How to calculate NCI (Non-controlling interests)

I’m not usually one to start with a disclaimer but this article was written by a human (yours truly) and is not intended to be a complete guide to every NCI scenario, but rather to give you a good grasp on why NCI exists, and to give you the tools to deal with almost any NCI issues in your consolidation.

What is NCI and when does it arise?

Before we calculate NCI, we need to have a good understanding of what it is. In its most basic form, non-controlling interests refers to interests in a company (i.e. shareholders) that don’t control a company.

You’ll also know that when looking at a single company on its own there’s never any mention of non-controlling interests. So where do they come from and why are we interested in them?

Well, the answer to those two questions is that NCI only arises on consolidation. Remember when we consolidate a subsidiary with its holding company, we consolidate 100% of the subsidiary’s profit and loss and100% of its balance sheet. That’s all very fine and well, but what happens if the holding company doesn’t own 100% of that subsidiary?

Surely, we should make some sort of disclosure or provision for something like that? It wouldn’t be correct to consolidate 100% of the earnings of a company and 100% of its balance sheet if we didn’t own 100% of that subsidiary without accounting for the piece we didn’t own. And that’s where the non-controlling interest comes into play.

That’s why:

- non-controlling interest arises only on consolidation and

- only when the holding the company holds less than 100% of the shares in the subsidiary

As per IFRS 10, “Non‑controlling interests represent the portion of equity in a subsidiary not attributable, directly or indirectly, to the parent. They are presented in the consolidated statement of financial position within equity (not as a liability).”

So we know we need to calculate something and that it belongs in the equity category of the consolidated financial statements.

So how does NCI get calculated?

Well, based on the definition of NCI above, this is an exercise that focuses on equity.

For purposes of this article, we’re going to split our guide into two pieces,

1) retained earnings (a special account in every accountant’s life) and

2) all other equity line items

Let’s start with retained earnings (profit and loss)

So, if we’re consolidating 100% of the profit and loss of the subsidiary, then that would be a good place to start.

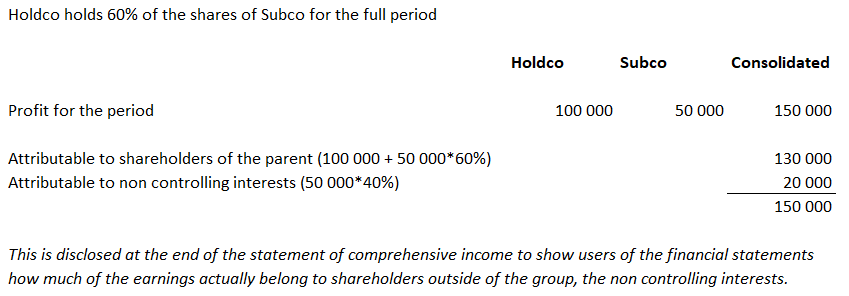

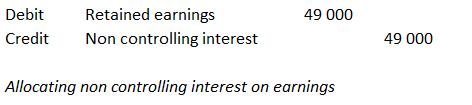

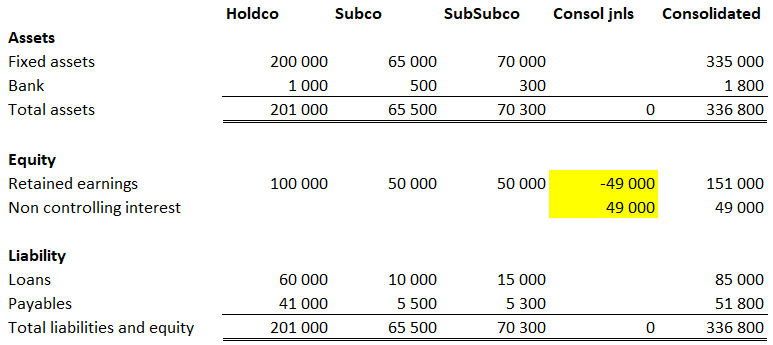

Example 1:

Below is an example of how we consolidate 100% of the earnings and show the users of the financials the split between what ultimately belongs to the parent (or Group) and the non-controlling interests.

