7 Features That Define Good Consolidated Financial Statements Software

The financial consolidation software market reached USD 2.70 billion in 2024 and is projected to hit USD 6.41 billion by 2032, growing at 11.4% CAGR according to Credence Research. That growth reflects a real operational shift: groups are adding subsidiaries, operating across more currencies, and facing tighter reporting deadlines under IFRS and US GAAP.

Not every consolidation statement tool solves the same problems. Some platforms automate intercompany eliminations and multi-currency translation with precision. Others are glorified spreadsheet templates that still require manual journal entries and offline reconciliation. The features you prioritize during evaluation determine whether the software cuts days from your close cycle or quietly introduces new bottlenecks.

The seven features below separate dedicated group financial statements platforms from generic accounting add-ons. Each section covers what to look for, what to test during a demo, and where finance teams most often get burned by feature gaps.

1. How Does Automated Intercompany Elimination Save Time?

Automated intercompany eliminations software removes intra-group revenue, expenses, receivables, and payables, preventing double-counting that distorts consolidated group financial statements across all reporting periods.

Mismatched intercompany balances rank among the most common audit findings for multi-entity groups. A subsidiary records a sale to its parent at one amount; the parent books the corresponding purchase at a slightly different figure due to timing, FX rounding, or data entry. In a spreadsheet, that mismatch hides until an auditor flags it. In a dedicated consolidation platform, it gets caught before the trial balance reaches the consolidation pack.

The capabilities that matter most in intercompany eliminations software break down into four specific areas:

- Automatic balance matching that pairs intercompany receivables against payables across entities, with tolerance thresholds configurable per currency or entity pair

- Rule-based elimination journals that fire on consolidation without manual posting, covering revenue/cost of sales, loan balances, dividends, and management fees

- Exception flagging that surfaces unmatched items in a queue so the controller can resolve them before sign-off, rather than discovering them mid-audit

- Full audit trails on every elimination entry, showing who created the rule, when it last ran, and what amounts it processed

Teams running eliminations manually often don't realize how much rework they absorb. One misstated intercompany loan balance cascades through NCI calculations, segmental reporting, and the group cash flow statement. Avoiding common consolidation mistakes starts with removing the manual steps that introduce them. Continuous intercompany reconciliation, where balances are matched throughout the period rather than only at month-end, is an emerging capability that further reduces close-day surprises.

2. What Does Multi-Currency Consolidation Really Require?

Multi-currency consolidation requires applying closing, average, and historical exchange rates to specific line items per IAS 21, then recognizing translation differences in the foreign currency translation reserve.

Simple currency conversion (multiplying everything by one rate) is the fastest way to produce a consolidated report that fails an audit. IAS 21 prescribes a more granular approach: assets and liabilities translate at the closing rate, income and expenses at the average rate for the period, and equity at historical rates. The difference flows into the foreign currency translation reserve in equity, not through profit or loss.

Consider a group headquartered in the UK with a subsidiary reporting in South African rand. If the ZAR weakens 8% against GBP during the reporting period, the subsidiary's net assets shrink on translation, but its revenue translates at the period average, a less dramatic rate. Getting this wrong overstates or understates group equity, and auditors will trace the FCTR movement line by line.

When evaluating any group financial statements platform for exchange rate handling, test these specifics:

- Can you assign different rate types (closing, average, historical) per account or account group?

- Does the system let you lock FX rates per period so prior-period consolidations don't shift when new rates load?

- Is there an audit trail showing which rate was applied to each line item, and who approved rate overrides?

- Can you integrate live or scheduled FX feeds while retaining manual override control for board-approved rates?

Groups operating across three or more currencies should treat strong multi-currency logic as non-negotiable. A tool that only supports a single conversion rate per entity per period forces workarounds in spreadsheets, which defeats the purpose of automating the consolidation cycle.

3. Why Is IFRS and GAAP Compliance a Non-Negotiable Feature?

Consolidated financial statements software must enforce IFRS 10 or ASC 810 consolidation rules, including NCI calculations, goodwill tracking, and framework-aligned disclosure templates for audit-ready output.

