Equity Accounting vs Proportionate Consolidation: The Policy Choice That Shapes Your Financial Statements

Pick the wrong method for a joint venture and your balance sheet tells a different story than it should. Leverage ratios shift. ROA moves. Audit questions multiply. The choice between equity accounting and proportionate consolidation is not a stylistic preference. It is a policy decision that reshapes how your group financial statements read.

The core question is straightforward. When a parent holds a stake in another entity but does not fully control it, does the group bring in a single equity-method line representing its share of net assets? Or does it absorb a proportionate share of every asset, liability, revenue, and expense line by line?

The headline answer for finance teams reporting under IFRS is blunt. Since IFRS 11 became effective for periods beginning on or after 1 January 2013, replacing IAS 31, proportionate consolidation is no longer permitted for joint ventures. The old IAS 31 policy choice between proportionate consolidation and the equity method is gone. Under US GAAP, proportionate consolidation survives, but only in narrow industry pockets.

This article works through the decision properly. We define both methods. We unpack the significant influence threshold and the 20%-50% ownership band. We run a worked example showing identical net profit but vastly different gross numbers. We walk through the ratio impact on leverage, ROA, and ROE. And we close with a practical decision framework for multi-entity groups navigating IFRS, US GAAP, or both.

What Is the Equity Method of Accounting?

The equity method is the quieter of the two approaches. It compresses a meaningful economic interest into a single line on the balance sheet. That line, usually labelled 'Investment in associate' or 'Investment in joint venture', represents the investor's proportionate share of the investee's net assets. No gross assets pulled in. No gross liabilities. Just one number that moves period to period.

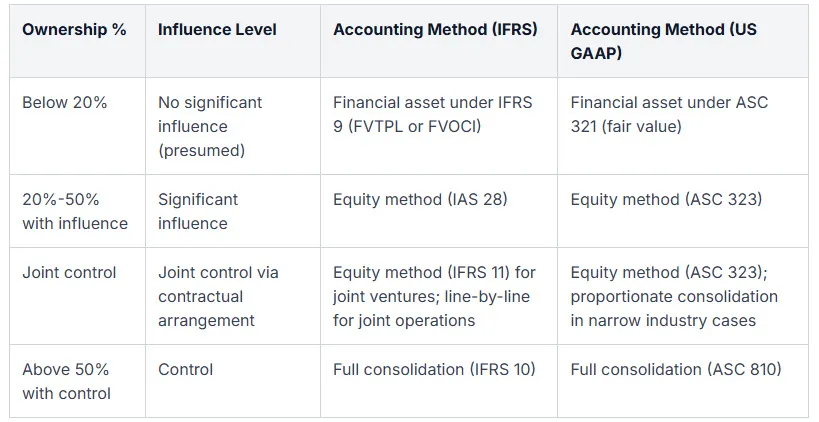

It applies when the investor has significant influence but not control. IAS 28 presumes significant influence when an investor holds 20% or more of the voting power of the investee, directly or indirectly. The presumption can be rebutted either way. Influence at 18% is possible. Absence of influence at 25% is possible. Substance over form.

The mechanics are clean. Initial recognition is at cost. After that, the carrying value moves with the investee's performance. Under the equity method, the investment is initially recorded at cost and subsequently adjusted for the investor's share of the investee's earnings and losses. Share of profits increases the carrying value. Share of losses reduces it. Dividends received reduce it. Share of OCI movements, like foreign currency translation reserves and revaluation gains, flow through OCI in the investor's accounts.

The income statement treatment is just as compact. The investor's share of the investee's profit or loss appears as a single line, typically 'share of profit from associate' or 'share of profit from joint venture'. No revenue. No cost of sales. No operating expenses. The investee's gross numbers stay out of the investor's top line entirely.

Governance sits across two standards. IAS 28 covers the equity method under IFRS. ASC 323 governs it under US GAAP, presuming significant influence at 20%-50% of voting stock. Both standards apply the equity method to associates without exception. For joint ventures, IFRS 11 mandates the equity method. US GAAP also defaults to the equity method for most joint ventures, with narrow exceptions.

For finance teams running a multi-entity group, the equity method is the default treatment for associates and joint ventures. The reporting impact is contained, the trial balance pull is lighter, and intercompany eliminations with associates follow a specific partial-elimination logic that differs from full subsidiary eliminations.

