When an investor buys 50% or more of the shares in a company, an investor is considered to have control over that company. Of course there are instances where the shareholding is 50%or more however the investor doesn’t have control – we will discuss this in our next article.

When an investor gets control over a company for the first time, the transaction is called a business combination. What does this mean? This means that the investor in substance has acquired control over the assets and liabilities of the subsidiary. The investor has the right to make decisions over the operations, financing and investing of the company. In these instances, the investor is required to prepare consolidated financial statements and consolidate the acquired company.

One of the requirements for the preparation of consolidated financial statements is that the assets and liabilities of the subsidiary have to be shown at their respective fair values in order to account for the acquisition. I am sure you are wondering whether this makes any sense at all?! Lets unpack it further. Remember the subsidiary would have accounted for the assets and liabilities in its own books based on the requirements of the relevant IFRS – however on the date of acquisition we apply special rules – one of which is to get the assets and liabilities of the subsidiary to their fair values. This only happens at the date of acquisition.

Why does this special rule at the date of acquisition make sense? Remember when an investor buys shares in a company they are in essence buying a portion of the equity (net assets) of the subsidiary. It makes business / economic sense that the investor would pay market/fair value for these shares (these transactions are generally at arms length). However, the subsidiaries net asset are not recognised at fair value but at historic carrying amount. In order to determine the value of the synergies that are acquired (i.e. goodwill), the assets and liabilities need to be at fair value so that a meaning comparison can occur i.e. comparing apples (amount paid at fair value)with apples (fair value of the assets and liabilities).

The best example is property, plant and equipment which may be fully depreciated but still actually have a fair value to a buyer/acquirer.

These adjustments are done using proforma journal entries (proforma journals are called that because the exist only at a moment in time for consolidation purposes).The amounts in the subsidiaries separates books do not change. The proforma entries merely adjust the subsidiary’s trial balance in order to prepare the consolidated trial balance.

Lets look at an example:

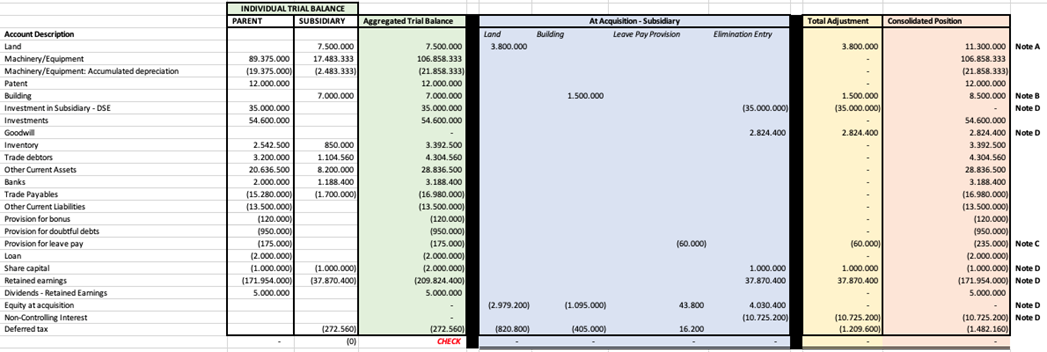

On 1 January 2024, Parent Limited acquired a 75% shareholding in Subsidiary Limited

Parent Limited paid 35000 000 for its shares.

Subsidiary Limited has the following equity balances on 1 January 2024

The non-controlling interest is measured at its proportionate share of the next assets at acquisition

Share Capital 1.000.000

Retained Earnings 37.870.400

Total Equity 38.870.400

Subsidiary Limited has land in its own books with a carrying amount of 7 500 000. This land is determined to have a fair value of 11 300 000

Subsidiary Limited has a building in its own books with a carrying amount of 7 000 000. This building is determined to have a fair value of 8 500 000

Subsidiary Limited has recognised a leave pay provision of 175000 in its own books. This leave pay provision is determined to have a fairvalue of 235 000

NOTES

For the notes below, ignore the carrying amounts of Parent Limited. These are included for completeness purposes.