The common advice is that your ERP can handle group consolidation. Most ERP consolidation modules were built for transactional processing, not for the specific logic that IFRS 10 or ASC 810 demands. An ERP will post journals, run trial balances, and produce single-entity financials confidently. Ask it to calculate non-controlling interest on a step acquisition, track goodwill impairment across reporting periods, or generate disclosure notes that satisfy an IFRS checklist, and you'll likely end up building that logic yourself in spreadsheets bolted alongside the ERP.

Dedicated consolidated financial statements software approaches compliance differently. The platform encodes the framework rules directly. When you add a 70%-owned subsidiary, the system automatically calculates the 30% NCI on consolidation, allocates goodwill based on acquisition-date fair value entries, and carries those balances forward with impairment testing support. Gartner's structured reviews of financial close and consolidation solutions consistently rank regulatory compliance as a top adoption driver. Getting compliance wrong isn't a rounding issue; it's a restatement risk.

Features that separate compliant platforms from basic consolidation tools include:

- Pre-built report templates aligned to IFRS or US GAAP disclosure requirements

- Automatic NCI allocation across profit or loss, OCI, and equity

- Goodwill and intangible asset registers with impairment tracking

- Statutory reporting packs for multi-entity close across jurisdictions

If your current tool requires you to manually compute minority interest or maintain a separate goodwill schedule in Excel, you have a reporting layer with a gap underneath it, not a consolidation platform.

4. How Should the Software Integrate With Your Existing ERP and Accounting Systems?

Effective consolidation software pulls trial balances directly from ERPs and accounting systems via API, eliminating CSV exports and manual uploads that introduce transcription errors each period.

A consolidation statement tool that can't talk to your accounting system creates a parallel manual process. Every period, someone exports trial balances from Xero, QuickBooks, or Sage, reformats them into the consolidation template, uploads them, and checks that nothing was lost in translation. That workflow eats hours and introduces transcription risk at the exact moment when the finance team is under the most pressure.

The integration question to ask during any demo is direct: does the platform pull data automatically, or does it wait for you to push files? API-first platforms connect directly to your general ledger, map accounts to the group chart of accounts once, and then sync trial balances on a schedule you define. Cloud-native tools that integrate with QuickBooks, Xero, and Sage tend to offer stronger connector ecosystems than on-premise solutions relying on flat-file imports.

Beyond the initial connection, evaluate integration depth. Can the system handle QuickBooks integration with automated trial balance mapping so new accounts in the subsidiary ledger get flagged rather than silently dropped? Does it support scheduled syncs (nightly, weekly, on-demand) without IT involvement? Can it harmonize data from entities running different accounting systems into a single consolidated trial balance without manual re-keying?

On-premise tools requiring middleware or custom scripts for every new entity connection become a bottleneck as the group grows. For groups with five or more entities across different accounting systems, integration depth should rank alongside elimination logic and multi-currency support in your scoring criteria.

5. What Audit Trail and Data Integrity Controls Should You Expect?

Consolidated financial statements software should provide immutable, journal-level audit trails with user stamps, period locking, and automated balance validation before report finalization.

Auditors don't just want to see your consolidated numbers. They want to click on a line item and trace it back through every elimination, every currency translation, every manual adjustment, all the way to the originating trial balance in the subsidiary ledger. If your software can't do that in a few clicks, your first external audit on the platform will be painful.

The controls that matter most during evaluation are ones you won't think to ask about in a demo. Journal-level drill-down lets auditors inspect each consolidation adjustment individually. User-stamped changes record who made an entry, when, and why, satisfying SOX and IFRS disclosure requirements around management judgement. Period locking prevents anyone from editing a closed month after sign-off, a control that sounds obvious until you discover a subsidiary accountant reopened March to "fix" a posting in June. Version control on consolidation runs means you can compare this month's output against last month's to pinpoint exactly what changed.

Before any consolidation run is finalized, the platform should run automated health checks: do debits equal credits across all entities, do intercompany balances net to zero, are there orphaned transactions without a matching counterparty? These pre-close validations catch errors that would otherwise surface during audit fieldwork. Groups that fail the audit test almost always trace the failure back to missing controls at this stage, not to incorrect accounting logic.

6. Does the Platform Support Real-Time Consolidation and Reporting?

Modern cloud-based consolidation platforms can execute full group consolidations in under 15 minutes, replacing batch processing that traditionally consumed entire working days.