What Is Proportionate Consolidation?

Proportionate consolidation works on a completely different principle. Rather than collapsing the investee into one line, the investor recognises its proportionate share of each individual asset, liability, income, and expense line by line. The investee's economic reality is woven directly into the group accounts.

A simple illustration. Investor Co holds a 40% interest in JV Co. Under proportionate consolidation, Investor Co adds 40% of JV Co's cash, 40% of its receivables, 40% of its inventory, 40% of its payables, and 40% of its loans to its own balance sheet. The same logic runs through the income statement. 40% of JV Co's revenue, 40% of its cost of sales, 40% of its operating expenses. Everything scales by the ownership percentage.

This was the historic treatment for jointly controlled entities under the old IAS 31. Finance teams reporting under IFRS had a policy choice between proportionate consolidation and the equity method, and many groups, especially in extractive industries and infrastructure, leaned proportionate to reflect the operational reality of the venture.

That choice is gone for IFRS preparers. IFRS 11 eliminated proportionate consolidation for joint venture arrangements, replacing it with the equity method in accordance with IAS 28. The change was deliberate. The IASB took the view that proportionate consolidation inflated assets and liabilities the investor did not actually control.

Under US GAAP, the method is not extinct. Most joint ventures are accounted for using the equity method under ASC 323, while proportionate consolidation is permitted in limited circumstances for unincorporated entities in construction and extractive industries. Oil and gas joint operations, mining ventures, and certain real estate arrangements still use it. The exceptions are narrow but real, and dual-reporting groups need to track them.

A critical distinction sits underneath. Proportionate consolidation is not full consolidation. Full consolidation brings in 100% of the subsidiary's line items and recognises a non-controlling interest for the share the parent does not own. Proportionate consolidation skips the NCI entirely. It only brings in the investor's share. No minority interest. No grossing up and stripping back. Just a partial line-by-line absorption.

For finance teams, the operational implication is that proportionate consolidation requires the same trial balance pull, intercompany mapping, and foreign currency translation discipline as full consolidation, just scaled by the ownership percentage.

How Is Significant Influence Determined and When Does Each Method Apply?

Significant influence is the gateway test. Get it wrong and the wrong method gets applied. IAS 28 presumes significant influence exists when an investor holds 20% or more of the voting power of the investee, and presumes significant influence does not exist when an investor holds less than 20% of voting power, unless influence can be clearly demonstrated. The thresholds are presumptions, not bright lines. Substance overrides the percentage when the qualitative evidence points the other way.

The qualitative indicators matter as much as the ownership stake. IAS 28 lists representation on the board of directors, participation in policy-making, material transactions between the investor and investee, interchange of managerial personnel, and provision of essential technical information. Any one of these can establish influence at 18% ownership. Equally, their absence can rebut the presumption at 25%.

Below the 20% threshold, the default treatment is different entirely. Equity investments below the 20% significant-influence threshold are generally measured at fair value through profit or loss or other comprehensive income, not under the equity method. The investment becomes a financial asset, not an associate.

The upper boundary matters just as much. Control flips the treatment. The equity method is not applied when the investor has control, typically more than 50% of voting rights, in which case full consolidation under IFRS 10 applies. Joint control is its own category. Where two or more parties share control under a contractual arrangement, the equity method applies under IFRS regardless of the individual percentage. Under US GAAP, joint ventures default to the equity method, with proportionate consolidation reserved for the narrow industry exceptions.

Method transitions are where finance teams quietly burn audit hours. Step acquisitions trigger remeasurement. Partial disposals do too. A stake that moves from 18% to 22% may shift from financial asset to associate. A stake that moves from 45% to 55% triggers full consolidation and a fresh purchase price allocation. Our resources on these transition mechanics walk through the journal-entry sequencing.

The practical workflow for the group accountant is to test ownership at every reporting date, test the qualitative indicators alongside it, and document the conclusion. The trial balance pull, intercompany elimination treatment, and segmental reporting all flow from that classification. (presumes significant influence does not exist when an investor holds less than 20% of voting power, unless influence can be clearly demonstrated)

IFRS 11 vs US GAAP: Why the Two Methods Diverged

The divergence between IFRS and US GAAP on joint venture accounting is not an accident. It is a deliberate standard-setting split that finance teams running dual-reporting groups have to live with every quarter.

