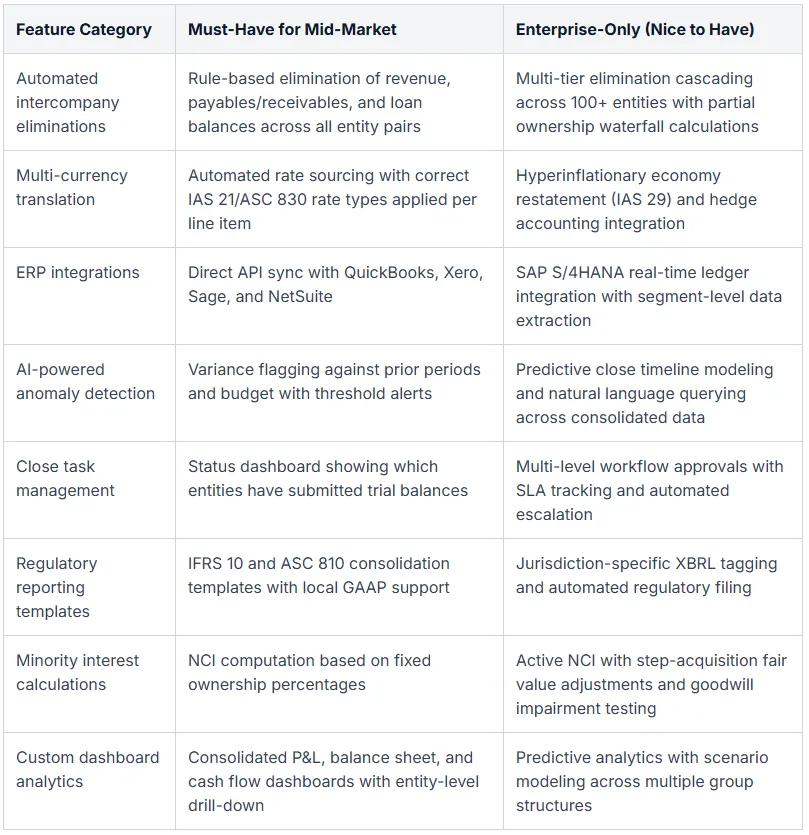

How to Choose the Right Financial Consolidation Software: Key Features at a Glance

Mid-market finance teams should prioritize automated eliminations, multi-currency translation, and direct ERP integrations, while treating AI analytics and advanced workflow tools as secondary considerations.

Not every feature on a vendor's marketing page is relevant to a group running 10 to 50 entities. Enterprise platforms built for Fortune 500 groups pack capabilities that mid-market teams will never configure, and paying for unused complexity is a poor use of budget. The table below separates must-have features from enterprise-tier extras so you can focus your evaluation on what actually affects your consolidation cycle.

The eight capabilities covered throughout this article form a decision framework, not a shopping list. Start by mapping your group's specific pain points. If currency translation errors consume two days every close, that feature jumps to the top. If your auditors consistently question elimination entries, the intercompany engine matters most. Compliance support for IFRS 10, ASC 810, or local GAAP requirements isn't optional for any group, but the depth of compliance automation you need depends on how many jurisdictions your entities report under.

The mid-market sweet spot is a platform that handles the critical six (eliminations, currency, integrations, compliance, audit trail, reporting) without requiring a dedicated IT team to maintain it.

Frequently Asked Questions About Financial Consolidation Software

What is financial consolidation software?

Financial consolidation software automates the aggregation, elimination, and reporting of financial data across multiple legal entities into unified group financial statements. It replaces manual spreadsheet processes by applying standardized rules for intercompany eliminations, currency translation, and ownership adjustments, producing audit-ready consolidated outputs.

How does the financial consolidation process work?

Each entity submits a trial balance, which is mapped to a unified group chart of accounts. The software applies consolidation adjustments: intercompany eliminations remove intra-group transactions, foreign currencies are translated to the presentation currency, and minority interest is calculated based on ownership percentages. The final output is a set of consolidated financial statements (P&L, balance sheet, cash flow) that represent the group as a single economic entity.

What are the key features to look for in financial consolidation software?

Multi-entity support, automated intercompany eliminations, and multi-currency handling are non-negotiable. Direct ERP integrations with systems like QuickBooks, Xero, and Sage eliminate manual data exports. Compliance templates for IFRS and US GAAP, a full audit trail, and flexible reporting round out the core feature set.

How long does it take to implement financial consolidation software?

Cloud-based mid-market solutions go live in two to six weeks. That timeline covers data migration, chart of accounts mapping, elimination rule configuration, and at least one parallel test run against your existing process.

Can financial consolidation software handle multiple currencies and accounting standards?

Yes. Modern platforms automate foreign currency translation by applying average rates to income statement items and closing spot rates to balance sheet items, following IAS 21 and ASC 830 requirements. Most support IFRS 10, ASC 810, and local GAAP reporting standards simultaneously, so groups operating across multiple jurisdictions can produce compliant consolidated statements from a single platform.

Ready to Close the Books Faster Across Every Entity?

If your finance team is still stitching together consolidations across multiple entities using spreadsheets, the close cycle will only get harder as the group grows. Automated multi-entity consolidation with month-to-month pricing and no long-term contracts removes that risk. See how it works for your group: Group Financial Consolidation.