Period-end batch consolidation forces finance teams into a predictable crunch: wait for all subsidiaries to close, upload data, run the consolidation overnight, review errors the next morning, fix, rerun. That cycle compresses reporting timelines and leaves zero room for analysis. On-demand consolidation flips this model. You run a full consolidation whenever you need one, mid-month for a board query or weekly for management reporting, without waiting for a formal close.

Cloud-based financial consolidation software vendors now deliver group consolidation completion times measured in minutes rather than hours. The practical benefit goes beyond speed. When a consolidation takes 15 minutes instead of 8 hours, the group accountant can rerun it after correcting a single subsidiary's data without losing an entire day. That rerun capability, with full auditability intact on each version, is the real differentiator.

A mid-market group with 12 subsidiaries across 4 currencies illustrates the impact clearly. Under a batch model, their monthly close stretched to 8 working days because each correction required a full reprocessing queue. Switching to on-demand consolidation cut that to 4 days, not because the accounting changed but because the feedback loop between error detection and correction collapsed from overnight to near-instant. When evaluating platforms, ask the vendor to run a live consolidation during the demo with realistic data volumes. Processing time under controlled conditions tells you more than any sales deck.

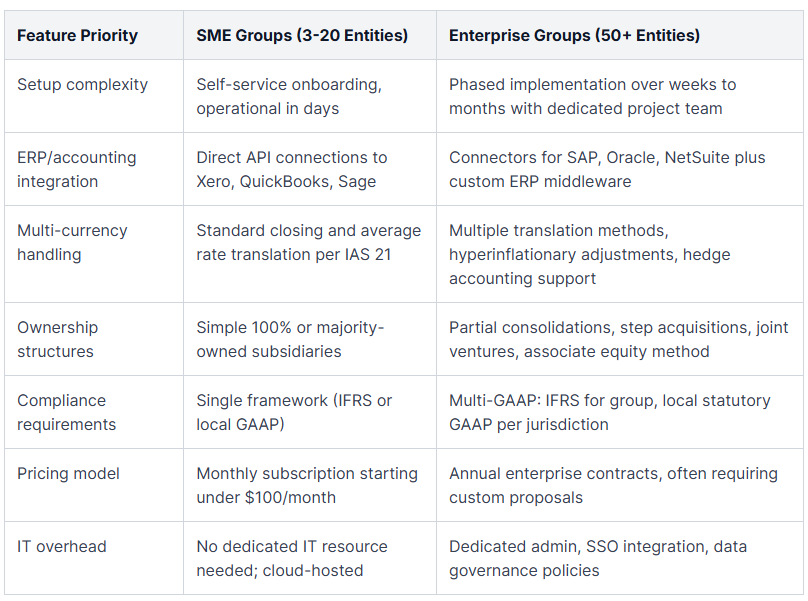

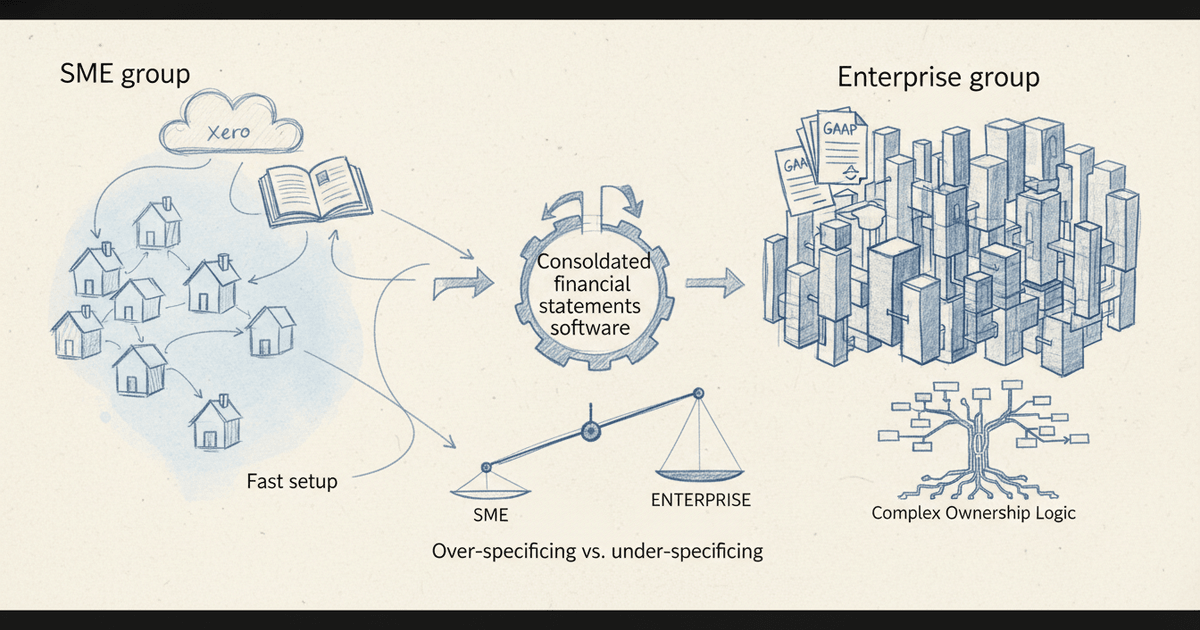

7. How Do You Evaluate Software for SMEs vs Enterprise Groups?

SME groups with 3 to 20 entities need fast setup and cloud accounting integrations, while enterprise groups with 50-plus entities require multi-GAAP reporting and complex ownership logic.

Over-specifying is just as costly as under-specifying. An SME group running 8 subsidiaries on Xero doesn't need role-based access controls for 200 users or proportional consolidation logic for joint ventures it will never have. Paying for that complexity means paying for configuration time, training overhead, and a steeper learning curve that slows down a lean finance team. Conversely, an enterprise group with partial ownership stakes across three jurisdictions and dual IFRS/US GAAP reporting can't rely on a lightweight tool designed for straightforward 100%-owned structures.

The table below maps the practical differences across the evaluation criteria that matter most.

Self-identifying where your group sits on this spectrum before shortlisting vendors saves weeks of wasted demos. A 10-entity group in South Africa with a single reporting framework has entirely different priorities than a 60-entity multinational filing in three jurisdictions. Start with the row that represents your biggest pain point and evaluate from there.