IFRS 11 is effective for annual periods beginning on or after 1 January 2013 and requires joint ventures to be accounted for using the equity method under IAS 28. It replaced IAS 31, and with it, the policy choice that let preparers pick between proportionate consolidation and the equity method. The standard also reframed the underlying classification. Joint arrangements are now either joint operations or joint ventures, and the distinction drives the accounting.

For joint operations, IFRS 11 requires a party to recognize its assets, liabilities, revenue, and expenses line-by-line, including its share of jointly held or incurred items. That looks like proportionate consolidation in practice, but it is grounded in a different concept: the parties have direct rights to assets and direct obligations for liabilities, so the line-by-line treatment reflects substance, not policy choice.

For joint ventures, IFRS 11 eliminated proportionate consolidation for joint venture arrangements, replacing it with the equity method in accordance with IAS 28. The IASB's reasoning was uncompromising. Proportionate consolidation, in their view, overstated assets and liabilities that the investor did not actually control. A 40% share of a JV's borrowings sat on the balance sheet as if the investor had a direct obligation, when in legal substance it did not. The standard chose faithful representation over operational familiarity.

US GAAP took the other road. ASC 323 defaults joint ventures to the equity method, but ASC 810 provides narrow exceptions permitting proportionate consolidation for certain unincorporated construction and extractive industry ventures. Oil and gas working interests are the textbook case. The exception is industry-bound and structurally specific, not a general policy choice.

Here is the part that gets under-explained. A dual-reporting group with a US parent and an IFRS-reporting subsidiary can end up accounting for the same joint venture two different ways in two different sets of statements. The IFRS group accounts apply the equity method. The US GAAP filings may apply proportionate consolidation if the JV qualifies under ASC 810's narrow industry carve-outs. Both sets of statements are technically correct. Both can be audited and signed off. But the gross assets, gross liabilities, revenue, and leverage ratios will differ materially.

This is the reporting trap. Free explainer content rarely walks past the headline that 'IFRS removed proportionate consolidation'. The interaction with US GAAP, the joint operation versus joint venture classification, and the dual-reporting implications are where the real audit risk sits.

Worked Example: Same Joint Venture, Both Methods Side by Side

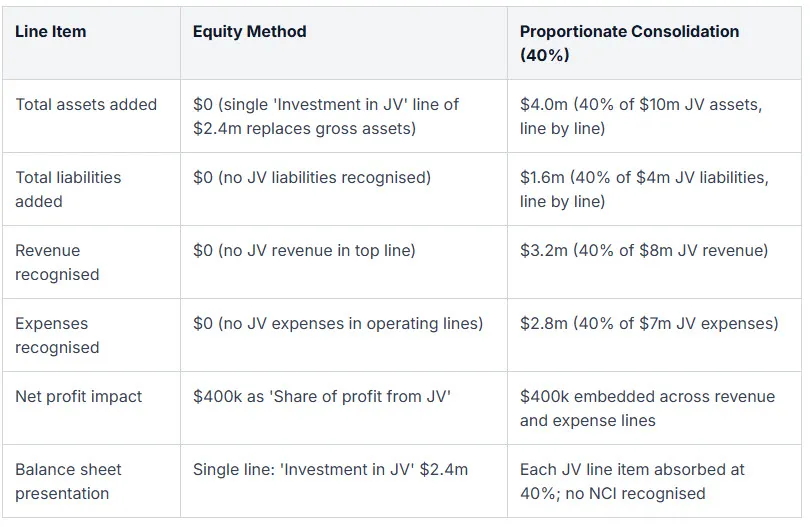

Numbers settle the debate faster than theory. Set up a clean scenario. Investor Co holds 40% of JV Co. JV Co's financials are straightforward: total assets of $10m, total liabilities of $4m, equity of $6m, revenue of $8m, expenses of $7m, and net profit of $1m.