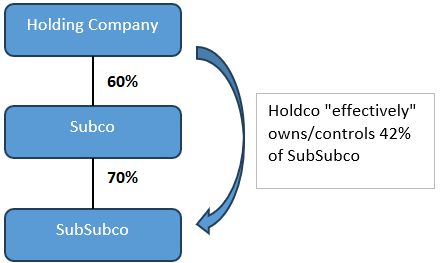

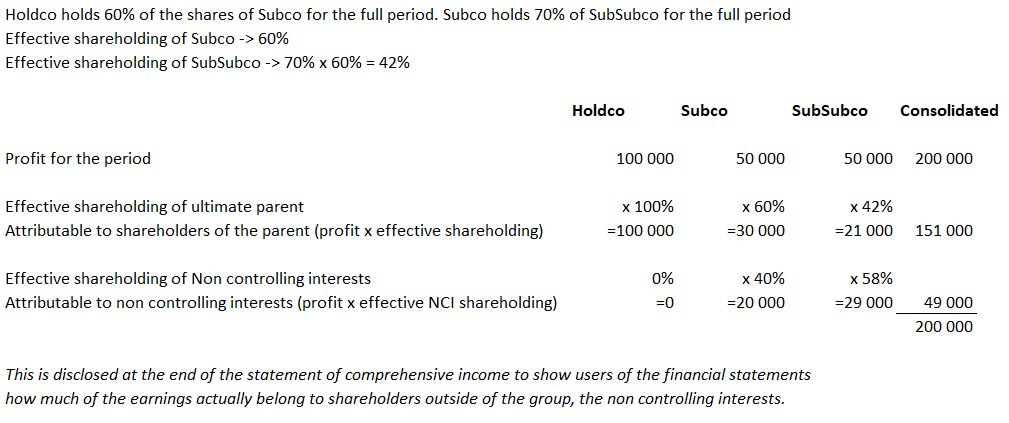

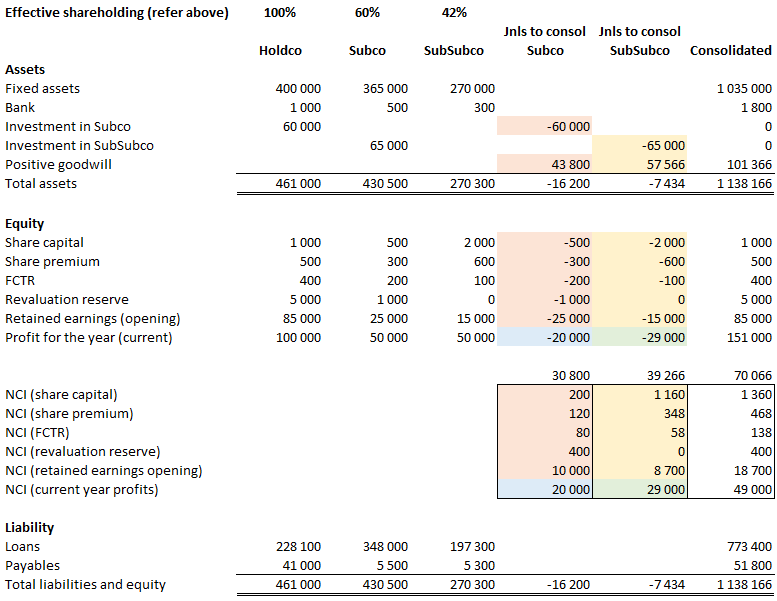

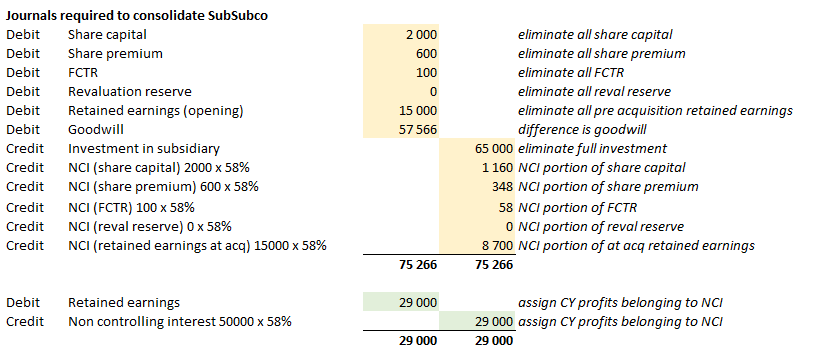

But what happens in a more complex group where a partially held subsidiary also has a partially held subsidiary?

Example 2:

We simply ask ourselves what the ultimate shareholding percentage is of each subsidiary and apply that percentage to its profit and loss.

You will also notice that we end up allocating 58% of SubSubco’s profit to the non-controlling interests even though we effectively control 100% of both subsidiaries, we are actually only entitled to 42% of its profits. You could very well end up with a scenario where the non-controlling interests outnumber the parent’s share of the profits.