Frequently Asked Questions About Consolidated Financial Statements Software

What is consolidated financial statements software?

It automates the combination of financial data from a parent company and its subsidiaries into unified group financial statements. The software handles intercompany eliminations, foreign currency translation, NCI calculations, and disclosure formatting that would otherwise require extensive manual spreadsheet work across multiple entities.

How does consolidated financial statements software handle intercompany eliminations?

Configurable matching rules automatically identify intra-group transactions (revenue against cost of sales, receivables against payables, intra-group loans) and eliminate them. When a mismatch exists, say one subsidiary recorded a sale of £50,000 but the counterparty only booked £49,200, the system flags the difference for manual review rather than silently netting it off.

What is the difference between financial consolidation and financial close?

Financial close finalizes a single entity's books for a reporting period. Consolidation is the step after, combining those closed books into group statements. The two processes are sequential: you can't consolidate data that hasn't been closed, though some platforms support both workflows in a single environment.

Can consolidation software integrate with QuickBooks, Xero, or Sage?

Yes. Cloud-native platforms typically connect via API to pull trial balances directly, removing the need for CSV exports each period.

How long does it take to implement consolidated financial statements software?

For SME groups with straightforward ownership, cloud platforms can be operational within a few days since there's minimal configuration beyond mapping chart of accounts and setting up entity hierarchies. Enterprise implementations with custom ERP connectors, complex ownership chains, and multi-GAAP requirements typically take several weeks to a few months depending on the number of subsidiaries and jurisdictions involved.

Find the Right Consolidation Statement Tool for Your Group

You now have seven concrete criteria to score any consolidation platform against: intercompany eliminations, multi-currency handling, IFRS/GAAP compliance, ERP integration, audit trail controls, real-time processing, and SME-vs-enterprise fit. Explore Quick Consols' financial consolidation software with a live demo using your own group data to see how these features hold up in practice.

Get the latest updates, exclusive content, and exciting news delivered right to your inbox.

Share this Article

Get in touch!

If you have any questions about our Consolidation Software, send us a message below and we'll get back to you ASAP.