Under the equity method, the treatment is compact. Investor Co's balance sheet shows a single line, 'Investment in JV', carried at $2.4m. That is 40% of JV Co's $6m equity, assuming the investment was originally acquired at fair value with no goodwill or fair value adjustments outstanding. The income statement shows one line, 'Share of profit from JV', at $400k. That is 40% of JV Co's $1m profit. Nothing else from JV Co touches Investor Co's accounts.

Under proportionate consolidation, the picture changes dramatically. Investor Co's balance sheet absorbs $4m of JV Co's assets, calculated as 40% of $10m, line by line. Cash, receivables, inventory, property, all scaled at 40% and added to Investor Co's existing balances. The liability side absorbs $1.6m, calculated as 40% of $4m. Trade payables, accrued expenses, borrowings, all scaled and added. The income statement absorbs $3.2m of revenue (40% of $8m) and $2.8m of expenses (40% of $7m). Net profit impact: $400k.

The net profit is identical under both methods. That is the point that often gets missed. The bottom line does not change. What changes is everything above it: gross revenue, gross expenses, total assets, total liabilities, and every ratio that uses those gross figures as inputs.

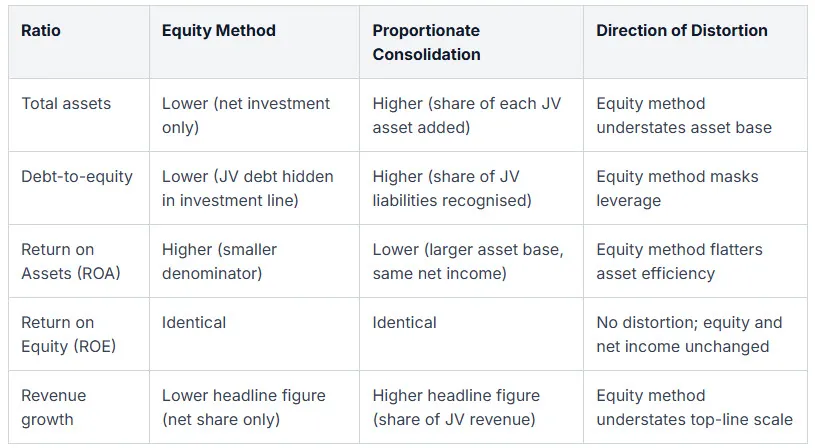

The ratio impact is material. Total assets are higher under proportionate consolidation by $4m. Total liabilities are higher by $1.6m. Debt-to-equity rises. Debt-to-assets rises. Return on assets falls, because the same net income is divided by a larger asset base. Return on equity stays roughly comparable, because both the numerator and denominator effects are concentrated on the asset and liability sides.

Intercompany eliminations introduce another layer. Under full consolidation, intercompany trades are eliminated 100%. Under proportionate consolidation, they are eliminated only to the extent of the investor's share, which is a partial elimination that catches teams off guard. Under the equity method, intercompany transactions with associates and joint ventures require partial elimination against the equity-method line itself, not against the gross transaction. The mechanics of eliminating intercompany transactions with associates differ meaningfully from full subsidiary eliminations, and the journal sequencing is where errors compound.

The takeaway for the worked example is simple. Same economic interest, same net profit, two completely different sets of financial statements. The leverage profile, the asset turnover, and the return on assets all read differently to a lender, an analyst, or a credit committee.

Impact on Key Financial Ratios: Leverage, ROA, and ROE

Ratios are where the choice of method stops being academic. Two companies with identical economic exposure can look like very different businesses depending on whether the joint venture lands inside the balance sheet or sits on one line.

Start with total assets. Under proportionate consolidation, the investor's share of every JV asset moves onto the consolidated balance sheet. Under the equity method, only the net investment shows up. Same economics, smaller asset base. The gap can be material when the JV is capital-intensive.

Liabilities follow the same logic. The equity method tucks the investor's share of JV debt inside the 'Investment in JV' line, where it is invisible to a quick read. Proportionate consolidation lifts that debt into plain sight. For lenders running covenant tests, this is not a cosmetic difference.

Now the ratios:

- Debt-to-equity rises under proportionate consolidation because the JV's liabilities are added to the group's. Under the equity method, the same leverage sits off-balance-sheet in substance.

- Return on Assets falls under proportionate consolidation. The numerator is unchanged, but the denominator grows. Equity method ROA looks healthier for the same (AnalystPrep's CFA Level II notes) underlying business.