Note A: We will need to increase the carrying amount of the subsidiary’s land to its fair value of 11 300 000. The carrying amount of the land of 7 500 000 has already been accounted for in the subsidiaries own accounting records. Because we are consolidating, we need to increase the carrying amount of the land by 3800 000 to get it to its fair value of 11 300 000.

Dr: Land 3 800 000

Cr: Equity at acquisition 3800 000

Cr: Deferred tax (SFP) 820 800

Why do we also increase the equity at acquisition?

If we think back to the accounting equation: Equity = Assets minus liabilities

When we increase the carrying amount of the asset, there is no corresponding change in the obligations of the subsidiary – therefore to balance this equation, this means that the equity value of the subsidiary has increased as a result of this fair value adjustment.

Equity increases on the credit side while assets increase on the debit side, hence the proforma journal entry above.

Note B: The same principle applies to the building , however its adjustment is 1500 000 because its carrying amount in the subsidiary’s own financial statements is 7 000 000 however the fair value was 8 500 000.

Dr: Building 1 500 000

Cr: Equity at acquisition 1095 000

Cr: Deferred tax (SFP) 405 000

What would we do if the fair value of the building was 6 200000?

In this instance we would have to reduce the carrying amountof the building by 800 000. Remember the subsidiary would have recognised thisbuilding in its books at 7 000 000 – at the date of acquisition we need to getthis asset to its fair value of 6 200 000.

Dr: Equity at acquisition 576 000

Dr: Deferred tax 216000

Cr: Building 800 000

Equity decreases on the debit side while assets decrease on the credit side, hence the proforma journal entry above.

Note C: The same principle applies to the leave pay provision. The subsidiary has accounted for a leave pay provision of 175 000 in its own books. However at acquisition, the leave provision should be at its fair value of 235 000. As such we need to increase the liability by 60 000

Dr: Equity at acquisition 43 800

Dr: Deferred tax 16200

Cr: Provision 60000

Why do we also decrease the equity at acquisition?

If we think back to the accounting equation: Equity = Assets minus liabilities

When we increase the carrying amount of the liability, there is no corresponding change in the assets of the subsidiary – therefore this means that the equity value of the subsidiary has decreased as a result of this fair value adjustment.

Equity decreases on the debit side while liabilities increase on the credit side, hence the proforma journal entry above.

Note D: All these adjustments will be needed in order to complete the consolidation at acquisition date. We will need to eliminate the subsidiary's equity against the investment.

WHY do we do this? Remember when we add the trial balances of the parent and the subsidiary, we end up in a position where we have the investment in the subsidiary (this was recognised by the parent – a debit balance) and we have the share capital, retained earning etc (this is recognised by the subsidiary – credit balances). In substance, the investment in subsidiary (what the parent paid) represents the equity of the subsidiary (what the parent paid for).You can almost think of this similarly to how we look at intercompany balances and their elimination. We therefore need to eliminate the investment in subsidiary against the equity of the subsidiary.

Dr: Equity at acquisition xxxx

Dr: Share capital xxxx

Dr: Retained earnings xxxx

Cr: Investment xxxx

Furthermore, we will need to recognise the non-controlling interest equity holders based on the % the parent doesn’t own and any goodwill or the gain on bargain purchased.

If we do not value the assets at acquisition, we will end up understating the subsidiaries equity and could end up with an overstated goodwill amount. Remember, in the goodwill balance we only want to include things that cannot be separated from the subsidiary i.e. we cannot sell the items/lease/transfer the items without selling the subsidiary itself.

Get in touch

The only thing we love more than Goodwill calculations are our customers. If you’d like to see how we can automate your consolidation, group reporting or financial statement preparation with the Quick Consols consolidation software and financial statement software, we’d love to hear from you and show you the software in a one on one demo.

You can follow our Linkedin page here for regular updates and take a look at our other content here.

Get the latest updates, exclusive content, and exciting news delivered right to your inbox.

Share this Article

Get in touch!

If you have any questions about our Consolidation Software, send us a message below and we'll get back to you ASAP.