So now that we’ve calculated the profit or loss attributable to non-controlling interests, what do we do with it? Well, other than disclosing it at the bottom of the profit and loss statement, we include that number in the NCI value on the balance sheet by moving it out of retained earnings. The number that we display in the balance sheet under retained earnings is only what is attributable to the shareholders of the ultimate parent in the group.

Remember that all earnings eventually end up in retained earnings, which means we need to take out the earnings that don’t “belong” to the ultimate parent. This is normally done with a consolidation journal after aggregating the entire group.

Do you need to allocate anything to NCI relating to intercompany eliminations of profit and loss items?

The short answer is no. The non-controlling interests are not affected at all by intercompany eliminations that are processed when preparing your consolidated profit and loss. In simple terms the non-controlling interests do not care and should not be affected simply because you decide to consolidate the company with its holding company and need to eliminate certain intercompany transactions.

Put yourself in the shoes of the non-controlling interests. Would you want your underlying value in a company changed simply because the company gets consolidated into a larger group? Of course not. Another way of looking at this is that the non-controlling interest is calculated at a company level and not at a group level and hence doesn’t get affected by intercompany eliminations against profit and loss.

See below how we “reallocate” the retained earnings that belong to the non-controlling interests on the consolidated balance sheet.

Note how we don’t change the underlying company’s results, only the consolidated value as NCI only arises on consolidation.

Allocation of the earnings owned by non-controlling interest to NCI on the balance sheet. The remaining amount in retained earnings is owned by the shareholders of the ultimate parent/group.

What about the other equity items?

Based on the definition of NCI we need to apply a carve out to all other line items of equity as well. This is fairly straightforward. We apply the effective NCI percentage to those line items in the balance sheet.

So, in summary we normally take each equity line item of the subsidiary and assign the effective non-controlling interest percentage to that equity to calculate our NCI value.

IFRS 3 adjustments

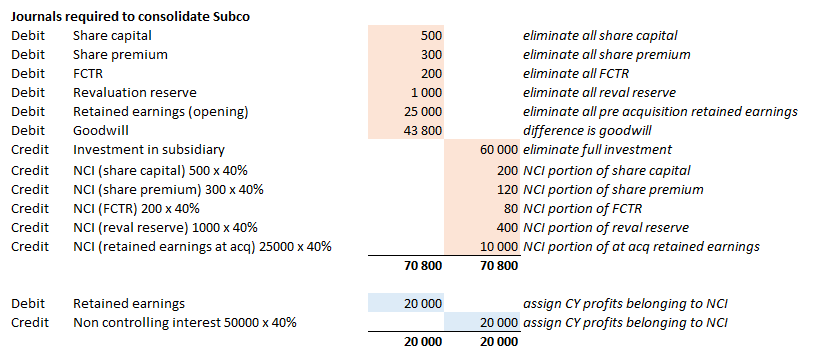

Any adjustments that you need to make to a subsidiary’s numbers as part of your consolidation process that result in a change to ANY of the equity line items of that subsidiary need to be apportioned between the parent and the non-controlling interest.

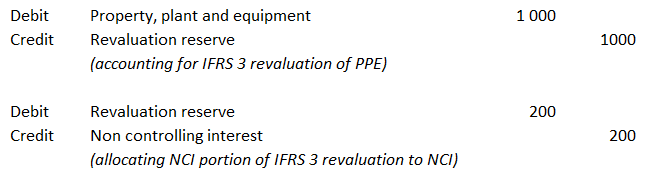

For example, any fair value adjustments that need to be made, either to property, plant and equipment or intangible assets, ultimately are the result of revaluing the subsidiary’s assets and therefore are directly tied to the subsidiary and therefore need to be carved out to the NCI as well, and these adjustments only happen on consolidation.

When assets are revalued to fair value during consolidation, the resulting increase in equity (revaluation reserve) is part of the subsidiary’s net assets. Therefore, NCI gets its proportionate share of that reserve.

If a subsidiary’s property, plant and equipment is revalued upward by 1 000 and the parent owns 80%, NCI (20%) would receive 200 in the revaluation reserve and is represented by the journal below (ignoring deferred tax in this example).

Consolidation journals would look like this.

Conclusion

Hopefully this guide has given you a deeper explanation of why NCI exists and how we go about calculating it. If you’d like to automate NCI and other technical consolidation processes in your business, reach out to us via our website or get in touch with us here, we’d be more than glad to have a chat about your needs and show you the Quick Consols application.

Get the latest updates, exclusive content, and exciting news delivered right to your inbox.

Share this Article

Get in touch!

If you have any questions about our Consolidation Software, send us a message below and we'll get back to you ASAP.