- Return on Equity is identical under both methods. Net income and net equity are unchanged. ROE is the one ratio analysts can trust across methods without adjustment.

- Revenue growth and operating margins diverge sharply. Proportionate consolidation pulls JV revenue and costs into the top of the income statement. The equity method shows only the net share of profit on a single line below operating profit.

This is exactly why critics of IFRS 11 keep pushing back. Removing proportionate consolidation simplified the rules. It also made off-balance-sheet leverage easier to miss in capital-intensive joint ventures. Analysts covering mining, construction, and energy still rebuild proportionate disclosures by hand to see the real leverage profile.

For finance teams, the implication is practical. Equity method statements are compliant under IFRS, but stakeholders often want both views. Build a consolidation process that can produce supplementary proportionate disclosures without rebuilding the model from scratch. The Quick Consols knowledge base on when equity accounting stops and starts is a useful reference point for teams reviewing their policy.

How to Choose: A Decision Framework for Finance Teams

Choosing a method is not a judgement call when the standards are read carefully. It is a sequence. Walk through it in order and the answer falls out.

Step 1: Identify the reporting framework. If the group reports under IFRS, the choice for joint ventures is already made. IFRS 11.24 requires the equity method, with no policy option. If the group reports under US GAAP, move to step 2. Dual reporters need a documented reconciliation policy, not a single answer.

Step 2: Classify the arrangement. Joint operation, joint venture, associate, or controlled subsidiary. The classification drives everything. Joint operations recognise the investor's share of assets, liabilities, revenue, and expenses line-by-line, as set out in the IFRS 11 joint operation guidance from AnalystPrep. Joint ventures get the equity method under IFRS. Associates use the equity method. Controlled subsidiaries get full consolidation.

Step 3: Test the US GAAP exception. For US GAAP joint ventures, check whether the narrow proportionate consolidation carve-out applies. The Universal CPA guidance on US GAAP joint venture definitions confirms the exception is limited to unincorporated entities in specific industries, mainly construction and extractive. If the JV is incorporated or sits outside those industries, the equity method applies. Stepped acquisitions and ownership shifts deserve their own technical review, and the Quick Consols write-up on phased subsidiary purchases is a useful starting reference.

Step 4: Map analyst and lender expectations. Banks and rating agencies often require proportionate disclosure for covenant calculations even when the primary statements use the equity method. Find out before the audit, not after a covenant test fails. Build the supplementary schedule into the close, not into a panic the week before reporting.

Step 5: Plan for ownership changes. Document the policy for step acquisitions, dilutions, partial disposals, and loss of significant influence. Each event has a remeasurement consequence. A clear written policy keeps the auditor conversation short.

Step 6: Check the software. A consolidation platform that handles only the equity method forces manual workarounds the moment a US GAAP exception or a supplementary disclosure appears. Pick a tool that handles both methods, intercompany eliminations at the correct percentage, and consistent FX translation across periods.

Follow the six steps and the right method is rarely ambiguous. Skip a step and the audit team finds it later.

How Consolidation Software Handles Each Method in Practice

Software is where method choice meets the close calendar. The mechanics of each approach are well understood. The execution is where teams burn hours.

Equity method workflow. The platform takes the investee's reported profit or loss, applies the ownership percentage, and posts the investor's share to the income statement. The investment carrying value moves with each period's share of earnings, dividends received reduce the carrying amount, and OCI movements flow through their own line. Done well, this is a few automated journals. Done in spreadsheets, it is a reconciliation every quarter and a fresh argument with the auditor about cumulative movements.

Proportionate consolidation workflow. The trial balance of the joint venture is multiplied by the investor's percentage, line by line, and merged into the group consolidation. Every account: cash, receivables, PP&E, debt, revenue, cost of sales. The software needs to apply the percentage cleanly, tag the entries to the JV entity, and keep the source data auditable. Manual versions of this work in a small group. They collapse the moment ownership percentages change mid-year or a new JV enters the structure.

Intercompany eliminations differ by method. Under full consolidation, intercompany transactions are fully eliminated. Under proportionate consolidation, eliminations run only to the extent of the investor's share. Under the equity method, no elimination is required for most transactions, though unrealised profits in inventory still need adjusting against the investment carrying value. Software that treats these as the same flow produces wrong numbers.

Multi-currency complexity. Both methods need FCTR handling, but the touchpoints differ. Equity method translation runs through the investment line and a translation reserve. Proportionate consolidation translates each line at the appropriate rate, with the residual moving through FCTR. Manual reconciliation of these movements is where most spreadsheet groups lose a day every close.

Audit trail requirements. Regulators want documented method selection, threshold testing, consistency across periods, and a clear link from the JV's source trial balance to the consolidated number. A platform with automated intercompany eliminations and a fixed audit trail removes most of the friction. When ownership percentages shift or new ventures appear, the workflow holds together instead of breaking.

The pattern is consistent across multi-entity groups. Manual processes work until they don't. The moment a second joint venture is added, or an ownership change lands mid-year, the spreadsheet model needs rebuilding.

Frequently Asked Questions

What is the main difference between equity accounting and proportionate consolidation?

The equity method shows the investment as a single line on the balance sheet, updated for the investor's share of profit, dividends, and OCI. Proportionate consolidation brings in the investor's percentage of each individual asset, liability, revenue, and expense. Net profit and net equity end up identical under both methods. Gross assets, liabilities, revenue, and operating margins look very different.

Is proportionate consolidation still allowed under IFRS?

No. IFRS 11, effective from 1 January 2013, removed proportionate consolidation for joint ventures. Joint ventures must use the equity method under IAS 28. Joint operations are a separate classification: the investor recognises its share of assets, liabilities, revenue, and expenses directly under IFRS 11.15-16. That is line-by-line recognition based on rights and obligations, not proportionate consolidation of a separate entity.

How is significant influence determined for the equity method?

Significant influence is presumed at 20% or more of voting power under IAS 28 and at 20%-50% under US GAAP ASC 323. The assessment also weighs qualitative factors: board representation, participation in policy-making, material intercompany transactions, interchange of managerial personnel, and provision of essential technical information. Substance overrides the percentage. Influence below 20% is possible but must be clearly demonstrated.

Does a joint venture always involve equity?

Not necessarily. A joint venture is defined by joint control, not by equity contribution. Parties can contribute cash, assets, services, intellectual property, or any combination. The accounting classification depends on the rights and obligations the arrangement creates for each party, and on whether the vehicle is a separate legal entity. Equity issuance is one mechanism, not the defining feature.

How do US GAAP and IFRS differ on joint venture accounting?

IFRS 11 mandates the equity method for every joint venture, with no policy choice. US GAAP under ASC 323 also defaults to the equity method but permits proportionate consolidation in narrow circumstances: unincorporated entities in construction and extractive industries, with limited application elsewhere under ASC 810. Dual reporters end up with the same answer in most cases but need a documented policy for the exceptions.

What happens when ownership crosses the 20% or 50% threshold?

Crossing 20% upward usually triggers a move from fair value accounting under IFRS 9 to the equity method, with remeasurement at the date of transition. Crossing 50% triggers full consolidation under IFRS 10, treated as a business combination. Falling below 20% with loss of significant influence ends equity method accounting; the retained investment is remeasured to fair value through profit or loss.

Get Your Joint Venture Accounting Right With Quick Consols

Joint venture accounting punishes the small mistakes. A misapplied percentage, a missed elimination, a method drift between periods. The audit team finds all of them. The numbers stop tying back. The close runs long.

Finance teams need software that handles both the equity method and proportionate consolidation correctly, under IFRS and US GAAP, without manual spreadsheet workarounds every time ownership shifts. That means automated share-of-profit calculations, partial intercompany eliminations at the correct percentage, clean FCTR handling on translated joint ventures, and an audit trail that ties the JV's trial balance to the consolidated number.

Quick Consols is built for this. The platform automates method selection, eliminations, FX translation, and the supplementary disclosures regulators and lenders look for. Multi-entity, multi-currency groups run their close in a single source of truth instead of stitching together quarterly workbooks. Audit-ready packs come out of the system, not out of a final-week scramble.

If joint ventures are pushing your close calendar, book a demo of Group Financial Consolidation and see the equity method and proportionate workflows run end-to-end on your structure. Bring a real trial balance. Watch the numbers settle in minutes instead of days.